In the current commercial real estate landscape, the traditional lease audit is evolving. High-level corporate tenants are no longer just looking at their own square footage; they are looking at the property’s profitability.

For a tenant in a high-rise office or a sprawling warehouse, the landlord’s net operating income (NOI) is the heartbeat of the building. If that heartbeat flutters, your services—from security to climate control—are the first to suffer. Understanding how to calculate net operating income is no longer just for commercial real estate investors; it is a critical survival skill for portfolio managers.

Net Operating Income: The Tenant’s Risk Barometer

Net operating income is a fundamental valuation metric that measures a property’s income after deducting operating expenses but before financing and taxes. For a tenant, a healthy net operating income noi signifies a landlord who has the liquidity to reinvest in the building. Conversely, a shrinking NOI suggests a landlord who may be forced to cut corners on property management and essential operating costs.

Formula of Net Operating Income

To understand the financial health of your building, you must look at the formula of net operating income. At its simplest, the net operating income formula is:

While real estate investors use this to determine property value, tenants should use it to gauge operational performance. If the operating expenses are being artificially suppressed to prop up the NOI, the “deferred maintenance” bill is quietly growing—and you will eventually pay it through poor service or emergency escalations.

Gross Operating Income: More Than Just Tenant Rents

The first step in the noi calculation is determining the gross operating income. This represents the total revenue the property generates if it were fully functional, minus vacancy losses.

Gross income includes:

-

Tenant rents: The primary rental income.

-

Ancillary income: Revenue from parking fees, laundry services (in flex/mixed-use), and communications infrastructure.

-

Additional income: Vending, signage, and other revenue generated by the asset.

A landlord struggling with revenue growth in tenant rents may become aggressive with ancillary income or “nickel-and-diming” tenants on administrative costs.

Calculate Net Operating Income: Peeling Back the Expenses

To calculate NOI accurately, you must understand what qualifies as an actual cash expense. To arrive at the actual NOI, the property owner subtracts total operating expenses from the gross income.

Common operating expenses include:

-

Property taxes and income taxes (where applicable).

-

Property management fees and maintenance fees.

-

Insurance and utilities.

-

Operating costs for common areas.

Crucially, net operating income does not include financing costs, debt payments, interest payments, or capital expenditures. This is where tenants get tripped up: a building can have a “positive” net operating figure while still being in a cash-flow crunch due to high interest rates on its loan payments.

Net Income vs. Net Operating Income

It is vital to distinguish between net operating results and net income. While net operating income focuses on the property’s ability to generate cash flow from operations, net income is the “bottom line” after all business expenses, including interest expense and debt service payments.

If a landlord’s net income is negative despite a positive NOI, the property is likely over-leveraged. REoptimizer® helps you spot these discrepancies by comparing your building’s financial efficiency against comparable properties in the property’s market.

Cap Rate: How NOI Dictates Property Value

The cap rate (or capitalization rate) is the link between net operating performance and market value.

For the tenant, the cap rate is a signal of risk. A very high cap rate compared to the property type average may indicate a “value-add” property where the landlord is desperately trying to calculate noi increases by slashing property’s operating expenses. This often leads to a decline in operational efficiency and a poor tenant experience.

Calculate NOI to Predict Tenant Improvement (TI) Capacity

One of the most practical reasons to calculate net operating income is to assess a landlord’s ability to fund tenant improvements.

If the NOI calculation example for your building shows a tightening margin, the landlord likely lacks the net profit to offer competitive TI packages. They may even struggle to fund capital expenditures like elevator modernizations or HVAC overhauls, which are not included in noi but are essential for actual profitability.

Managing Multiple Properties with REoptimizer®

In a large-scale portfolio, manually reviewing the income statements for every rental property is impossible. This is where REoptimizer® becomes your most valuable asset. Our software allows you to:

-

Benchmark Operational Performance: Compare the operating profitability of your landlords across multiple properties.

-

Flag NOI Instability: Automatically detect if total operating expenses are out of sync with market trends.

-

Audit Property Management Fees: Ensure you aren’t overpaying for management fees that aren’t translating into operational efficiency.

-

Visualize Cap Rate Compression: Understand how property value shifts affect your landlord’s ability to maintain the investment property.

The REoptimizer® Advantage: Beyond the Spreadsheet

Don’t let your commercial real estate strategy be dictated by a landlord’s hidden financial strain. By understanding the formula of net operating income and utilizing REoptimizer® to monitor noi calculation trends, you shift the power dynamic back in your favor.

Are you ready to audit your portfolio’s true risk?

REoptimizer® provides the tools to see through the gross income and find the actual cash expense realities of your landlords. We help you identify the “red zone” properties where operating income is insufficient to support long-term property’s profitability.

Book a demo today for a data-driven portfolio review. Let us show you how to use NOI insights to secure better lease terms and protect your operational future.

A lease is more than just a contract for space; it is a multi-million dollar bet on your landlord’s financial stability. Whether you are managing a global warehouse network or a large-scale office portfolio, your operational continuity depends on the person across the table. And in today’s volatile market, the most critical “inspection” isn’t of the brick and mortar—it’s of the debt service coverage ratio (DSCR).

If your landlord is facing financial strain, your “Class A” experience can quickly dissolve into deferred maintenance, tax liens, or even the nightmare of a mortgage loan foreclosure. Here is how sophisticated real estate investors and corporate tenants use DSCR to protect their interests and why REoptimizer® is the essential tool for flagging these risks before they become your problem.

What is DSCR (Debt Service Coverage Ratio)?

The Debt Service Coverage Ratio (DSCR) is a financial metric used by many lenders to determine a borrower’s capacity to repay a loan. In simple terms, DSCR measures whether the property generates enough cash flow to cover loan payments.

For a tenant, the landlord’s DSCR is a barometer for their ability to maintain the property. If the ratio is too low, the landlord is likely “robbing Peter to pay Paul”—diverting your monthly rent to cover current debt obligations instead of essential operating expenses.

How to Calculate DSCR

To calculate DSCR, you divide the property’s net operating income (NOI) by its total debt service:

DSCR=Total Debt ServiceNet Operating Income (NOI)

- Net Operating Income (NOI): This is the rental income minus operating expenses (such as taxes, insurance, and maintenance).

- Total Debt Service: This includes all principal and interest payments on the mortgage loan.

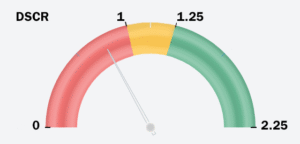

Benchmarks: What is an “Acceptable DSCR”?

Understanding the numbers is the first step in identifying financial difficulties in your landlord’s portfolio.

- DSCR > 1.25: This is the common industry standard for most real estate investors. It means the property generates 25% more income than is needed to cover loan payments.

- DSCR = 1.0: The property is just breaking even. One major vacancy or a spike in the annual interest rate could push the property into the red.

