For the Fortune 500 real estate director, a lease is more than a right to occupy; it is a long-term liability that requires active hedging. Central to this hedge is the expense stop, a mechanism that defines the boundary between a predictable overhead and an escalating variable cost.

The expense stop is the pivot point of this risk. It is a contractual provision that sets a maximum limit on the landlord’s operating expenses.

While it serves to provide a predictable “floor” for the landlord’s contribution, it simultaneously functions as a latent liability for the tenant. For the sophisticated occupier, understanding the interplay between the base year, actual expenses, and annual increases is the difference between budget stability and an unexpected multi-million dollar hit to the EBITDA.

Expense Stop: The Landlord’s Hedge and the Tenant’s Exposure

An expense stop in commercial real estate is essentially a risk-transfer mechanism. It is primarily used in Full-Service Gross Leases to protect landlords from rising costs while providing tenants with a predictable initial rent. By setting a certain amount—typically expressed per square foot—the landlord caps their financial liability.

From the landlord’s perspective, this provision ensures predictable cash flow. The risk of rising inflation, sudden spikes in utility costs, or labor increases for building expenses is transferred to the tenant.

If the actual operating expenses rise to $12 per square foot while the expense stop amount is set at $10, the tenant is responsible for the $2 difference. On a 100,000-square-foot headquarters, this “minor” fluctuation results in a $200,000 unbudgeted expense.

However, the expense stop is not inherently predatory; it can provide predictability for tenants in terms of operating expenses, allowing them to budget effectively for the first year. The risk, however, is that if the initial stop is set artificially low during lease negotiations, the tenant may be exposed to large, immediate increases in subsequent years.

Base Year: Defining the Economic Baseline

The base year is the chronological anchor of a commercial lease. While it can be any year agreed upon, it is typically the first year of the lease term. In a full service or modified gross lease, the landlord pays for all operating expenses incurred during this period. The actual amount of expenses tied to this window becomes the “floor” for the remainder of the term.

For the C-suite, the base year amount is a critical data point. If a tenant signs a lease in a building that is only 50% occupied during the base year, the actual expenses will be deceptively low. As the building fills and occupancy reaches 95%, the variable expenses—such as janitorial services, utilities, and property management fees—will skyrocket.

Without proper lease protections, such as a “Gross-Up” clause, the tenant will face significant rent increases simply because the landlord was successful in leasing the rest of the building. A sophisticated new lease negotiation must ensure the base year is adjusted to reflect a fully occupied building, creating a “realistic base year” that prevents unfair spikes in the second year and beyond.

Operating Expenses: The Anatomy of “Additional Rent”

To manage a large-scale portfolio, one must look beyond the total sum and analyze the components of building operating expenses. These generally include:

- Property Taxes: Often the largest and most volatile uncontrollable expense.

- Insurance: Subject to global market shifts and climate-related adjustments.

- Common Area Maintenance (CAM): The costs of operating shared lobbies, elevators, and parking structures.

- Property Management Fees: Usually calculated as a percentage of gross revenue.

In a full service lease, the tenant benefits from the landlord’s management of these services, but they assume the risk of any operating costs that exceed the specified expense stop. This can lead to significant, unexpected increases in total rent.

Conversely, in a net lease, the tenant pays their pro rata share of all expenses from day one. While a net lease offers more transparency, the gross lease with an expense stop is often preferred by large corporations for the initial budget certainty it provides, provided the base year stop is negotiated aggressively.

Commercial Real Estate Portfolio Strategy: Mitigation and Negotiation

A Fortune 500 tenant must approach commercial real estate leases with a defensive mindset. Because the risk of unexpected increases in property expenses is transferred to the tenant—supporting the stability of the landlord’s investment—the tenant must negotiate counter-measures.

- Negotiating the Expense Cap: While the expense stop limits the landlord’s downside, a sophisticated tenant will negotiate for an “expense cap.” This is a secondary ceiling that limits how much the tenant’s pro rata share can increase year-over-year. For example, capping annual increases on controllable operating expenses (like landscaping or security) at 5% ensures that the landlord has an incentive to manage the property efficiently.

- The Power of Audit Rights: Many tenants fail to exercise their right to verify actual expenses. Tenants should negotiate robust audit rights to ensure accuracy in the landlord’s operating expense statements. Requesting an annual audit prevents the landlord from passing through capital expenditures (which should be the landlord’s cost) as common area maintenance.

- Understanding the Base Year Lease vs. Expense Stop Amount: It is a common misconception that all commercial leases handle increases the same way. In a base year lease, the tenant is responsible for any increase in operating expenses over the actual expenses of the first year. In a lease with a fixed expense stop amount, the dollar figure is hard-coded (e.g., $10.00/SF). If the building’s actual expenses in the first year are already $11.00/SF, the tenant is effectively paying overages from the moment they move in.

Common Area Maintenance: The Friction Point

The common area maintenance (CAM) section of a lease is where most disputes arise. For a large-scale office building, CAM includes everything from HVAC maintenance to the flowers in the lobby.

Sophisticated tenants must scrutinize the definition of CAM to exclude:

- Executive salaries of the landlord’s personnel.

- Marketing costs for vacant spaces.

- Costs associated with other specific tenants’ modified gross leases.

- Taxes and insurance that should be itemized separately to ensure they are not being marked up by management fees.

By tightening these definitions, the tenant ensures that the difference they pay between the actual expenses and the base year stop represents legitimate, market-rate increases rather than landlord inefficiencies.

From Strategy to Execution: Optimizing with REoptimizer®

The most critical insight for a C-suite executive is that an expense stop is not a static figure; it is a dynamic risk that requires continuous monitoring. For organizations managing a high-volume, large-scale portfolio, manual tracking in spreadsheets is an invitation for budget leakage and missed audit windows.

To turn real estate from a passive expense into a strategic asset, forward-thinking tenants leverage REoptimizer®, a cloud-based transaction and lease management platform designed specifically for corporate tenants.

How REoptimizer® Protects Your Bottom Line:

- Centralized Expense Clarity: REoptimizer® acts as a single source of truth, centralizing all lease documents and abstracting critical data points like your base year stop, expense caps, and audit rights.

- Automated Anomaly Detection: The software provides instant visibility into overspending. By benchmarking your actual operating expenses against market data and previous years, REoptimizer® identifies red flags—such as “spiking” variable costs or miscalculated pro rata shares—before they become permanent losses.

- Audit Readiness: When it’s time to exercise your audit rights, REoptimizer® ensures you have the historical data and line-item clarity needed to hold landlords accountable, ensuring you aren’t paying for capital improvements or non-allowable CAM charges.

- Strategic Decision Support: Using interactive dashboards and AI-powered data mapping, REoptimizer® allows you to simulate “what-if” scenarios. You can see the long-term impact of rising property taxes or inflation on your entire portfolio’s occupancy costs years in advance.

Take Control of Your Portfolio Today

Don’t leave your corporate real estate budget to chance or landlord-favorable estimates. Whether you are negotiating a new high-rise lease or auditing a global portfolio, the right technology is your best defense.

Ready to see what you should be paying?

Schedule a Demo of REoptimizer® today to discover how our patented technology can identify inefficiencies, lower your CRE spend, and provide the transparency your C-suite demands.

Book a Demo

A lease is more than just a contract for space; it is a multi-million dollar bet on your landlord’s financial stability. Whether you are managing a global warehouse network or a large-scale office portfolio, your operational continuity depends on the person across the table. And in today’s volatile market, the most critical “inspection” isn’t of the brick and mortar—it’s of the debt service coverage ratio (DSCR).

If your landlord is facing financial strain, your “Class A” experience can quickly dissolve into deferred maintenance, tax liens, or even the nightmare of a mortgage loan foreclosure. Here is how sophisticated real estate investors and corporate tenants use DSCR to protect their interests and why REoptimizer® is the essential tool for flagging these risks before they become your problem.

What is DSCR (Debt Service Coverage Ratio)?

The Debt Service Coverage Ratio (DSCR) is a financial metric used by many lenders to determine a borrower’s capacity to repay a loan. In simple terms, DSCR measures whether the property generates enough cash flow to cover loan payments.

