A lease is more than just a contract for space; it is a multi-million dollar bet on your landlord’s financial stability. Whether you are managing a global warehouse network or a large-scale office portfolio, your operational continuity depends on the person across the table. And in today’s volatile market, the most critical “inspection” isn’t of the brick and mortar—it’s of the debt service coverage ratio (DSCR).

If your landlord is facing financial strain, your “Class A” experience can quickly dissolve into deferred maintenance, tax liens, or even the nightmare of a mortgage loan foreclosure. Here is how sophisticated real estate investors and corporate tenants use DSCR to protect their interests and why REoptimizer® is the essential tool for flagging these risks before they become your problem.

What is DSCR (Debt Service Coverage Ratio)?

The Debt Service Coverage Ratio (DSCR) is a financial metric used by many lenders to determine a borrower’s capacity to repay a loan. In simple terms, DSCR measures whether the property generates enough cash flow to cover loan payments.

For a tenant, the landlord’s DSCR is a barometer for their ability to maintain the property. If the ratio is too low, the landlord is likely “robbing Peter to pay Paul”—diverting your monthly rent to cover current debt obligations instead of essential operating expenses.

How to Calculate DSCR

To calculate DSCR, you divide the property’s net operating income (NOI) by its total debt service:

DSCR=Total Debt ServiceNet Operating Income (NOI)

- Net Operating Income (NOI): This is the rental income minus operating expenses (such as taxes, insurance, and maintenance).

- Total Debt Service: This includes all principal and interest payments on the mortgage loan.

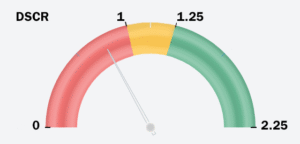

Benchmarks: What is an “Acceptable DSCR”?

Understanding the numbers is the first step in identifying financial difficulties in your landlord’s portfolio.

- DSCR > 1.25: This is the common industry standard for most real estate investors. It means the property generates 25% more income than is needed to cover loan payments.

- DSCR = 1.0: The property is just breaking even. One major vacancy or a spike in the annual interest rate could push the property into the red.

- DSCR < 1.0: A low DSCR indicates that the rental property’s cash flow is insufficient to cover mortgage payments.

The “Office Trap”: Why Office Tenants Face Higher Risk

For the office sector, a standard 1.25x DSCR is a starting point. Because office buildings have high tenant concentration and massive down payments required for tenant improvements (TIs), lenders often demand a minimum DSCR of 1.35x to 1.40x to approve an office mortgage loan.

The NOI Cash Flow Crisis

In the office world, Net Operating Income (NOI) is under siege. Unlike warehouse spaces with triple-net (NNN) leases that pass most costs to the tenant, office landlords often bear the brunt of:

- Skyrocketing Insurance Premiums: Insurance is a primary operating expense that has jumped 20–40% in some urban markets.

- Capital Expenditure (CapEx) vs. NOI: Standard DSCR calculation methods often exclude CapEx. However, an office landlord must spend heavily on lobbies and “amenitization” to attract tenants. If they are spending their cash on debt instead of CapEx, your building is effectively “dying on the vine.”

The Danger of Cross-Collateralization with a DSCR Loan

This is the “invisible” threat for a corporate tenant. Many large-scale office landlords use cross-collateralization, where multiple properties serve as collateral for a single mortgage loan (often called a blanket mortgage).

- The Scenario: Your office building might have a “healthy” individual DSCR of 1.30x.

- The Risk: If your landlord’s warehouse in another state loses its anchor tenant and its DSCR drops to 0.80x, the lender can trigger a cross-default.

- The Result: The lender could seize your building even if its performance is perfect. This “portfolio contagion” is why you must look beyond the single asset to the borrower’s capacity across their entire holdings.

Strategic Management: How to Audit Your Landlord

While you may not always have access to a landlord’s private tax returns, you can use the following factors to estimate their DSCR calculation:

- Analyze Market Rents: Use monthly rental income data for the property’s location to estimate the revenue.

- Monitor Tenant Turnover: If an office building has 20% of its leases expiring in the same period, the NOI is at extreme risk, which will tank the DSCR.

- Review Loan Terms: Research when the property was purchased. Loans from 2021 with low interest rates are now facing “refinancing cliffs” where the new annual interest rate will double the monthly payments.