- DSCR < 1.0: A low DSCR indicates that the rental property’s cash flow is insufficient to cover mortgage payments.

The “Office Trap”: Why Office Tenants Face Higher Risk

For the office sector, a standard 1.25x DSCR is a starting point. Because office buildings have high tenant concentration and massive down payments required for tenant improvements (TIs), lenders often demand a minimum DSCR of 1.35x to 1.40x to approve an office mortgage loan.

The NOI Cash Flow Crisis

In the office world, Net Operating Income (NOI) is under siege. Unlike warehouse spaces with triple-net (NNN) leases that pass most costs to the tenant, office landlords often bear the brunt of:

- Skyrocketing Insurance Premiums: Insurance is a primary operating expense that has jumped 20–40% in some urban markets.

- Capital Expenditure (CapEx) vs. NOI: Standard DSCR calculation methods often exclude CapEx. However, an office landlord must spend heavily on lobbies and “amenitization” to attract tenants. If they are spending their cash on debt instead of CapEx, your building is effectively “dying on the vine.”

The Danger of Cross-Collateralization with a DSCR Loan

This is the “invisible” threat for a corporate tenant. Many large-scale office landlords use cross-collateralization, where multiple properties serve as collateral for a single mortgage loan (often called a blanket mortgage).

- The Scenario: Your office building might have a “healthy” individual DSCR of 1.30x.

- The Risk: If your landlord’s warehouse in another state loses its anchor tenant and its DSCR drops to 0.80x, the lender can trigger a cross-default.

- The Result: The lender could seize your building even if its performance is perfect. This “portfolio contagion” is why you must look beyond the single asset to the borrower’s capacity across their entire holdings.

Strategic Management: How to Audit Your Landlord

While you may not always have access to a landlord’s private tax returns, you can use the following factors to estimate their DSCR calculation:

- Analyze Market Rents: Use monthly rental income data for the property’s location to estimate the revenue.

- Monitor Tenant Turnover: If an office building has 20% of its leases expiring in the same period, the NOI is at extreme risk, which will tank the DSCR.

- Review Loan Terms: Research when the property was purchased. Loans from 2021 with low interest rates are now facing “refinancing cliffs” where the new annual interest rate will double the monthly payments.

Don’t Let Their Debt Become Your Disaster

In the current market, a strong DSCR is the ultimate sign of a reliable landlord. As a corporate tenant, you have the responsibility to understand the financial health of the entities housing your operations.

Are you ready to see the hidden risks in your CRE portfolio?

Stop guessing and start optimizing. REoptimizer® is the only transaction management software built to give corporate tenants an “institutional-grade” look at their landlords’ financial health. We don’t just help you manage leases; we help you audit the entities behind them.

Why REoptimizer® is Your Ultimate Shield:

- The Landlord Watchlist: Our platform flags landlords who are under financial strain based on real-time market data, debt maturity “cliffs,” and historical performance.

- Red & Yellow Flag Alerts: Instantly see which properties in your portfolio have a low DSCR or rising operating expenses that could trigger a service lapse.

- Cross-Collateralization Mapping: We reveal the hidden links in your landlord’s debt. If your warehouse is cross-collateralized with a failing office tower, REoptimizer® puts that risk on your dashboard before the lender sends a default notice.

- NOI Stress Testing: See how your building’s Net Operating Income holds up against shifting interest rates and inflation, giving you a clear picture of your borrower’s capacity.

Contact REoptimizer® today for a free portfolio health check. See exactly how our software can identify cross-default risks, flag high-risk debt obligations, and save you millions in hidden operational disruptions. Book a demo to see the difference it can have on your portfolio today.

Frequently Asked Questions: Navigating Landlord DSCR Risk

For corporate tenants, the financial health of a landlord is just as important as the physical health of the building. Below are the most common questions regarding the debt service coverage ratio and how it impacts your investment decisions.

How do you use the DSCR formula for a commercial landlord?

To perform a dscr calculation on a potential landlord, you need to estimate the building’s Net Operating Income (NOI) and divide it by the total debt service. While you may not have their exact ledger, you can use a dscr calculator approach by researching:

- Revenue: Estimated monthly rental income based on the building’s square footage and current market rates for the property’s location.

- Expenses: Standard operating expenses (usually 25–35% of gross income for office/warehouse) including taxes, insurance, and maintenance.

- Debt: Estimated principal and interest payments based on the property’s last recorded loan amount and the prevailing interest rate at the time of financing.

What is considered an acceptable DSCR for office vs. warehouse properties?

While many lenders accept a minimum DSCR of 1.25x for general investment property, the “safety zone” varies by asset class:

- Warehouse/Industrial: Because these often have stable, long-term NNN leases, a ratio of 1.20x to 1.25x is typically an acceptable DSCR.

- Office Space: Due to higher tenant turnover and the massive down payment required for tenant improvements (TIs), savvy tenants look for a landlord with a DSCR of 1.35x or higher. Anything lower suggests the landlord may lack the liquidity to fund your next office build-out.

How does a high interest rate impact a landlord’s debt service?

The annual interest rate is the most volatile component of the dscr formula. If a landlord has a floating-rate mortgage loan or an upcoming “refinancing cliff,” a 2% jump in the interest rate can instantly drop a healthy 1.30x DSCR to a sub-1.0 financial strain level. This is why REoptimizer® tracks market cycles—to warn you when your landlord’s borrower’s capacity is shrinking.

Can I use a DSCR loan calculator to estimate landlord risk?

Yes. A dscr loan calculator is a great “reverse engineering” tool. By inputting the property’s estimated value and the current loan to value (LTV) ratios, you can determine the maximum debt service the property can handle. If the resulting monthly payments are nearly equal to the estimated monthly rent, the landlord has zero margin for error.

What are the “other factors” that can tank a property’s DSCR?

Beyond the basic dscr calculation, tenants should watch for:

- Cross-Collateralization: If your office building is tied to a struggling retail mall in the same mortgage loan pool.

- Soft Market Conditions: Rising vacancy rates in the same period that expenses like insurance and taxes are increasing.

- Capital Expenditures: One-time costs (like a roof replacement) that aren’t in the NOI but drain the cash needed to repay the loan.

Proactive Portfolio Protection

In the high-stakes world of corporate CRE, information is your only shield. Don’t wait for a “For Sale” sign or a lapse in building services to realize your landlord is in trouble.

REoptimizer® gives you the data-driven edge to:

- Flag High-Risk Landlords: Identify owners with low DSCR and heavy debt obligations.

- Optimize Deal Terms: Use landlord financial weakness as leverage for better lease protections.

- Centralize Portfolio Health: See all your office and warehouse risks in one interactive dashboard.

High vacancy rates, a growing wave of landlord defaults, and a lingering oversupply of office space have created a rare market moment: corporate tenants can often secure better buildings on better terms—sometimes for less than they’d have paid years ago.