For a tenant, the landlord’s DSCR is a barometer for their ability to maintain the property. If the ratio is too low, the landlord is likely “robbing Peter to pay Paul”—diverting your monthly rent to cover current debt obligations instead of essential operating expenses.

How to Calculate DSCR

To calculate DSCR, you divide the property’s net operating income (NOI) by its total debt service:

DSCR=Total Debt ServiceNet Operating Income (NOI)

- Net Operating Income (NOI): This is the rental income minus operating expenses (such as taxes, insurance, and maintenance).

- Total Debt Service: This includes all principal and interest payments on the mortgage loan.

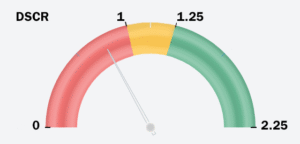

Benchmarks: What is an “Acceptable DSCR”?

Understanding the numbers is the first step in identifying financial difficulties in your landlord’s portfolio.

- DSCR > 1.25: This is the common industry standard for most real estate investors. It means the property generates 25% more income than is needed to cover loan payments.

- DSCR = 1.0: The property is just breaking even. One major vacancy or a spike in the annual interest rate could push the property into the red.

- DSCR < 1.0: A low DSCR indicates that the rental property’s cash flow is insufficient to cover mortgage payments.

The “Office Trap”: Why Office Tenants Face Higher Risk

For the office sector, a standard 1.25x DSCR is a starting point. Because office buildings have high tenant concentration and massive down payments required for tenant improvements (TIs), lenders often demand a minimum DSCR of 1.35x to 1.40x to approve an office mortgage loan.

The NOI Cash Flow Crisis

In the office world, Net Operating Income (NOI) is under siege. Unlike warehouse spaces with triple-net (NNN) leases that pass most costs to the tenant, office landlords often bear the brunt of:

- Skyrocketing Insurance Premiums: Insurance is a primary operating expense that has jumped 20–40% in some urban markets.

- Capital Expenditure (CapEx) vs. NOI: Standard DSCR calculation methods often exclude CapEx. However, an office landlord must spend heavily on lobbies and “amenitization” to attract tenants. If they are spending their cash on debt instead of CapEx, your building is effectively “dying on the vine.”

The Danger of Cross-Collateralization with a DSCR Loan

This is the “invisible” threat for a corporate tenant. Many large-scale office landlords use cross-collateralization, where multiple properties serve as collateral for a single mortgage loan (often called a blanket mortgage).

- The Scenario: Your office building might have a “healthy” individual DSCR of 1.30x.

- The Risk: If your landlord’s warehouse in another state loses its anchor tenant and its DSCR drops to 0.80x, the lender can trigger a cross-default.

- The Result: The lender could seize your building even if its performance is perfect. This “portfolio contagion” is why you must look beyond the single asset to the borrower’s capacity across their entire holdings.

Strategic Management: How to Audit Your Landlord

While you may not always have access to a landlord’s private tax returns, you can use the following factors to estimate their DSCR calculation:

- Analyze Market Rents: Use monthly rental income data for the property’s location to estimate the revenue.

- Monitor Tenant Turnover: If an office building has 20% of its leases expiring in the same period, the NOI is at extreme risk, which will tank the DSCR.

- Review Loan Terms: Research when the property was purchased. Loans from 2021 with low interest rates are now facing “refinancing cliffs” where the new annual interest rate will double the monthly payments.

Don’t Let Their Debt Become Your Disaster

In the current market, a strong DSCR is the ultimate sign of a reliable landlord. As a corporate tenant, you have the responsibility to understand the financial health of the entities housing your operations.

Are you ready to see the hidden risks in your CRE portfolio?

Stop guessing and start optimizing. REoptimizer® is the only transaction management software built to give corporate tenants an “institutional-grade” look at their landlords’ financial health. We don’t just help you manage leases; we help you audit the entities behind them.

Why REoptimizer® is Your Ultimate Shield:

- The Landlord Watchlist: Our platform flags landlords who are under financial strain based on real-time market data, debt maturity “cliffs,” and historical performance.

- Red & Yellow Flag Alerts: Instantly see which properties in your portfolio have a low DSCR or rising operating expenses that could trigger a service lapse.

- Cross-Collateralization Mapping: We reveal the hidden links in your landlord’s debt. If your warehouse is cross-collateralized with a failing office tower, REoptimizer® puts that risk on your dashboard before the lender sends a default notice.

- NOI Stress Testing: See how your building’s Net Operating Income holds up against shifting interest rates and inflation, giving you a clear picture of your borrower’s capacity.

Contact REoptimizer® today for a free portfolio health check. See exactly how our software can identify cross-default risks, flag high-risk debt obligations, and save you millions in hidden operational disruptions. Book a demo to see the difference it can have on your portfolio today.

Book a Demo

Frequently Asked Questions: Navigating Landlord DSCR Risk

For corporate tenants, the financial health of a landlord is just as important as the physical health of the building. Below are the most common questions regarding the debt service coverage ratio and how it impacts your investment decisions.

How do you use the DSCR formula for a commercial landlord?

To perform a dscr calculation on a potential landlord, you need to estimate the building’s Net Operating Income (NOI) and divide it by the total debt service. While you may not have their exact ledger, you can use a dscr calculator approach by researching:

- Revenue: Estimated monthly rental income based on the building’s square footage and current market rates for the property’s location.

- Expenses: Standard operating expenses (usually 25–35% of gross income for office/warehouse) including taxes, insurance, and maintenance.

- Debt: Estimated principal and interest payments based on the property’s last recorded loan amount and the prevailing interest rate at the time of financing.

What is considered an acceptable DSCR for office vs. warehouse properties?

While many lenders accept a minimum DSCR of 1.25x for general investment property, the “safety zone” varies by asset class:

- Warehouse/Industrial: Because these often have stable, long-term NNN leases, a ratio of 1.20x to 1.25x is typically an acceptable DSCR.

- Office Space: Due to higher tenant turnover and the massive down payment required for tenant improvements (TIs), savvy tenants look for a landlord with a DSCR of 1.35x or higher. Anything lower suggests the landlord may lack the liquidity to fund your next office build-out.

How does a high interest rate impact a landlord’s debt service?

The annual interest rate is the most volatile component of the dscr formula. If a landlord has a floating-rate mortgage loan or an upcoming “refinancing cliff,” a 2% jump in the interest rate can instantly drop a healthy 1.30x DSCR to a sub-1.0 financial strain level. This is why REoptimizer® tracks market cycles—to warn you when your landlord’s borrower’s capacity is shrinking.

Can I use a DSCR loan calculator to estimate landlord risk?

Yes. A dscr loan calculator is a great “reverse engineering” tool. By inputting the property’s estimated value and the current loan to value (LTV) ratios, you can determine the maximum debt service the property can handle. If the resulting monthly payments are nearly equal to the estimated monthly rent, the landlord has zero margin for error.

What are the “other factors” that can tank a property’s DSCR?

Beyond the basic dscr calculation, tenants should watch for:

- Cross-Collateralization: If your office building is tied to a struggling retail mall in the same mortgage loan pool.

- Soft Market Conditions: Rising vacancy rates in the same period that expenses like insurance and taxes are increasing.

- Capital Expenditures: One-time costs (like a roof replacement) that aren’t in the NOI but drain the cash needed to repay the loan.

Proactive Portfolio Protection

In the high-stakes world of corporate CRE, information is your only shield. Don’t wait for a “For Sale” sign or a lapse in building services to realize your landlord is in trouble.

REoptimizer® gives you the data-driven edge to:

- Flag High-Risk Landlords: Identify owners with low DSCR and heavy debt obligations.

- Optimize Deal Terms: Use landlord financial weakness as leverage for better lease protections.

- Centralize Portfolio Health: See all your office and warehouse risks in one interactive dashboard.

Learn More

Rent escalations aren’t inherently “bad.” They’re a normal part of commercial leasing meant to protect a landlord’s revenue over time. The real risk is how the escalation is structured—and how easily the language can shift volatility, compounding, and index-selection power onto the tenant.