Don’t Let Their Debt Become Your Disaster

In the current market, a strong DSCR is the ultimate sign of a reliable landlord. As a corporate tenant, you have the responsibility to understand the financial health of the entities housing your operations.

Are you ready to see the hidden risks in your CRE portfolio?

Stop guessing and start optimizing. REoptimizer® is the only transaction management software built to give corporate tenants an “institutional-grade” look at their landlords’ financial health. We don’t just help you manage leases; we help you audit the entities behind them.

Why REoptimizer® is Your Ultimate Shield:

- The Landlord Watchlist: Our platform flags landlords who are under financial strain based on real-time market data, debt maturity “cliffs,” and historical performance.

- Red & Yellow Flag Alerts: Instantly see which properties in your portfolio have a low DSCR or rising operating expenses that could trigger a service lapse.

- Cross-Collateralization Mapping: We reveal the hidden links in your landlord’s debt. If your warehouse is cross-collateralized with a failing office tower, REoptimizer® puts that risk on your dashboard before the lender sends a default notice.

- NOI Stress Testing: See how your building’s Net Operating Income holds up against shifting interest rates and inflation, giving you a clear picture of your borrower’s capacity.

Contact REoptimizer® today for a free portfolio health check. See exactly how our software can identify cross-default risks, flag high-risk debt obligations, and save you millions in hidden operational disruptions. Book a demo to see the difference it can have on your portfolio today.

Frequently Asked Questions: Navigating Landlord DSCR Risk

For corporate tenants, the financial health of a landlord is just as important as the physical health of the building. Below are the most common questions regarding the debt service coverage ratio and how it impacts your investment decisions.

How do you use the DSCR formula for a commercial landlord?

To perform a dscr calculation on a potential landlord, you need to estimate the building’s Net Operating Income (NOI) and divide it by the total debt service. While you may not have their exact ledger, you can use a dscr calculator approach by researching:

- Revenue: Estimated monthly rental income based on the building’s square footage and current market rates for the property’s location.

- Expenses: Standard operating expenses (usually 25–35% of gross income for office/warehouse) including taxes, insurance, and maintenance.

- Debt: Estimated principal and interest payments based on the property’s last recorded loan amount and the prevailing interest rate at the time of financing.

What is considered an acceptable DSCR for office vs. warehouse properties?

While many lenders accept a minimum DSCR of 1.25x for general investment property, the “safety zone” varies by asset class:

- Warehouse/Industrial: Because these often have stable, long-term NNN leases, a ratio of 1.20x to 1.25x is typically an acceptable DSCR.

- Office Space: Due to higher tenant turnover and the massive down payment required for tenant improvements (TIs), savvy tenants look for a landlord with a DSCR of 1.35x or higher. Anything lower suggests the landlord may lack the liquidity to fund your next office build-out.

How does a high interest rate impact a landlord’s debt service?

The annual interest rate is the most volatile component of the dscr formula. If a landlord has a floating-rate mortgage loan or an upcoming “refinancing cliff,” a 2% jump in the interest rate can instantly drop a healthy 1.30x DSCR to a sub-1.0 financial strain level. This is why REoptimizer® tracks market cycles—to warn you when your landlord’s borrower’s capacity is shrinking.

Can I use a DSCR loan calculator to estimate landlord risk?

Yes. A dscr loan calculator is a great “reverse engineering” tool. By inputting the property’s estimated value and the current loan to value (LTV) ratios, you can determine the maximum debt service the property can handle. If the resulting monthly payments are nearly equal to the estimated monthly rent, the landlord has zero margin for error.

What are the “other factors” that can tank a property’s DSCR?

Beyond the basic dscr calculation, tenants should watch for:

- Cross-Collateralization: If your office building is tied to a struggling retail mall in the same mortgage loan pool.

- Soft Market Conditions: Rising vacancy rates in the same period that expenses like insurance and taxes are increasing.

- Capital Expenditures: One-time costs (like a roof replacement) that aren’t in the NOI but drain the cash needed to repay the loan.

Proactive Portfolio Protection

In the high-stakes world of corporate CRE, information is your only shield. Don’t wait for a “For Sale” sign or a lapse in building services to realize your landlord is in trouble.

REoptimizer® gives you the data-driven edge to:

- Flag High-Risk Landlords: Identify owners with low DSCR and heavy debt obligations.

- Optimize Deal Terms: Use landlord financial weakness as leverage for better lease protections.

- Centralize Portfolio Health: See all your office and warehouse risks in one interactive dashboard.