But there’s a catch. Distressed assets are a major risk and navigating this environment should not be taken lightly for tenants. To make it more difficult, they’re not waving a white flag announcing the trouble. There can be real risk hiding behind an address. This includes the landlord’s broader debt exposure, watchlist status, and cross-collateralized loans that can drag “healthy” properties down with “sick” ones.

That’s why today’s winners aren’t guessing—they’re using REoptimizer® to uncover which landlords are on a watchlist, what loans are at risk, and which properties may be tied together behind the scenes.

In this article, you’ll learn how to:

-

Define what makes a commercial property “distressed”

-

Understand why distressed buildings can be strategically valuable for tenants

-

Identify risk and opportunity using landlord watchlists and cross-collateral exposure

-

Negotiate smarter by knowing what the landlord can’t afford to lose

And while distressed properties aren’t automatically “bad,” the danger is leasing from a landlord whose portfolio-level risk can create operational, financial, and continuity headaches for your business. Let’s discuss.

What Defines a Distressed Commercial Property?

A commercial property is “distressed” when financial or operational pressure makes it undervalued, unstable, or at elevated risk of default, foreclosure, or forced restructuring. Common indicators include:

Loan Distress and Servicing Red Flags

-

Delinquencies (missed or late payments)

-

Special servicing transfers (a major warning sign that the lender has stepped in)

-

Weak DSCR (Debt Service Coverage Ratio) where income doesn’t comfortably cover debt payments

-

As a rule of thumb, DSCR below ~1.0–1.25 often signals heightened risk, depending on the lender and asset profile.

-

High Vacancy and “Silent Vacancy”

-

Vacancy rates: obvious indicator of weaker tenant demand and unstable cash flow

-

Under-occupancy (“dormant vacancy”): space that looks occupied today, but is functionally vacant the moment a lease rolls.

Market Saturation

Oversupplied submarkets create fire-sale leasing conditions—especially in older classes of inventory. Distress, in other words, isn’t just about a building. It’s about cash flow + debt + market pressure converging in a way that reduces stability and increases urgency.

How to Identify Distressed Properties (and Risky Landlords) the Smart Way

Whether you want to avoid distressed assets, audit your current portfolio, or capitalize on tenant-favorable conditions, your method matters. A quick “market scan” won’t cut it anymore.

1. Use Distress and Watchlist Intelligence (Not Just Comps)

Traditional leasing analysis is backwards-looking. Watchlist intelligence is forward-looking.

With REoptimizer®, you can evaluate a target building through the lens that matters most:

-

Is the landlord on a watchlist?

-

Is the loan associated with the property showing elevated risk signals?

-

Are there other properties in the owner’s portfolio that appear connected (cross-collateralized) to loans under stress?

This is how corporate tenants avoid signing a long-term lease under a landlord who may be forced into reactive decision-making.

2. Leverage CMBS and Loan-Performance Data for Negotiation Power

Platforms like Trepp and KBRA aggregate CMBS and credit performance data that can help identify pressure points. Key metrics to watch include:

-

Special servicing and delinquency flags

-

High LTV (Loan-to-Value): often signals thin equity and urgency to stabilize cash flow

-

Debt yield weakness: low debt yield indicates lenders may view the loan as higher risk

-

NOI declines and cap rate pressure: signals reduced income stability

Even if you don’t live in these datasets day-to-day, REoptimizer®’s watchlist visibility helps translate “credit stress” into real-world leasing decision support.

3. Track Market Indicators (At the Submarket Level)

Big headline vacancy numbers don’t negotiate your lease—micro conditions do.

Look at:

-

Vacancy by class (A vs. B/C)

-

Vacancy composition (shadow vacancy, near-term rollovers)

-

Net absorption trends by submarket, not just city-wide averages

-

Employer movement patterns and infrastructure investment

The best opportunities often sit in the gaps—where a submarket is weak overall, but a specific pocket is still strategically valuable.

Risks When Leasing a Distressed Building

The biggest risk is not the space—it’s the landlord’s financial position and what’s happening across their portfolio.

Key tenant risks:

-

Service degradation (maintenance delays, understaffed management)

-

Deferred capex (systems fail, upgrades stall)

-

Ownership disruption (sale, receivership, lender control)

-

Lease administration issues during restructures

Most importantly: a building that looks “fine” can still be risky if the owner is exposed elsewhere.

Why Distressed Properties Can Be a Strategic Advantage (If You Avoid the Wrong Risks)

Distressed office environments are brutal for landlords and lenders—but that stress can translate into meaningful tenant upside:

Cost Savings and Concessions

Distressed owners are often more willing to offer:

-

Lower base rent

-

Bigger TI (tenant improvement) allowances

-

Longer rent-free periods

-

Flexibility on term length, options, signage, etc.

Better Space for the Same (Or Less) Money

This is where tenants can “trade up” into stronger locations or higher-class assets at reduced effective rates—boosting brand perception and talent attraction.

Negotiating Leverage

A landlord under pressure values predictable cash flow. A strong corporate lease can be the difference between stabilizing the asset—or sliding further toward default.

But here’s the part most tenants miss:

What Lease Protections Should Tenants Request in Distressed Situations?

If a property or owner shows financial stress, tenants should prioritize operational continuity and risk containment, not just pricing. High-value protections to negotiate:

-

Stronger landlord maintenance/service obligations

-

Clear remedies and cure periods

-

Delivery and TI completion guarantees

-

Operating expense transparency / caps (where feasible)

-

Rights tied to building disruption events (practical protections if conditions deteriorate)

The Hidden Risk: A “Fine” Building Owned by a Watchlisted Landlord

Even if your building looks safe, the owner’s portfolio may not be.

Landlords frequently use financing structures that can connect multiple properties to the same debt obligation. In cross-collateralized loans, several properties serve as collateral for a single loan (or interconnected loans). If one asset deteriorates, it can raise risk across all linked assets—even the ones performing well.

That can create tenant risks like:

-

Deferred maintenance or degraded building services

-

Slower response times from ownership/management

-

Surprise ownership changes or lender intervention

-

Disrupted capital plans (elevators, HVAC, lobby, build-out approvals)

-

Lease administration complications during restructures

Where REoptimizer® Changes the Game

Instead of relying on surface-level deal comps and a building tour, REoptimizer® helps tenants:

-

See which landlords are on a watchlist

-

Identify which properties appear tied to debt at risk of default

-

Spot potential cross-collateral exposure so you can avoid getting trapped in a portfolio-wide problem

This means you can pursue “distressed opportunity” while filtering out “distressed operator risk.”

How to Approach Negotiations Once You’ve Found a Target

When REoptimizer® shows ownership pressure (watchlist status, risky debt, portfolio flags), you don’t just “ask for a better deal.” You negotiate around what the landlord must solve.