This is why escalation clauses are one of the most common “quiet cost drivers” in a lease: the numbers often look acceptable in Year 1, but the clause can create an outsized impact by Year 7, 10, or 15. Let’s talk about how to avoid this.

What Is A Rent Escalation Clause?

A rent escalation clause defines how rent increases over the lease term, including timing (annual, every other year, at specific milestones) and the method used (index-based, fixed, hybrid, or bumps). The nuance most teams miss is that escalations are typically compounding: each increase builds on the last year’s rent, not the original base. That compounding effect is where “small” differences in language become meaningful portfolio-level budget outcomes.

Two subtle points that matter in negotiations:

-

Escalation method interacts with term length. A clause that seems tolerable in a 5-year deal can become a serious exposure in a 12–15 year deal.

-

Escalation language often includes embedded leverage. Index selection, floor/ceiling language, notice timing, and calculation method can all tilt results—without changing the headline escalation “type.”

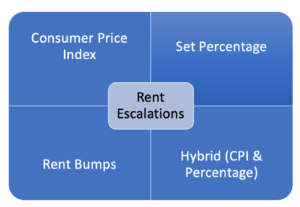

The Four Basic Types Of Rent Escalations

1. CPI Or Inflation-Based Escalations

CPI-based escalations are often presented as “fair”—rent only rises with inflation. But the practical reality is that CPI clauses can be one-sided risk transfer if they don’t include guardrails.

Where CPI gets dangerous (the nuance):

-

Index selection isn’t neutral. Landlords may specify a CPI measure or geography that best supports higher increases. Even small differences in index definition can create materially different outcomes over time.

-

CPI clauses can have “silent” floors. Some CPI clauses include a minimum increase (a floor) even when CPI is low, but still allow full upside when CPI is high. That’s not “inflation protection”—that’s asymmetry.

-

Timing matters more than most people think. CPI is usually measured over a period (e.g., year-over-year). If the clause uses a measurement window that catches an inflation spike, that spike can become embedded in the rent base going forward.

-

Compounding locks in the pain. Even if inflation cools later, the higher rent established during the spike becomes the new baseline for future increases.

How REoptimizer® helps (subtle but powerful):

-

Flags CPI escalation language and the fine print (index, geography, lookback window, floor/ceiling language)

-

Converts the clause into a plain-English summary: “Your rent increases by X, measured by Y, calculated on Z schedule, with limits of A/B”

-

Models multiple inflation scenarios so you can see how “reasonable” becomes “runaway” across the term, especially in longer leases

Negotiation angle that often works:

If CPI is on the table, push for caps and clarity (and avoid floors that create upside-only outcomes). When landlords insist on CPI, the win is often in the guardrails—not in eliminating CPI entirely.

2. Fixed Percentage Escalations

Fixed escalations are typically the most tenant-friendly option because they turn uncertainty into a schedule. But “fixed” doesn’t automatically mean “optimized”—the details still matter.

The nuance in fixed escalations:

-

Fixed is predictable, not always cheap. A fixed 3% may be a win versus CPI during high inflation—but in low-inflation periods it can cost more than what CPI would have done. The key is whether the predictability premium is worth it for your organization.

-

The compounding effect is still real. A fixed increase compounds too, so the difference between 2.5% and 3% is not linear over 10+ years.

-

Fixed escalations can hide in base rent resets. Some leases combine a fixed escalation with periodic “reset to market” language or appraisal mechanisms that function like a second escalation.

-

Fixed increases interact with concessions. A landlord may trade a slightly lower fixed escalation for changes elsewhere (free rent, TI, abatement language, operating expense treatment). The “best deal” is often the one with the best total economics, not the lowest escalation percentage.

Negotiation angle that often works:

Fixed escalations are easiest to justify internally. They also make it easier to create landlord competition because you can compare offers apples-to-apples across properties.

3. Hybrid Escalations (Fixed + CPI Triggers Or Limits)

Hybrid systems are where complexity starts doing real damage—or real good—depending on how they’re structured. A well-built hybrid can be a smart compromise in long-term deals. A poorly built hybrid can quietly recreate CPI risk while looking tenant-friendly.

The nuance in hybrids:

-

Hybrids should reduce volatility, not reintroduce it. The goal is a controlled range of outcomes. If a hybrid clause still allows large CPI swings with minimal limits, it’s not really a hybrid—it’s CPI with extra steps.

-

Trigger design is everything. A “trigger” could be CPI above a threshold, but you need to examine:

-

What measurement period is used?

-

What happens when CPI goes back down?

-

Does the escalation revert, or does it ratchet upward permanently?

-

Caps/floors can create asymmetry. A ceiling (cap) helps tenants. A floor helps landlords. Some hybrids include both—fine—unless the floor is set high and the cap is set too high to matter.

-

Hybrids can be structured as “bands.” For example: 3% unless CPI exceeds X, then 4% for that year only, then revert when CPI normalizes. That approach contains exposure better than “CPI in full if CPI exceeds X.”

Negotiation angle that often works:

Hybrids are a useful concession when landlords won’t commit to fixed increases across long terms. The tenant win is getting the hybrid to behave like a fixed schedule most years while limiting worst-case inflation exposure.

4. Rent Bumps (Set Dollar Increases)

Rent bumps are often viewed as simple, but they can carry their own nuance—especially in how frequently they occur and how they align to market dynamics.

The nuance in rent bumps:

-

Bumps can be more transparent than percentages. Stakeholders can understand “+$0.50/SF” more quickly than compounding percentages—useful for approvals and budgeting.

-

Frequency is negotiable in some markets. Annual bumps are common, but every-other-year bumps can appear when demand is lower or when landlords are trying to stabilize occupancy.

-

Bumps behave differently depending on the starting rent. A $1.00/SF bump is a larger effective percentage when starting rent is low and a smaller effective percentage when starting rent is high. That matters when comparing proposals.

-

Bumps can be paired with renewal options strategically. Tenants can sometimes negotiate different bump schedules for base term vs. renewal periods, aligning increases to business uncertainty.

Negotiation angle that often works:

If you can’t win on the bump amount, win on the timing (less frequent increases) or on other economic levers that reduce total occupancy cost.

Why CPI Escalations Tend To Be The Most Dangerous

CPI escalations feel reasonable because they’re anchored to “inflation,” which sounds objective. But CPI clauses are often where landlords can embed the most optionality and the least predictability for tenants. The biggest tenant-side risk isn’t CPI itself—it’s CPI without boundaries, combined with compounding.

REoptimizer® helps teams avoid the classic mistake: evaluating escalation clauses based on what inflation has been, rather than what it could be over the life of the lease.

How To Negotiate A More Tenant-Friendly Escalation

A strong escalation strategy typically looks like this:

-

Start with a fixed schedule preference (predictability wins internal buy-in)

-

If CPI enters the deal, contain it with clear caps and transparent definitions

-

Avoid one-way clauses (floors without meaningful caps, or ratchets that never revert)

-

Use competition to force landlords to price risk fairly

REoptimizer® supports this by turning lease language into a financial narrative: what you’re paying, when you’re paying it, and what could change under different conditions—so the negotiation isn’t emotional, it’s mathematical.

REoptimizer® Use Cases For Escalation Clauses

-

Clause Risk Flagging: Identify CPI, ratchets, floors, and hybrid triggers early—before late-stage legal review.

-

Scenario Modeling: Test inflation environments so teams can see exposure boundaries, not just the “expected” path.

-

Budget-Ready Rent Schedules: Generate stakeholder-friendly schedules that align to term, options, and renewal structure.

-

Negotiation Prep: Quantify alternatives so you can trade intelligently (e.g., escalation concessions in exchange for TI, free rent, or better renewal terms).

Schedule a demo today to see hoe REoptimizer® can level up your portfolio by strengthening each individual lease.

Book a Demo

FAQ’s Rent Escalation:

Which rent escalation is safest for tenants?

Most tenants prefer 2. Fixed Percentage Escalations because predictability reduces budget risk and approval friction.

Why can CPI escalations become expensive even if inflation falls later?

Because rent is usually compounding. A high CPI year can increase the base rent permanently, and subsequent increases build on that higher number.

Are hybrid escalations good or bad?

3Hybrids can be good when they genuinely limit volatility (caps, bands, reversion). They’re risky when they add complexity without adding real limits.

Are rent bumps better than fixed percentages?

Rent Bumps can be excellent for transparency and, in some cases, negotiable frequency. The “better” option depends on starting rent, bump size, and term length.

Commercial lease renewals are no longer a routine administrative task. In today’s office market, they are one of the most powerful—and underutilized—levers for reducing occupancy costs, improving space utilization, and reshaping a company’s real estate portfolio.

Done strategically, a renewal can unlock millions in savings, flexibility, and optionality. Done passively, it can quietly lock in outdated economics, underused space, and unnecessary risk for years.

This guide explains how to approach commercial lease renewals—and how modern portfolio intelligence tools like REoptimizer® allow tenants to make renewal decisions with clarity, leverage, and confidence.

What Is A Commercial Lease Renewal?

A commercial lease renewal is the process of extending, renegotiating, or restructuring an existing office lease before its expiration. While many leases include renewal options, exercising them without market analysis can be one of the most expensive mistakes tenants make.

A renewal should be treated as a new transaction, evaluated against current market conditions, space utilization, and long-term business strategy—not as a default continuation of the past.

Why Commercial Lease Renewals Matter Right Now

The office market didn’t just “bounce” into a new cycle—it repriced risk and value. That shows up in how landlords underwrite deals, how employees experience offices, and how finance teams judge real estate decisions.

-

Hybrid Work Changed Utilization, Not Just Attendance

It’s not simply “fewer days in-office.” It’s spikier demand (peaks midweek, valleys Monday/Friday), more cross-functional collaboration days, and greater sensitivity to layout quality. Two companies can have the same headcount and radically different space needs depending on scheduling norms, team structure, and meeting behavior.

-

Vacancy Is Elevated, But Leverage Is Uneven

Many submarkets have plenty of availability, yet best-in-class buildings can still command stronger pricing and terms because they’re winning the “flight to quality.” That means renewals aren’t about “rent down” everywhere—they’re about choosing whether you’re paying for quality, flexibility, or pure cost, and negotiating accordingly.

-

The Real Gap Is Between “Contracted Rent” And “Market Reality”

A lot of tenants are sitting in leases negotiated under very different assumptions—growth projections, in-office expectations, and rent trajectories. Even when face rent looks acceptable, the total economics can drift: escalations compound, operating expenses rise, and older leases often lack modern flexibility (givebacks, expansion rights, sublease freedom, termination options).

-

Capital Markets And Building Health Now Matter To Tenants

Lease decisions used to be mostly about space and price. Now, tenants also have to think about landlord capacity to fund improvements, maintain services, and execute capital work. Building-level financial stress can translate into operational friction—or become leverage if you understand the owner’s incentives and timing.

-

Costs To Move Or Build Out Are Higher And More Variable

The renewal vs. relocate math isn’t just about rent. It’s about TI dollars, construction timelines, permitting risk, downtime, furniture/IT, and change management. In many cases, the “cheapest rent” option loses once you model the full cost and risk to execute.

-

Leadership Teams Want Finance-Grade Decisions

CFOs and executives increasingly expect real estate choices to be justified like any other investment: NPV impact, scenario planning, risk tradeoffs, and measurable utilization—not anecdotes like “people like the building.” That’s why the renewal window is so valuable: it’s one of the few times you can make a high-impact change with a clear decision point and negotiation leverage.

Net: the renewal window is one of the only moments where tenants can reset economics, right-size intelligently (not blindly), and rebalance portfolios—but only if they have visibility into things like remaining lease NPV, true utilization by site, comparable deal terms, and relocation scenarios (exactly the inputs tools like REoptimizer® are built to centralize).

The Four Most Common Commercial Lease Renewal Mistakes

1. Treating A Renewal Like A Paperwork Exercise

Tenants often assume that staying put is the safest option. Familiarity with the space, landlord, and commute patterns can create a false sense of security.

But renewing without analysis often means:

-

Overpaying above market rent

-

Carrying excess or poorly configured space

-

Locking into outdated lease terms and escalations

A renewal is a multi-year financial commitment and should receive the same scrutiny as a new lease—sometimes more.

2. Negotiating Without Understanding True Portfolio Economics

Many tenants negotiate renewals in isolation, looking only at:

-

Current rent

-

Renewal option language

-

Short-term savings

What’s often missing is visibility into how each lease performs inside the broader portfolio.This is where modern portfolio analytics change the game.With REoptimizer®, tenants can:

-

See the remaining Net Present Value (NPV) of each lease

-

Understand how future rent escalations compound over time

-

Compare the cost of staying versus relocating or restructuring

-

Identify which locations are financial outliers

Without this data, tenants negotiate blind.

3. Ignoring Utilization And Right-Sizing Opportunities

Excess space is one of the largest hidden costs in corporate real estate.

Many organizations no longer need the same footprint they signed for years ago—but that doesn’t always mean a simple reduction. The real opportunity lies in nuanced optimization. REoptimizer® enables tenants to:

-

Measure utilization at each site

-

Identify underused locations and redundant footprints

-

Evaluate whether satellite offices can be consolidated

-

Model scenarios like combining locations into a single, higher-quality hub

Instead of asking, “How much space do we cut?” The better question is, “How should our space actually work?”

4. Failing To Leverage The Market With Real Alternatives

Landlords negotiate differently when they know a tenant has credible options.

However, “alternatives” only create leverage if they are:

-

Comparable in quality and function

-

Priced accurately on a net-effective basis

-

Evaluated alongside renewal economics

REoptimizer® allows tenants to:

-

Match renewal terms against true market comparables

-

Compare new locations side-by-side with the existing lease

-

Model total occupancy costs across multiple scenarios

-

Create defensible competition for their tenancy

This transforms negotiations from reactive to strategic.

How REoptimizer® Changes The Commercial Lease Renewal Process

Traditional renewal planning relies on spreadsheets, fragmented data, and anecdotal market knowledge. REoptimizer® replaces that with a centralized decision platform.

Portfolio-Level Intelligence

Utilization And Strategy Alignment

-

Site-level utilization insights

-

Identification of consolidation and combination opportunities

-

Alignment with hybrid work policies and growth plans

Market And Scenario Comparison

-

Comparable lease benchmarking

-

Renewal vs. relocation modeling

-

Side-by-side evaluation of multiple options

Faster, Better Decisions

-

Clear visuals for executives and finance teams

-

Scenario modeling that supports internal buy-in

-

Data-backed negotiation strategies

The result: better outcomes with less guesswork.

When Should You Start Planning A Commercial Lease Renewal?

For most office tenants, renewal planning should begin 18–36 months before lease expiration, depending on portfolio size and complexity.

Starting early allows tenants to:

-

Identify leverage well before deadlines

-

Avoid costly extensions or rushed decisions

-

Use time as a negotiating advantage

-

Align real estate decisions with broader business planning

With tools like REoptimizer®, early planning becomes practical—not overwhelming.

The Bottom Line: Renewals Are Where Portfolios Are Won Or Lost

Commercial lease renewals are no longer about simply staying or leaving. They are about optimizing an entire portfolio—financially, operationally, and strategically.

Tenants who succeed will:

-

Treat renewals as new investments

-

Use data, not assumptions

-

Understand utilization at a granular level

-

Leverage market alternatives intelligently

-

Equip themselves with the right technology and representation

REoptimizer® doesn’t replace strategy—it enables it.Want to see how it can level up your portfolio? Book a demo today.

Book a Demo

Commercial Lease Renewal FAQs

When Should I Start Planning A Commercial Lease Renewal?

Most tenants should begin planning 18–36 months before lease expiration. Starting early gives you time to benchmark the market, build internal alignment, and create real negotiating leverage—without risking costly extensions or rushed decisions.

Should I Exercise My Renewal Option Or Renegotiate?

A renewal option is not automatically the “best deal.” Many option clauses reset only some terms (or lock in above-market economics). The safest approach is to price the option against market comparables and alternative locations, then choose the path with the best net-effective outcome.