High-impact asks commonly include:

-

Larger TI allowances (or turnkey build-outs)

-

Longer free rent and phased commencement

-

Stronger landlord work-letter commitments

-

More protective defaults/cure rights

-

Expanded termination/relocation rights (where appropriate)

-

Audit rights / transparency improvements in operating costs

Knowing the landlord’s risk profile helps you structure terms that protect your operations—not just your rent number.

Bottom Line: Distressed Can Be a Win—If You Can See the Landlord Risk

Distressed leasing environments create real opportunity for corporate tenants. But the smartest move isn’t simply finding a “cheap Class A building.”

It’s finding the right building owned by the right landlord, with a clear view into:

-

watchlist risk,

-

loan stress,

-

and cross-collateral exposure that could blindside you mid-lease.

That’s exactly what REoptimizer® is built for: turning opaque landlord risk into actionable intelligence—so your relocation is an advantage, not a gamble. Learn more about how to utilize REoptimizer® for portfolio wide visibility and strategic moves that will keep your portfolio safe for years to come.

In the world of corporate real estate, there are certain things everyone talks about—market cycles, hybrid work, construction delays, the CFO’s latest mandate to “do more with less.” And then there are the things no one talks about until they suddenly become very expensive.

Welcome to the thrilling world of holdover tenancy.

When a lease agreement ends but the tenant remains in the premises, even for what feels like an innocent extra week, the meter starts running—fast. The legal term for this is tenancy at sufferance, but “sufferance” is a polite way of saying “your P&L is about to suffer.”

For large occupiers juggling dozens—or hundreds—of locations, a single holdover tenant can cascade into increased rent, operational disruption, legal exposure, and a very unpleasant conversation with the CFO about why you’re suddenly paying double rent on a space you were supposed to vacate.

Let’s break down why holdover tenancy is becoming one of the most expensive—and most overlooked—risks in modern portfolio management, what’s driving the surge, and how to protect your organization before the next lease term ends.

Why Holdover Tenancy Exists (and Why It Hurts So Much)

At first glance, a holdover clause feels like legal housekeeping sprinkled into every written lease. The premise seems simple:

When the lease expires, the landlord may charge elevated rent if the tenant continues to occupy the rental property.

In reality, this tiny clause packs an outsized punch. Under most commercial leases:

- The moment the lease ends, your right of possession ends.

- If the tenant continues occupying the premises, the lease converts into a month-to-month lease or periodic tenancy—usually at 150% to 300% of base rent.

- If the landlord accepts rent payments, that can—depending on state and local laws—create an unintended new tenancy, complicating the eviction process.

- If the landlord does not wish to accept rent, they may pursue legal action, often a formal holdover proceeding in small claims courts or commercial housing courts.

The reasoning? Landlords need certainty. When a tenant fails to leave, the landlord loses control of their asset. They may miss a new tenant’s scheduled move-in, incur actual damages, delay construction, or even lose financing tied to occupancy timelines.

In such cases, the landlord may treat a holdover as a breach, seek to evict the tenant, or attempt to collect actual damages caused by the extended stay. Yikes!

Why Holdover Tenancy Is Surging in 2025

Historically, many landlords looked the other way on small delays—especially if the landlord accepted a simple extra rent payment and both sides wanted a smooth transition.Those days are gone.

1. Market Pressures Are Changing the Rules

Office vacancies hit 20.1% nationwide in Q2 2025 (Cushman & Wakefield), the highest since the Great Financial Crisis. With asset values under pressure, lenders scrutinizing cash flow, and owners fighting to maintain NOI, landlords now need predictability more than ever.

Higher vacancy + tighter lending = stricter enforcement.

2. Construction Delays Are the New Normal

More than 60% of office build-outs delivered behind schedule in 2024 (NAIOP), many by 30–90 days. When new space isn’t ready, tenants stay put.

But unless the landlord gives genuine approval—in writing—for an extension, the delayed exit almost always triggers the holdover period and the associated penalties.

3. Portfolio Complexity Has Skyrocketed

With hybrid work reshaping footprints, tenants are:

- downsizing,

- rightsizing,

- creating collaboration hubs,

- subleasing,

- merging locations,

- and adjusting for constantly shifting headcounts.

More moving parts means more rental terms, more termination dates, more notice windows, and more opportunities for someone to miss a deadline. And when a tenant refuses or simply forgets to vacate, the rental business consequences escalate quickly.

4. Internal Delays Are Becoming Unavoidable

Whether due to budget cycles, protracted negotiations, redesigns, or C-suite review, many new lease agreement processes now stretch longer than they used to. That means more tenants enter an uncomfortable no-man’s-land at the end of the lease, unsure whether the next space will be ready or the current landlord will grant a short-term extension.Landlords, however, are increasingly treating these situations as tenant holding without permission—and billing accordingly.

The True Cost of Becoming a Holdover Tenant

The direct rent premium is only the beginning. The downstream costs are where things really get interesting for your finance team.

1. Rent Payments Surge: 150% to 300% Overnight

Across major U.S. markets, the average holdover tenant triggers rent at 175% to 250% of the original lease according to JLL’s 2024 Occupier Sentiment Report.

Example: A corporate tenant paying $50/SF on a 20,000-SF space faces:

- $1M annual rent at base rate

- $1.75M to $2.5M annualized during a holdover

- Even one month can cost $50K to $80K in unbudgeted expenses.

For a company juggling 40–200 locations, those numbers multiply dangerously fast.

2. Legal Risk and Forced Tenancy

If the landlord wishes to regain possession, they may file a formal eviction case or eviction proceeding, even in commercial settings. In some states:

- If the landlord accepts payment, it may inadvertently create a tenancy at will or a renewed month-to-month term.

- If they refuse payment, the tenant may rack up unpaid rent, penalties, legal fees, and risk a forced lockout.

Welcome to the world where the wrong check can legally trap you in a rental agreement you no longer want.

3. Property Damage Claims and Construction Delays

Landlords may claim:

- Property damage beyond the security deposit

- Actual damages tied to a delayed incoming tenant

- Unapproved physical changes that must be remediated

- Rush fees for accelerated construction

- Storage or relocation costs for the next tenant

In large urban markets, these claims can reach six or seven figures.

4. Operational Disruption

Holdover creates a domino effect:

- Two simultaneous leases

- Double rent payments

- A rushed move

- A disrupted construction schedule

- Additional overtime labor

- Technology downtime

- Dislocated teams

- CFO heartburn

Even well-oiled corporate real estate teams buckle under the pressure of a poorly timed holdover period.

How Corporate Tenants End Up in Holdover (Even When They Swear They Won’t)

Holdover is almost never the result of negligence. Instead, it’s usually caused by everyday operational realities that collide at the worst possible time.

1. Mismatched Timelines Between Spaces

When the next space isn’t complete, but the current lease term ends, the tenant has little choice. Without landlord’s permission in writing, staying even 24 hours can trigger penalties.