How Do I Know If I’m Overpaying Rent?

You’re likely overpaying if your lease was signed in a stronger market and has compounding escalations, or if comparable buildings are offering better economics (rent, concessions, flexibility). The most reliable test is a true side-by-side comparison of:

-

Base rent + escalations

-

Operating expenses (and caps)

-

Tenant improvement allowance

-

Free rent / abatement

-

Move, build-out, and downtime costs

What Are The Biggest Negotiation Levers In A Lease Renewal?

Most renewal wins come from negotiating the full value stack, not just rent:

-

Tenant improvement (TI) dollars

-

Free rent / rent abatement

-

Operating expense protections (caps, exclusions, audit rights)

-

Flexibility clauses (expansion, contraction, termination options)

-

Parking, signage, and amenities

-

Sublease and assignment rights

Can I Reduce My Square Footage During A Renewal?

Often, yes—but it depends on building layout, the landlord’s leasing strategy, and timing. Many tenants pursue:

-

A direct reduction (smaller suite)

-

A re-stack within the building

-

A blend-and-extend with resizing

-

A partial giveback paired with a longer term

The key is to make the new footprint worth it to the landlord (term, credit, stability, or avoided vacancy risk).

How Do I Measure Office Utilization Before A Renewal?

Utilization should reflect how people actually use the space—by day, department, and peak periods—rather than assumptions. Measuring utilization helps you avoid renewing excess space and can reveal opportunities like consolidating teams, redesigning layouts, or combining nearby satellite locations.

What Is Remaining Lease NPV And Why Does It Matter?

Remaining lease NPV (Net Present Value) estimates the value of your remaining lease obligations in today’s dollars. It helps decision-makers compare options like:

-

Renewing vs. relocating

-

Downsizing vs. reconfiguring

-

Shorter term vs. longer term

-

Paying more now vs. avoiding higher long-term cost

NPV makes “stay vs. go” a finance-grade comparison instead of a gut call.

How Can REoptimizer® Help With Lease Renewals?

REoptimizer® helps tenants turn renewals into a portfolio optimization decision by enabling you to:

-

See the remaining NPV of each lease

-

Understand escalation exposure and term risk

-

View utilization by site to identify right-sizing opportunities

-

Spot nuanced consolidation plays (like combining satellite locations)

-

Match market comparables and benchmark deal terms

-

Compare renewal vs. new location scenarios side-by-side

How Do I Create Leverage In A Renewal Negotiation?

Leverage comes from credible alternatives and a clear plan. The best path is to:

-

Identify 2–4 realistic relocation options

-

Compare them against the renewal on a net-effective basis

-

Communicate that you can execute (not just “shop around”)

-

Keep options alive until the renewal is fully documented

Do I Need A Tenant Representative For A Renewal?

It’s not required, but it’s often the difference between an average deal and an optimized one. A tenant rep brings:

-

Market benchmarks and comp visibility

-

Negotiation strategy and leverage building

-

Term and legal-risk awareness

-

Time savings and process control

What If I Wait Too Long To Start The Renewal Process?

If you wait, you risk:

-

Losing renewal rights or negotiation windows

-

Paying for expensive short-term extensions

-

Accepting unfavorable terms due to time pressure

-

Missing better market opportunities

Time is leverage—starting early protects it.

Commercial leases don’t just have “terms.” They have deadlines—and missing one can cost you renewal rights, expansion space, tenant improvement dollars, or trigger default. This guide breaks down the most important lease dates to track, what they mean, and how to stay protected.

Quick Answer: What Are The Key Dates In A Commercial Lease?

The most important dates in a commercial lease usually include:

-

Delivery Date (when the space must be ready)

-

Lease Commencement Date (when the lease legally starts)

-

Rent Commencement Date (when billing begins)

-

Rent Escalation Dates (when rent increases)

-

Option Notice Windows (renew, terminate, expand, downsize)

-

CAM / Operating Expense Reconciliation & Audit Deadlines

-

Insurance & Certificate of Insurance (COI) Renewal Dates

-

Security Deposit / Letter of Credit (LOC) Expiration & Step-Down Dates

-

Assignment/Sublease Consent & Recapture Deadlines

-

Restoration, Surrender, and Move-Out Dates

-

Termination Date and Holdover Period Triggers

If you track nothing else, track these.

Why Key Lease Dates Matter (And Why Tenants Lose Money)

Most commercial leases make it 100% the tenant’s responsibility to:

-

remember critical dates, and

-

deliver notice exactly the way the lease requires.

Landlords don’t have to remind you. And many are perfectly happy if you miss a renewal window, lose a right to expand, or default on an administrative technicality.

The Portfolio Problem: One Lease Is Manageable—Twenty Isn’t

Tracking lease dates for a single location is hard enough. Tracking them across an entire portfolio is where tenants get hurt.

Because once you scale to multiple sites, you’re no longer managing a “lease.” You’re managing a deadline ecosystem, with hard stops and serious liability.

One missed renewal window can wipe out your leverage. One missed CAM audit deadline can lock in overcharges. One delayed delivery can force holdover tenancy with penalty rent and potential damages. And spreadsheets? They don’t protect you when the real landmines are notice requirements—the exact method, address, timing, and proof that make or break your rights.

If you manage multiple locations, you need more than reminders—you need a system built for lease deadlines. REoptimizer® helps track critical dates, notice windows, escalations, and portfolio exposure in one place, so you don’t lose options, overpay rent, or get trapped in holdover. See how it can streamline your portfolio and book a demo today.

Book a Demo

The “Trigger Chain”: Dates That Control Other Dates

A best practice is to map your lease like a domino run:

Delivery Date → Lease Commencement → Rent Commencement → Escalations → Option Windows → Termination/Surrender

A surprising number of disputes come down to: which date triggered which obligation.

1. Delivery Date (When The Space Must Be Ready)

Definition: The date the landlord must deliver the premises in the condition required by the lease.

What Tenants Should Tie To The Delivery Date

-

Required Condition Standard (code-compliant, clean, safe, systems working)

-

Utilities/Services Live (HVAC, electric, water, internet readiness)

-

Punch List Process (walkthrough, deficiency list, cure timeline)

-

Remedies If Late (rent delay, per diem penalties, termination right, reimbursement)

Why It’s Critical

A late delivery can force a business into:

Tenant tip: Your lease should define “delivered” clearly—otherwise a landlord can argue the space is “ready” when it’s not ready for your operations.

2. Lease Commencement Date (When The Lease Legally Starts)

Definition: The date the lease term officially begins.

This date often controls:

-

The Lease Term End Date

-

When Options Can Be Exercised

-

When Certain Obligations Begin (insurance, maintenance responsibilities, reporting)

Watch for: “earlier of” and “later of” language. Many leases say commencement is the earlier of occupancy or a set date—meaning you might trigger obligations by moving in early.

3. Rent Commencement Date (When You Start Paying)

Definition: The date rent starts accruing—often different from lease commencement.

Common Rent Commencement Structures

Free Rent Isn’t Always Free

Many leases make free rent conditional:

-

Base Rent Only (not CAM/operating expenses)

-

Abatement Ends If You Default

-

The “Free Months” Extend The Lease Term (e.g., 120 months of paid rent becomes 132 months total)

4. Rent Escalation Dates (When Rent Increases)

Definition: The recurring date rent increases (often annually).

Common Rent Escalation Types

-

Fixed Percentage Increases

-

CPI Adjustments (with caps/floors sometimes)

-

Stepped Increases (pre-set schedule)

-

Fair Market Adjustments (typically at renewal)

Why It Matters

Escalations are cumulative—they compound across long terms. A “small” clause can become a major cost driver over 7–15 years.

Tenant tip: Track escalation dates and the formula inputs (CPI base year, index month, cap/floor, rounding rules).

5. Option Notice Windows (Renew, Terminate, Expand, Downsize)

Definition: A set window when a tenant must give notice to exercise a right.

This is the #1 category tenants miss.