2. Miscommunication Between Real Estate, Facilities & Finance

One missed date. One outdated spreadsheet. One assumption that “someone else is tracking this.” This is why holdover tenancy disproportionately affects large occupiers.

3. Slow Internal Approvals

Especially in 2024–2025, corporate governance has tightened. Renewal approvals that once took 30 days now sometimes take 90–180.Meanwhile, the clock on the lease period keeps ticking.

4. Landlords Changing Tactics

Some landlords, facing financial pressure, now:

- refuse to accept rent during holdover

- accelerate legal filings

- increase penalties

- or insist on immediate surrender of possession

The softer, handshake-heavy days of relationship-driven office leasing are fading quickly.

What Tenants Need to Do in This New Market Reality

The rules of the game have changed—permanently. To avoid becoming an expensive example in your CFO’s next “risk management” slide deck, tenants must adapt.

1. Negotiate Stronger—Much Stronger—Holdover Terms Upfront

Corporate tenants increasingly push for:

- Capped rent multipliers (125–150% max)

- Grace periods (5–10 days to vacate)

- Limits on consequential damages

- Clear definitions of what constitutes landlord genuine approval

If your portfolio includes rent-regulated or legacy markets (New York, LA, San Francisco), even more protections may be warranted due to unique rules and state laws governing holdover.

2. Track Every Date Automatically (Stop Relying on Spreadsheets)

Most holdovers happen because someone misses a date buried in a spreadsheet tab. Automation is no longer optional.

Platforms like REoptimizer® centralize:

- lease expirations

- renewal windows

- notice requirements

- rent escalations

- termination options

- landlord restrictions

- deliverable timelines

One dashboard. Zero surprises.

3. Begin Renewals or Relocations 12–18 Months Out

For spaces over 10,000 SF, this is the industry standard. For multi-location portfolios, it’s survival.

This buffer protects against:

- construction delays

- slow negotiations

- supply chain issues

- shifting headcounts

- internal approval bottlenecks

Starting early is the easiest way to avoid a holdover tenant situation.

4. Assess Landlord Stability Before You Sign

Landlords in distress enforce rules aggressively. They:

- decline extensions

- reject rent checks

- file holdover claims quickly

- avoid informal agreements

- require strict compliance with written notice

A landlord’s financial state is now a material risk factor—just like rent, TI, or location.

The Bigger Picture: Holdover Is a Symptom of a Larger Market Shift

Here’s the uncomfortable truth: Holdover tenancy isn’t rising because tenants are suddenly disorganized. It’s rising because the entire commercial real estate ecosystem is under stress.

Hybrid work has created unpredictable space needs. Construction timelines remain volatile. Capital markets are tightening. Landlords are fighting for every dollar. Tenants are optimizing every square foot.

And in this high-stakes standoff, timing is everything—and timing is fragile. Holdover tenancy is simply where all those stress fractures show up.

The Bottom Line: In 2025, You Can’t Afford to Be Caught Off-Guard

If you manage a large corporate portfolio, holdover exposure isn’t a legal footnote—it’s a six-figure risk that can snowball into an operational crisis.

The best-run tenants in the world are tightening their processes because the market is tightening its tolerance.

The new mandate for real estate leaders? Eliminate surprises, reactive decisions, and preventable costs.

How REoptimizer® Helps You Stay Ahead of the Curve

In a landscape where key dates drive your portfolio performance, your team needs clarity—not scattered spreadsheets, outdated trackers, or “Bob said he put the date in the SharePoint doc.”

REoptimizer® gives occupiers:

- A single source of truth for every lease

- Automated alerts before every critical date

- Real-time visibility into expiration risks

- Portfolio-wide reporting for C-suite insight

- Tools to plan market timing months ahead

- Workflows to reduce human error

- Analytics to avoid unbudgeted surprises

Instead of reacting to missed dates or expensive holdover tenancy, you stay ahead of every move, every negotiation, every renewal. Because the best portfolio strategy isn’t responding to emergencies. It’s preventing them. Learn more today.

Learn More

The debt markets are always the first to whisper when real estate’s about to shift.

And right now, the commercial mortgage-backed securities (CMBS) is giving us a detailed stress map of where commercial real estate (CRE) is being repriced.

And that map shows two very different paths for property types. For months, delinquency rates have been creeping up across commercial real estate, but a closer look reveals something deeper — a market quietly redrawing the boundaries between office, industrial, and multifamily assets.

A Tale of Two Commercial Real Estate Markets

The headline number grabbed attention:

- Overall CMBS delinquency rate: 7.46 %, up 23 basis points from the month prior — the highest in nine years.

- Overall delinquent balance: $44.6 billion, after $4 billion in newly delinquent loans in October alone.

- Outstanding balance: down to about $598 billion, meaning the same number of delinquencies now makes up a larger share of the pool.

Behind those averages lies the real story — a widening gap between sectors.

Office remains the epicenter of stress.

- Office delinquency rate: 11.76 %, a new all-time high.

- Newly delinquent office loans: more than $1.7 billion in October, while only $760 million were cured.

- The rise marks the sixth consecutive month of office delinquencies climbing.

By contrast:

- Industrial’s delinquency rate decreased to around 0.64 %, holding near record lows.

- Multifamily delinquency rate: 7.12 %, up 53 basis points — its highest since 2015.

- Retail delinquency rate: 6.89 %, up 13 basis points; lodging: 6.07 %.

The result is a bifurcated market: distress in office and parts of multifamily offset by resilience in industrial.

Why Office Keeps Breaking Down

The office story isn’t just cyclical — it’s structural.

Vacancy and utilization remain stuck near post-pandemic lows. Lenders who extended maturity dates last year are running out of patience, and the maturity wall in 2025-26 is forcing a reckoning.

Borrowers face a triple hit:

- Valuations down 30–50 % from pre-2020 peaks.

- Interest costs doubled or worse.

- Refinancing options scarce.

Those ingredients are producing a steady pipeline of newly delinquent loans and swelling delinquent balances. For many borrowers, there’s no economic case to refinance; handing the keys back is cheaper than rolling debt at a negative yield.

For occupiers, that distress changes the playing field.

- Landlords under pressure are offering shorter leases, bigger TI allowances, or blend-and-extend deals just to keep cash flow current.

- Corporate tenants with strong credit can extract value now — especially in Class A or B buildings facing upcoming loan maturities.

- Owners with their own office properties should re-underwrite values and debt coverage; the next appraisal may not look anything like the last one.

Office delinquencies are no longer an anomaly — they’re a reset mechanism. The CMBS market is effectively repricing office debt in real time, establishing the “new normal” for yield spreads and valuations.

Industrial: The Lone Sector Still Getting a Pass

While office burns, industrial remains the calm center of the storm.

Even with construction costs rising and cap-rate expansion trimming some values, the sector’s fundamentals still look enviable:

- Vacancy below 4 % nationally.