Options Usually Include

-

Renewal / Extension Options

-

Early Termination Options

-

Contraction Or Downsize Options

-

Expansion Options (ROFO/ROFR or fixed space options)

The Real Trap: Notice Rules

A tenant can “send notice” and still lose the right if:

-

Notice Method Is Wrong (email not allowed)

-

Sent To The Wrong Address

-

Missed The Window By A Day

-

Lacked Required Enclosures (financials, proposed terms)

Best practice: Track both:

6. Right of First Offer (ROFO) (Expansion Timing Advantage)

Definition: Before the landlord markets certain space, they must offer it to the existing tenant first.

Key dates to track:

If you can’t respond fast, you lose the shot.

7. Right of First Refusal (ROFR) (Match A Third-Party Deal)

Definition: Landlord can market space, but must let the existing tenant match the third-party deal.

Key dates to track:

Practical difference: ROFR can slow deals, but gives the tenant a chance to “match” a real market offer.

8. CAM / Operating Expense Reconciliation And Audit Deadlines

This is one of the most expensive “hidden” date categories.

Key dates:

-

Annual Reconciliation Statement Delivery Date

-

Tenant Dispute Window (often 30–180 days)

-

Audit Request Deadline

-

Payment Due Date For Under-Billings

Tenant tip: If you miss the dispute window, many leases treat the landlord’s statement as final—even if it’s wrong.

9. Insurance Renewal And COI Deadlines

Many leases require:

-

Specific Coverage Types/Limits

-

Landlord Named As Additional Insured

-

COIs Delivered Annually or upon renewal

Key dates:

-

Policy Expiration

-

COI Delivery Deadline

-

Renewal Bind Date

Missing this can be a technical default even if you’re otherwise a perfect tenant.

10. Security Deposit / Letter Of Credit (LOC) Dates

If you have an LOC, date tracking is non-negotiable.

Key dates:

Tenants get defaulted all the time for simply failing to renew an LOC on time.

11. Assignment / Sublease Consent And Recapture Deadlines

If you plan to sublease or assign the lease:

Key dates:

-

Tenant Request Submission Date

-

Landlord Response Deadline

-

Recapture Election Deadline

-

Execution Deadline For Sublease/Assignment

12. Restoration, Surrender, And Move-Out Dates (The Endgame)

The termination date isn’t your only end-of-lease date.

Key dates:

-

Restoration Notice Deadline (landlord tells you what must be removed)

-

Decommission Start Date (IT, cabling, supplemental HVAC, signage)

-

Final Walkthrough Date

-

Key Return/Access Shutoff Date

-

Move-Out Completion Deadline

13. Termination Date And Holdover Trigger

Definition: The date the lease ends and you must be fully out.

If you stay past it, you can trigger:

Tenant tip: Track a move-out runway (60–180 days out) so surrender doesn’t become a crisis.

The Tenant’s Critical Date System (Best Practice Checklist)

To make lease date tracking actually work, log each critical date with:

-

Deadline Date

-

Earliest Notice Date (if applicable)

-

Notice Method + Address(es)

-

Owner (primary person responsible)

-

Backup Owner

-

Proof-Of-Delivery Requirement

-

Linked Lease Clause Reference

A calendar reminder alone is not enough if your lease requires certified mail to a specific address by a specific time.

FAQ: Key Dates In Commercial Leases

What is the most important date in a commercial lease?

For most tenants: Rent Commencement Date (when payments begin) and option notice deadlines (renewal/termination). These two categories drive the biggest financial outcomes.

Are lease dates the tenant’s responsibility?

In most leases, yes. The tenant is typically responsible for tracking dates and providing proper notice exactly as required.

What happens if I miss a renewal notice deadline?

You may lose the renewal option entirely and be forced to vacate or renegotiate at a much higher rent—often with reduced leverage.

Never Miss a Key Date

Tracking critical dates is a business imperative—but it’s only one part of optimizing a lease.The real advantage comes from seeing every deadline, notice window, escalation, and expansion right across your entire portfolio—before it turns into a costly mistake.

REoptimizer® is built to do exactly that: centralize your lease obligations, surface upcoming risk, and keep you ahead of renewals, CAM deadlines, LOC expirations, and holdover exposure. If you’re still relying on spreadsheets and calendar reminders, you’re one missed notice away from losing leverage.

Book a REoptimizer® demo to see how portfolio-wide critical date management actually works—and how much money and risk you can pull back into your control.

Book a Demo

CRE transaction management software is a platform that helps you run commercial real estate deals end-to-end—from requirements and site selection through negotiations, approvals, documentation, and close—so every deadline, cost, and decision is tracked in one place (instead of living in spreadsheets, inboxes, and scattered folders).

REoptimizer® is built for exactly this: centralizing portfolio data and automating reporting, alerts, and workflows so teams can move faster and negotiate from a stronger position.

Who Can Benefit from CRE Transaction Management Software?

If your organization has more than a few locations—or multiple deals happening at once—transaction management software becomes a necessity, not a “nice to have.”

Typical users include:

- Corporate Real Estate (CRE) And Portfolio Strategy teams managing growth, consolidation, relocations, and renewals

- Finance / FP&A tracking budgets, approvals, and forecast vs. actual

- Legal managing LOIs, redlines, and compliance documentation

- Operations / Workplace / Facilities aligning space with headcount and utilization

- Executives who need a clear view of deal risk, savings, and timing

REoptimizer® is positioned for enterprise teams dealing with complexity—replacing “spreadsheets, siloed systems, and manual processes” with a single system of record.

What CRE Transaction Management Software Does

At its core, CRE transaction management software helps you:

- standardize the process (repeatable workflows and checklists)

- coordinate people and deadlines (ownership, reminders, accountability)

- organize documents (versions, approvals, audit trail)

- track costs line-by-line (so overages don’t hide in the noise)

- report in real time (so leadership isn’t waiting on a “Friday spreadsheet”)

REoptimizer® adds a key layer: it’s designed to help teams compare deal economics against comps and benchmarks and generate reporting fast with templates—because the real money is won or lost in the details.

Where It Fits (And Why It’s Not The Same As Lease Management)

A simple way to think about the lifecycle:

Before The Deal: Strategy And Site Search

This is where teams define what they need and evaluate options. REoptimizer® supports this with KSDs (Key Site Drivers) and tools like CRESiteIQ™, built to analyze markets, compare sites, and visualize opportunities. More on in the next section…

During The Deal: The Transaction Itself

This is the heavy-lift phase: comps, negotiations, approvals, legal, due diligence, and getting to signature/close.

After The Deal: Lease Management

Lease management is what happens after execution—tracking key dates like renewals, expirations, options, and escalations. REoptimizer® content points out how missed key dates can create real cost and risk at portfolio scale.

Bottom line: lease management is “operate what you signed.” Transaction management is “control what you sign.”

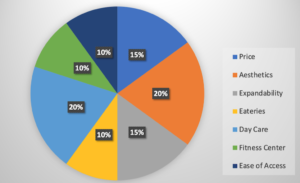

What Are KSDs?

KSDs (Key Site Drivers) are the criteria that define what “best location” means for your business—then you weight and score them so every option can be compared objectively (not emotionally, not anecdotally, and not based on whoever toured last). Consider them your highly unique KPI’s.

REoptimizer® uses KSDs to score each property in real time and calculate a final weighted score per building, instantly ranking your top contenders side-by-side.

Why KSDs Are Invaluable (And Why Teams That Use Them Win More Often)

They Turn “Opinions” Into A Repeatable Decision System. Without KSDs, site selection usually sounds like:

- “This one feels right.”

- “The price is good, but…”

- “Leadership likes that submarket.”

KSDs force alignment upfront. You define the “must-haves” and “deal-breakers” before you tour, so your team is evaluating every property against the same standard.

They Help You Compare The Stuff That’s Hard To Measure

Price and square footage are easy. The real risk is everything else:

- Workforce access and commute patterns

- Truck access and delivery windows

- Power capacity and future expansion needs

- Column spacing, dock ratios, clear height (industrial)

- Customer proximity and logistics cost impacts

- Rent vs market comps (and trend direction)

- Total Occupancy Cost (rent + CAM/NNN + taxes + insurance + utilities)

- Current utilization vs required utilization (desk sharing, peak days)

- Adjacency needs (teams that must be near each other

- Layout efficiency (loss factor, usable vs rentable SF)

REoptimizer’s® KSD approach is designed specifically to capture those “hard-to-quantify” drivers and make them scorable—so the best site isn’t just the cheapest, it’s the lowest total cost of occupancy and best operational fit.