- Rent growth averaging mid-single digits.

- Debt service coverage well above 1.6 × across most portfolios.

That’s why industrial’s delinquency rate retreated in Q3 — the only major sector to post a decline.

Lenders see it too. CMBS investors continue to pay tighter spreads for logistics-backed pools, while life companies and banks compete to place debt with reliable warehouse and manufacturing borrowers.

Still, the calm could fade. Slowing trade and reshoring logistics might compress demand growth in 2026, and fewer speculative projects mean less future inventory. But compared to office or even retail, industrial remains the lowest-risk credit in CRE.

Multifamily: The Momentum Slows

For much of the past decade, multifamily was the safe bet. That narrative is shifting.

The multifamily delinquency rate pulled the overall CMBS index higher this quarter, climbing past 7 %. Rising operating expenses and higher floating-rate debt are behind the move. Many short-term bridge loans written during 2021’s boom are reaching their maturity dates now, and refinancing at today’s rates often requires fresh equity.

Yet context matters:

- Fannie Mae and Freddie Mac loans still show delinquency rates near 0.64 %, essentially unchanged for six months — the lowest rate across CRE.

- Trouble is concentrated in private CMBS and bank balance-sheet loans for newer apartment buildings that overshot pro-forma rents.

So, yes, multifamily delinquencies are up — but it’s a rate shock, not a demand collapse.

Retail and Lodging: Somewhere in the Middle

Retail and lodging continue to post back-to-back months of minor delinquency increases. But the nuance matters: necessity-based centers are stable, while legacy malls and secondary hotels remain under strain.

These sectors show how the overall delinquency rate can rise without signaling a systemwide breakdown. The credit stress is uneven—concentrated where tenant demand or capital access has structurally changed.

The Broader Credit Picture

Pull the lens back and you can see what’s really happening.

- Newly delinquent loans keep outpacing cured loans, meaning total delinquencies keep rising even when some assets recover.

- Because the outstanding loan balance is shrinking, each new default moves the needle more.

- Serious delinquencies (60+ days late or in foreclosure) now make up nearly 7 % of CMBS loans.

This isn’t a liquidity freeze like 2008; it’s a repricing cycle. Capital is migrating away from legacy risk — older office, marginal retail — and toward sectors with tangible user demand and rent resilience.

What It Means for Executives and Tenants

If you sit in a boardroom managing a national footprint or a real estate portfolio, the implications are concrete.

1. Office negotiations will tilt toward tenants: Loan stress equals flexibility. Expect landlords to prioritize occupancy over rent growth.

2. Industrial will stay competitive: Low delinquency and steady absorption mean little distress-driven opportunity. Lock in renewals early.

3. Multifamily’s correction will create selective openings: Distress in smaller, high-leverage projects may generate attractive recap or acquisition plays.

4. Watch the credit pipeline: Monitor CMBS delinquency rate trends by property type — they’ll telegraph which sectors will see value compression next.

Looking Ahead: Sorting, Not Sinking

Across the past year, the CMBS market has evolved from a passive tracker of distress to the active mechanism through which CRE values reset.

What happens over the next few quarters will hinge on three data points:

- Volume of newly delinquent loans versus cures each month.

- The size of the delinquent balance relative to the outstanding balance.

- Sector-specific delinquency trends — whether industrial’s decrease can offset office’s all-time highs.

If those ratios stabilize, we’ll call this the bottom. If not, 2026 could bring another wave of price discovery, especially as the next batch of CMBS loans hits its maturity dates.

Either way, this moment is defining the next phase of commercial real estate. Delinquency rates are the truest reflection of where value, risk, and opportunity are moving. Consider them the clearest window into what’s next. REoptimizer® helps you read that window — and respond.

With REoptimizer®, you don’t just track data; you use it. Our platform helps you quantify exposure, identify negotiation leverage, and plan real estate moves that align with evolving market conditions.

Because in a cycle defined by repricing and uncertainty, clarity is your most valuable asset. Learn more about how REoptimizer® gives your portfolio the razor sharp edge it needs to survive amid an evolving CRE market.

When Brookfield defaulted on over $1 billion in loans tied to its downtown Los Angeles office properties last year, the news spread quickly across the financial press.

Bloomberg cited “rising interest rates” and “higher borrowing costs weighed on valuations.” The Financial Times reported that property values had fallen by half, and that lenders were moving several buildings into special servicing.

But the story wasn’t just about one firm. Brookfield’s defaults—rooted in its sprawling portfolio of office towers like the Gas Company Tower, EY Plaza, America Plaza, and the 777 Figueroa Street tower—signaled a deeper shift in how commercial real estate (CRE) works in the modern era.

This wasn’t a bankruptcy. It was a business model pivot—a public admission that owning too much office space had become a liability.

And now, as Brookfield sells off billions in office assets, it’s becoming a case study in how even the most powerful owners are being forced to evolve, deleverage, and redefine success.

The Los Angeles Defaults: A Case Study in Value Erosion

In February 2024, Brookfield defaulted on loans totaling over $1 billion across its Los Angeles office portfolio, including loans backed by its once-flagship Gas Company Tower.

That 52-story building, valued at $675 million in 2021, was later appraised at just $270 million—a 60% loss in value. It soon landed in receivership, joining a growing list of high-profile Los Angeles office buildings in distress.

The same story repeated at EY Plaza, where Brookfield defaulted on a $275 million loan, and at 777 Tower, burdened with $289 million in debt before a planned $145 million sale collapsed. Another major property, the Wells Fargo Center, carried $763 million in outstanding debt set to mature within the year.

Collectively, these defaults represented less than 1% of Brookfield’s total real estate assets—but more than $1 billion in direct losses tied to some of the country’s most visible downtown office buildings. For lenders and investors, it was a chilling signal that even institutional-grade assets were not immune.

How We Got Here: The Office Market’s Fragile Economics

To understand the Brookfield defaults, it’s necessary to zoom out to the macroeconomic forces reshaping the office market nationwide.

- Office values have plummeted by 30–70% in key U.S. metros since 2020.

- Rising interest rates have doubled borrowing costs for many landlords.

- Leasing demand has declined as tenants shrink footprints and adopt hybrid work.

- Outstanding debt on office assets is expected to exceed $1 trillion by 2026, according to Morgan Stanley.

In this context, Brookfield’s decision to walk away from underwater properties was less a shock than a preview of what’s ahead.

The firm recognized, earlier than most, that paying on non-recourse loans for half-empty office towers in Los Angeles, San Francisco, and even New York no longer made financial sense.

By allowing lenders to take possession, Brookfield effectively capped its losses.

“We made the prudent choice not to continue making payments on certain non-core assets,” Brookfield spokesperson

They confirmed the defaults but emphasized that the company’s “core office holdings remain strong.” In truth, this selective retreat reflected the harsh math of modern real estate: cash flow couldn’t cover debt service, and refinancing at today’s interest rates would have been ruinous.

From Foreclosures to Fund Management: Brookfield’s 2025 Pivot

Fast forward to late 2025. Brookfield, once the largest office owner in the United States, has become one of the largest office sellers. The company is preparing to offload $10 billion in office assets by 2030 as part of a broader $45 billion real estate reduction plan, reshaping its $80 billion portfolio.

The strategy is clear:

- Sell or relinquish underperforming office properties.

- Refinance $8 billion in debt maturities coming due over the next two years.

- Double down on fund management—raising capital from investors rather than owning the properties directly.

Among the properties reportedly on the block are One Liberty Plaza in New York, One Leadenhall in London, and other mid-tier towers that no longer fit Brookfield’s definition of “super-core.”

Meanwhile, the company’s new $17 billion opportunity fund is already targeting distressed office and retail assets—potentially including some buildings it once owned. It’s a full-cycle repositioning: from borrower to buyer of bargains.

Data Doesn’t Lie: The Office Market Is Still in Decline

If Brookfield’s shift seems drastic, it’s because the numbers demand it.

According to Green Street Advisors, U.S. office property prices have fallen by 52% in major CBDs since the pandemic. In San Francisco, vacancy rates hover near 35%; in downtown Los Angeles, they’re approaching 30%.

Even prime assets are trading at cap rates unseen since 2009.

And the outlook? Still cloudy.

- Interest rates remain elevated, and lenders have become more selective.

- Special servicing volumes are up 118% year-over-year, per Trepp data.

- Nearly $300 billion in office loans will mature by the end of 2026.

This means borrowers like Brookfield—even with access to capital and deep relationships with banks—are being forced to make hard choices: sell, restructure, or default.

Lessons from Brookfield: The New Playbook for CRE Giants

The Brookfield defaults are not an isolated event but a glimpse into a broader structural evolution in commercial real estate.

1. The Era of Permanent Leverage Is Over.

For decades, firms like Brookfield and Blackstone thrived on cheap debt and long-term appreciation. That model depended on predictable cash flow and stable interest rates. Neither exists today.

2. Non-Recourse Lending Has Changed the Game.

By utilizing non-recourse loans, Brookfield could default strategically without broader balance sheet exposure. This “walk-away option” is increasingly being exercised by borrowers across markets, particularly where office values have fallen by more than 40%.

3. Portfolio Management Is Now About Subtraction, Not Addition.

Brookfield’s 2025 selloff marks the dawn of lean real estate operations. It’s not just offloading debt—it’s redefining what “core” means in a world where occupancy and financing risk dominate returns.

4. The Shift to Fund Models Is Permanent.

Institutional firms are pivoting from ownership to capital management. Instead of holding towers directly, they raise funds to invest opportunistically—minimizing exposure while keeping upside optionality.

Implications for Tenants and Corporate Occupiers

For corporate tenants, the Brookfield defaults carry clear operational lessons.

- Know Your Landlord’s Financial Health.

Buildings in special servicing or foreclosure can impact lease terms, maintenance, and renewals. Due diligence on ownership structure and outstanding debt is no longer optional. - Revisit Lease Clauses for Continuity and Control.

Tenants should negotiate protections in case of landlord default or asset sale—including continuity-of-service agreements, rights of first offer, and early termination triggers tied to building ownership changes. - Capitalize on Distress.

For tenants renewing or relocating, this period offers leverage. Landlords facing loan maturities or value erosion are increasingly open to generous concessions—free rent, build-out allowances, and flexible terms.

The Wider Market Picture: Default as Strategy, Not Failure

While Brookfield defaulted on marquee Los Angeles office buildings, it continues to expand its global funds platform and manage over $825 billion in total assets. That’s the paradox of today’s market: defaulting is not necessarily failing—it’s sometimes optimizing.

As one former Brookfield executive with direct knowledge of the firm’s debt strategy told the Financial Times, “These are not distress moves—they’re deliberate portfolio management.”

In other words, the default itself has become a financial instrument, a tool to rebalance and reprice risk in an environment where debt and property values no longer align.

What’s Next: Two Years That Will Define the Decade

Over the next two years, the office market faces its most critical test.

Between now and 2027, nearly $800 billion in commercial loans will mature—most tied to office and retail properties whose values have not recovered.

Morgan Stanley estimates that $500 billion of this debt is “at risk of refinance failure.” That means many landlords, from regional owners to global firms, will have to either inject new capital, sell at discounts, or surrender assets outright.

If the Brookfield defaults were the early warning, the Brookfield selloffs are the blueprint for survival.Firms are consolidating, deleveraging, and retooling for a leaner, more data-driven era of CRE.

The Future Belongs to the Agile

The story of Brookfield—from downtown Los Angeles defaults to a global office selloff strategy—captures the broader transformation of the commercial real estate industry.

This is no longer a market of endless expansion or trophy ownership. It’s a market where information, timing, and agility define performance.Office properties are no longer passive income streams; they are dynamic liabilities that must be managed, hedged, or repositioned.

Brookfield’s evolution—from defaulting borrower to opportunistic fund manager—proves one thing: in the new world of commercial real estate, the smartest firms aren’t the ones who never stumble—they’re the ones who immediately respond, adapt, and turn crisis into capital.

If you thought the office slump had bottomed out, think again. Because the office market may have turned a corner in absorption, but not in value.

According to CoStar’s latest CMBS analysis, distressed U.S. office buildings have lost more than half their appraised value over the past 12 months. For tenants, that headline is a marker of transition. The office market is redefining what value means, and those who adapt early will shape the future landscape of corporate space.

A Historic Value Correction — and It’s Not Over Yet

CoStar’s deep dive into 270 specially serviced CMBS loans paints a stark picture: the collateral behind those loans is now worth $16.6 billion, down from $34.6 billion when they were originated. That’s an $18 billion haircut, with average reappraisal values down 52%.

The culprit? Plummeting occupancy.

A portfolio that was underwritten at 91% occupancy now averages just 64%, a 27-point decline that has vaporized billions in equity. Nearly a quarter of these properties are less than half full. As one CMBS analyst put it bluntly, “What we’re seeing is a reset of expectations — not just in valuation, but in what the office actually means.”

The math gets ugly fast:

-

Over 70% of loans now carry loan-to-value (LTV) ratios exceeding 100%.

-

The average LTV is 167% — meaning the property is worth far less than its debt.

-

Half of properties can’t generate enough income to cover their debt payments.

-

Nearly 80% of the loans are delinquent.

This is market re-pricing in real time.

Occupancy Is the Value Driver

One of CoStar’s most striking findings: Properties that saw occupancy drop by 40 percentage points or more experienced 62% value declines, nearly double that of assets that held steady.