They Save Time By Eliminating Bad-Fit Tours Early

One of the most expensive mistakes companies make is touring before they’ve defined what matters most. REoptimizer calls this out directly: teams waste time touring warehouses without clear KSDs—then end up revisiting assumptions mid-process. When KSDs are set first, you filter faster and only tour buildings that can realistically win.

They Strengthen Negotiations Because You Know Your Leverage

When you can prove (with scoring) that multiple buildings meet your needs, negotiations change:

- You’re selecting from the strongest options and negotiating from leverage.

- You can back up concession requests with evidence, using comps plus the operational requirements that drive real value.

- You reduce waste by not paying extra for features that don’t move the needle for your business.

Because Reoptimizer® scores contenders side-by-side and ranks them instantly, your team walks into negotiation with clarity: what matters, what doesn’t, and what you can walk away from.

They Keep The Portfolio Aligned With The Business (Not Just The Deal)

The biggest value of KSDs isn’t picking a building—it’s ensuring every location decision supports the business:

- growth plans

- service levels

- labor strategy

- cost targets

- utilization and waste reduction

REoptimizer’s® broader positioning is exactly this: giving teams visibility into overspending and underused space, then translating that into action through dashboards and metrics—so site decisions don’t live in a one-time spreadsheet, they become an operational advantage.

How REoptimizer® Makes KSDs Practical (Not Just A Worksheet)

Here’s the difference between “having KSDs” and using KSDs:

- Score Each Property In Real Time: As you evaluate a site, REoptimizer scores how well it delivers on each KSD—immediately, even while touring.

- Rank Overall Suitability: REoptimizer calculates a weighted score per building and instantly highlights top contenders.

- Expand Site Intelligence With CRESiteIQ™: For location strategy, CRESiteIQ™ helps define what matters and compare sites using many data points (example categories include demographics, income, fuel costs, population trends, and more).

Why Your Portfolio Needs CRE Transaction Management Software

In CRE, savings (or losses) don’t come from “being organized.” They come from making better decisions earlier and catching issues before they get locked into the deal.

Transaction management software helps you:

- Avoid missed deadlines that weaken leverage

- Prevent “death by a thousand line items” (fees, escalations, TI, concessions, operating assumptions)

- Benchmark against comps instead of negotiating blind

- Expose underutilization and waste so the portfolio improves over time

REoptimizer® specifically highlights eliminating wasted effort by centralizing data and automating alerts/workflows—so teams spend time on strategy, not chasing updates.

Why Spreadsheets Don’t Work For Transaction Management

Spreadsheets are fine for a single deal. They fail when you’re handling:

- Multiple stakeholders and approvals

- Changing versions of assumptions and documents

- Market comps, benchmarks, and reporting needs

- Utilization/waste measurement across a portfolio

That’s why REoptimizer® focuses on replacing spreadsheets and siloed tools with a centralized platform and automation.

FAQs

What Is CRE Transaction Management Software?

It’s software that manages the full commercial real estate deal process—tasks, deadlines, documents, approvals, and costs—from strategy through close, so nothing falls through the cracks.

How Is CRE Transaction Management Different From Lease Management?

Lease management is post-signature administration (key dates, escalations, compliance). Transaction management covers the whole process where the economics and terms are created.

Who Needs CRE Transaction Management Software?

Any company with a multi-location portfolio or frequent transactions—especially when deals involve finance, legal, operations, and leadership approvals.

How Does REoptimizer® Help With CRE Transaction Management?

REoptimizer® helps enterprise teams centralize portfolio data and automate reporting, alerts, and workflows—and supports site selection and deal evaluation with KSD scoring and related tools.

What Is CRESiteIQ™?

CRESiteIQ™ is a REoptimizer® tool for site selection, built to analyze markets, compare sites, and visualize opportunities in one platform.

What Are Key Site Drivers (KSDs) In Commercial Real Estate?

KSDs are your business’s weighted location criteria—used to score and compare properties objectively so you can identify the best-fit sites faster.

Why Should KSDs Be Weighted?

Because not all criteria matter equally. Weighting prevents teams from over-prioritizing “nice-to-haves” (or the loudest opinion) over the drivers that actually impact cost, operations, and performance.

How Does REoptimizer Use KSDs?

REoptimizer® scores each property against your KSDs in real time and produces a final weighted score to rank contenders side-by-side.

Learn more about REoptimizer® today.

Learn More

Corporate tenants have spent the last two years hyper-focused on flexibility, operating costs, consolidation, and hybrid strategy. Fair—those issues matter. But while everyone was busy right-sizing their footprint, something far more consequential was happening behind the scenes: Landlords started defaulting. In large numbers.

In office markets, valuations have fallen by double-digits and weaker assets in certain urban cores are being written down far more aggressively.

Meanwhile, refinancing pressure on commercial loans is acute — making the need for tenant protections like the SNDA all the more urgent.

And here’s the part tenants tend to miss: If your landlord defaults, your lease is only as strong as the protections you negotiated—most importantly, the SNDA.

No SNDA? You can lose your space, your rights, your security deposit, and months of operational continuity. All because a lender’s mortgage lien outranks your leasehold interest.

This is not theoretical. This is the modern commercial real estate landscape.

Never Lease a Commercial Property Without an SNDA (Subordination Non Disturbance and Attornment) Agreement

An SNDA—Subordination, Non-Disturbance, and Attornment Agreement—is the legal document that decides who you are and what you are entitled to when a lender forecloses on the commercial property you occupy.

It governs the relationship between you (the tenant), the property owner, and the landlord’s lender, and it becomes critical when the landlord’s property ends up in a foreclosure sale.

Here’s the fast breakdown:

1. Subordination Provision: Where You Rank in the Food Chain

Every commercial loan comes with a lender’s security interest—a mortgage or deed of trust that automatically sits above your lease unless you negotiate otherwise.

If your lease is subordinate:

- The lender’s rights have priority.

- Your lease can be terminated in a foreclosure.

- You have no inherent right to stay in the leased property.

Without an SNDA, the hierarchy is simple: Mortgage > Lease.

And that means the lender can treat your existing lease as optional.

2. Non-Disturbance Agreement: The Clause That Saves You From Eviction

With a proper non-disturbance clause, the lender agrees not to throw you out when they take ownership. This ensures that:

- Your tenant’s rights remain intact.

- Your operations continue uninterrupted.

- Your workforce and equipment stay put.

- Your security deposit doesn’t vanish into a black hole of litigation.

In other words: If you’re paying rent, you stay. Period.

This is the core protection large corporate tenants need—but don’t always get.

3. Attornment Agreement: Accepting the New Landlord Without Losing Leverage

When lenders foreclose and become the new owner, the attornment provision requires the tenant to recognize them as the landlord.

It’s not as scary as it sounds. It keeps your lease alive and forces continuity.

But attornment must be paired with strong non-disturbance rights, or you’ve effectively agreed to report to a landlord who isn’t obligated to keep you.

Say Goodbye to Your Lease in a Foreclosure Sale

The “foreclosed office tower” storyline is becoming normal. Receivers are stepping in faster. Commercial lenders are enforcing rights more aggressively. Loan documents are driving the real outcomes—not the lease.

For corporate tenants, this means:

1. Traditional “Class A Stability” Assumptions Are Gone

Even trophy properties with strong sponsorship are facing refinancing hurdles and valuation write-downs.

2. Lease Provisions You Ignored Now Determine Survival

The SNDA is the difference between:

- Staying through foreclosure, or

- Being treated as collateral damage.

3. Without an SNDA, You Have No Real Negotiating Power With the New Owner

If a purchaser at foreclosure doesn’t like your rent schedule? Without an SNDA, they can simply remove you.

4. Security Deposits Become Vulnerable

If the landlord burns through them during financial distress, recovery becomes a legal war you don’t want to fund.

The Uncomfortable Truth: Most Tenants Don’t Realize They’re Exposed

You’d be shocked at how many large enterprises occupy commercial real estate without an SNDA. Why? Because historically:

- Landlords resisted offering it

- Lenders didn’t want to negotiate it

- Tenants assumed it was “standard enough”

And truthfully, the market was stable enough for the gamble to pay off—until now. Entering the 2026 landscape: Not having an SNDA is a material operational risk.

And CFOs are starting to ask about it—because they should.

Where the Leverage Has Shifted to the Tenant

Here’s the good news: This is one of the most tenant-favored markets in 30 years.

Vacancy is still elevated. Landlords are fighting to retain every square foot of occupancy. Commercial lenders want in-place rent streams. And because of that… This is the moment to negotiate SNDAs with actual teeth.

Corporate tenants can—and should—demand:

- Broader non-disturbance protections

- Lender’s consent on material landlord actions

- Security deposit tracking and safeguards

- Limits on lender step-in liability

- Clarification on insurance proceeds

- Preservation of key lease provisions through foreclosure

You have leverage. Use it before the next wave of landlord defaults hits.

What Savvy Corporate Tenants Are Doing Right Now

Modern occupiers aren’t waiting for their landlord to run out of cash. They’re conducting proactive portfolio reviews:

1. Auditing Every Lease for SNDA Presence & Quality

Not all SNDAs are equal. Some are window dressing; some actually protect you.

2. Requesting Lender Information on At-Risk Properties

Tenants can—and should—know who controls the mortgage loan, where it stands, and whether distress is imminent. This includes any loans that are crosscollateralized with other properties (that could be at risk.

3. Pre-Negotiating SNDA Terms Before Renewals or Expansions

A renewal without an SNDA in 2025 is… bold.

4. Stress-Testing Building Ownership Structures

If the borrower is exposed, you are exposed. It’s that simple.

5. Embedding SNDA Requirements in Corporate Real Estate Policy

Standardizing this prevents future oversight.

The Hard Reality: If Foreclosure Happens Without an SNDA, You’re Playing Defense

Here’s how it looks without protection:

- Lender forecloses

- Property ownership transfers

- Your lease becomes subordinate

- Leasehold interest = not guaranteed

- New landlord decides whether to honor it

- You negotiate from zero leverage

This is when tenants say things like:“We thought the lease protected us.” It doesn’t. The SNDA does. Given the scale of distress in commercial real estate, sophisticated tenants are treating SNDAs the way they treat:

- Audit rights

- Operating expense caps

- Relocation clauses

- Security instrument review

- Landlord’s lender notifications

Essential—not optional. As office assets continue to trade hands through workouts and foreclosure sales, the SNDA is becoming the backbone of tenant continuity.

The SNDA Isn’t Fine Print Anymore — It’s a Survival Strategy

The tenants who will actually win in this market are the ones who understand a simple truth: Real estate risk no longer lives with the landlord. It lives with the lender.

In the mortgage. In the lien. In the loan documents you never see.

That’s why the SNDA matters. It’s the only document that protects your leasehold interest when ownership changes, loans go sideways, or a foreclosure reshuffles the deck.

Most tenants only discover their exposure after a lender becomes their new landlord. REoptimizer® exists so you never end up in that position.

With REoptimizer®, you get the data visibility and risk intelligence your lease agreements don’t show you:

- Identify which landlords are most likely to default—before it becomes your problem.

- Flag leases missing critical protections across your entire portfolio.

- Model foreclosure and refinancing risk for every address you occupy.

- Benchmark terms market-by-market, so you know when to push harder.

- Strengthen your negotiating position with lenders, landlords, and purchasers.

- Protect business continuity in a market where ownership is changing faster than tenants realize.

This is no longer about optimizing space—it’s about securing it. Don’t wait for a lender to introduce themselves as your new landlord. Use REoptimizer® to lock down your position now—before the market forces your hand. Learn more today.

Learn More

If you manage a national footprint or oversee a large corporate real estate portfolio today, you already know this truth: flexibility is the most valuable resource you have left. And nothing in your lease agreement influences that flexibility more than the sublease clause—the single contract provision that can save you millions, or cost you millions, depending on how well it was negotiated.

In 2025–2026, subleasing is a strategic lever, a risk-control mechanism, and in many cases the only way to get ahead of space you no longer need.

But here’s the problem: most tenants don’t realize their sublease rights have been slowly weakened by landlord-friendly drafting, vague definitions, and “standard” language that’s anything but.

We’ll break down what’s changed, why it matters, and what corporate tenants must do now if they want their sublease agreement to work when it counts.

The Office Market Has Shifted (and So Has the Power Dynamic)

Let’s start with the facts.

- U.S. office vacancy fell to 18.8% in Q3 2025, marking the first year-over-year improvement since before the pandemic.

- National availability sits at 22.8%, with 3% of that being sublet space—still elevated but no longer ballooning.

- In several major markets (Los Angeles, Manhattan, Dallas), sublease supply has declined year-over-year for the first time in half a decade.

So what does this mean for enterprise tenants?

- Landlords are no longer in panic mode, and approvals are tightening.

- Lenders are more active, meaning landlords closely enforce anything tied to rights, approval, or income stability.

- Tenants still hold leverage, but that leverage now comes from contract clarity, not market distress.

In 2023, you might have gotten a “yes” simply because the building needed bodies. In 2025, you’ll get a “yes” only if your contract actually requires one. This is why the sublease clause is no longer back-of-the-binder material…

Negotiating Sublease Rights in the Original Lease

A properly negotiated clause gives the original tenant options:

- Reduce unused premises without paying for dead space

- Bring in a new tenant that covers rent payments

- Strategically downsize during M&A, restructuring, AI-driven shifts, or headcount changes

- Avoid being forced into a premature termination or buyout

But when the clause is weak?

- Every approval becomes discretionary

- The landlord gains veto power

- Timelines stretch

- Costs increase

- And if the subtenant fails to pay, the landlord comes straight to you

All while you continue to pay monthly rent, operating expenses, utilities, and maintenance under the master lease. That’s exposure, plain and simple.

The Five Most Dangerous Sublease Traps in Today’s Market

1. When The Landlord’s Consent to Sublease Is Not Consent

Most leases contain some version of:

“Landlord’s consent shall not be unreasonably withheld or delayed.”

But unless your clause defines:

- A strict number of days for the landlord to respond in writing

- What information the tenant must provide

- Whether non-response is deemed consent

- A limit on any administrative fee

…the landlord can simply sit on the request. And when you’re the one paying the monthly rent on unused space, every day costs money.

Watch for red flags:

- No defined response timeline

- No deemed-approval mechanism

- Requirements for “complete” information without defining what “complete” means

- A vague “review fee” that can morph into a profit center

This one seems small. It’s not. It’s the difference between a 30-day sublease process and a six-month one.

2. Use Restrictions That Shrink Your Subtenant Pool

Your original lease agreement likely has a permitted-use clause. But many landlords tie the sublease clause to that same narrow definition.

Examples include:

- “Use only for legal practice”

- “Office use for financial services”

- “Software development operations only”

Congratulations—you’ve now limited your subleased premises to a tiny sliver of the market.And the landlord typically reserves the right to deny subleasing to:

- Current tenants in the building

- Competitors

- Anyone the landlord is “in discussion with”

- Businesses outside your original use

This is one of the biggest killers of sublease deals. The modern tenant wishes for flexibility, but the contract says otherwise.

What you need instead:

- General office use as the permitted use for subtenants

- The ability to sublease to existing tenants unless there’s a documented conflict

- Removal of subjective terms like “in landlord’s sole discretion” or “active negotiations”

3. Economic Landmines: Recapture and Payment Flow from New Tenant

Here’s where the biggest financial damage occurs.

Recapture Rights

A shockingly large number of leases allow the landlord to terminate and recapture the space you want to sublet.

Sometimes that helps you. Sometimes it leaves you paying rent on space you no longer control.

Rent Payment Flow

Some leases force the subtenant to pay the landlord directly.

This is fine unless:

- The landlord misapplies payments