In other words: every lost tenant directly compounds valuation loss. Office properties lost an average of $655 in value per square foot of vacated space. That’s an unprecedented sensitivity to tenancy — and a wake-up call for landlords (and tenants negotiating with them).

The reason? In this environment, cash flow equals survival. With fewer leases to support debt service, even modest rent roll losses can push a building into default territory. As one commercial finance executive put it, “Today’s office market isn’t just about who can fill space — it’s about who can finance it.”

Downtown Pain, Suburban Stability

The data also draws a sharp distinction between downtown and suburban offices.

-

Central business district (CBD) properties: 58% occupancy, 189% average LTV.

-

Suburban properties: 67% occupancy, 157% average LTV.

In plain terms, suburban buildings are holding up better, even if they’re not thriving. The decentralization trend that began during the pandemic is proving durable, driven by tenant demand for shorter commutes, smaller footprints, and flexible configurations.

For corporate occupiers, this means leverage in both directions:

-

Downtown landlords are highly motivated to deal.

-

Suburban options offer pricing power and flexibility.

The “flight to quality” narrative remains true for top-tier assets, but equally powerful is the “flight to convenience” — a redefinition of location value in the hybrid era.

CMBS Meltdown: Retail and Secondary Markets Join the Slide

The office sector isn’t alone. CMBS investors are also absorbing steep losses in retail and secondary markets.

Consider the Palisades Center in West Nyack, New York — one of the largest malls in the country. Once appraised at $881 million, the property’s 2023 valuation came in at just $209 million. Bondholders in a $418.5 million CMBS loan suffered major write-downs, extending into even Class A bonds, traditionally considered safe.

The loan’s servicer, Mount Street, applied $231.4 million in losses, while Class A bondholders recouped just $157.1 million of their $229.1 million investment.

That means even the most senior bondholders — the ones “protected” by layers of subordination — weren’t immune. It’s a stark reminder of how deep the devaluation runs when fundamentals crack.

Meanwhile, in Cleveland, a 21-story downtown office tower at 1100 Superior Avenue sold for $8.1 million after being valued at $52.5 million a decade earlier. The building was 32% occupied at sale, and investors in its $45 million loan were completely wiped out.

Those numbers illustrate what many CRE professionals already sense: the value reset isn’t isolated — it’s systemic.

“This Is a Reset, Not a Recession”

While headlines paint doom, industry analysts are framing this as a rebalancing rather than a collapse.

“This is the painful but necessary repricing of office risk,” said a senior CoStar economist. “We’re seeing a market that’s finding its new equilibrium — one that’s smaller, leaner, and better aligned to post-pandemic work habits.”

There’s truth in that optimism. CoStar reports that, for the first time since late 2021, net absorption turned positive in Q3 2025, with 12 million more square feet occupied than vacated.

That’s a crucial inflection point: while capital markets are correcting, leasing demand — albeit measured and cautious — is stabilizing. Occupiers are returning to the market, but they’re doing so strategically.

Strategic Implications for Large Tenants and Occupiers

For corporate occupiers and multi-location tenants, this environment is both a challenge and a window of opportunity.

Here’s how the smartest real estate teams are thinking right now:

1. Leverage the Landlord’s Pressure

With so many owners facing delinquent loans and shrinking cash flow, tenants hold more leverage than they realize.

Use that to:

-

Negotiate higher tenant improvement (TI) allowances.

-

Secure shorter initial terms with extension flexibility.

-

Lock in expansion or contraction rights that mirror headcount volatility.

-

Ask for blend-and-extend arrangements at reduced rents.

2. Recalibrate Portfolio Mix

The CoStar data validates what many occupiers have already begun doing: rebalancing downtown exposure with suburban efficiency.

Hybrid work isn’t eliminating office demand — it’s redistributing it.

Occupiers are trading older, high-cost CBD leases for smaller, amenity-rich suburban or edge-urban locations closer to workforce clusters.

It’s a portfolio optimization moment, not a retreat. The occupiers who act now can lock in long-term flexibility at favorable rates while landlords are still recalibrating.

3. Watch for Secondary Market Value Plays

The Cleveland sale is instructive.

When a $52 million asset trades for $8 million, it signals more than distress — it signals entry pricing for opportunistic buyers and corporate owner-occupiers.

Expect corporate sale-leaseback interest to accelerate as lenders reset valuations and motivated sellers surface.

For large occupiers considering owning versus leasing, 2025–2026 may present the most attractive acquisition pricing in a decade.

4. Use Data to Drive Negotiations

In a market this fluid, data is negotiation currency.

Armed with real-time occupancy, rent comps, and CMBS loan performance, tenants can frame lease proposals around facts, not feelings.

If your landlord’s loan is underwater — and CMBS data shows many are — you have an edge.REoptimizer’s® analytics and benchmarking tools help occupiers identify where those pressure points exist and align negotiation timing with ownership risk.

The Bigger Picture: A Reset Toward Efficiency

The office market is being resized to fit a leaner, more distributed workplace ecosystem. Value is shifting from size and address to adaptability and utilization.

Lenders, landlords, and tenants alike are being forced to think in cash flow terms, not legacy valuation models. For corporate occupiers, this means future portfolios will be built around:

-

Data-backed utilization metrics

-

Flexible lease structures

-

High-performance space efficiency

-

Geographic diversification

In short: the future office portfolio is smaller, smarter, and more strategic.The CMBS fallout isn’t the end of office real estate — it’s the end of denial.The market is repricing risk, not erasing relevance. Occupiers that act strategically in this window will define the next decade of corporate real estate.

At REoptimizer®, we see this every day — tenants using analytics, timing, and leverage to transform market uncertainty into long-term advantage.Because in CRE, distress creates opportunity — but only for those ready to move.

When your lease ends but you’re still in the space, things can get expensive—fast.

Enter the holdover clause. Few lease provisions are as deceptively simple (or as financially punishing) as the holdover clause. Yet many corporate tenants gloss over it until it’s too late. When you overstay your lease, even for a few weeks, the repercussions can ripple across your entire portfolio, hitting your P&L, disrupting operations, and straining landlord relationships.

This article breaks down:

-

The essentials of holdover clauses and why they exist

-

The most common scenarios that trigger holdover tenancy

-

The financial, legal, and operational consequences

-

Proactive strategies to protect your organization before problems arise

If you manage corporate leases, understanding your holdover exposure isn’t optional—it’s essential to maintaining financial and operational control.

What Is a Holdover Clause, and Why It Matters

A holdover clause is a standard provision in most commercial leases that specifies what happens if a tenant remains in the space after the lease expires.

At first glance, it might seem like a minor administrative detail. But the stakes are high: once your lease term ends, your legal right to occupy the space ends with it. Any continued occupancy—no matter how temporary—can trigger steep rent increases, penalties, or even legal action.

How Holdover Clauses Work

Under a typical commercial lease, if the tenant does not vacate by the expiration date, the landlord can:

-

Impose “holdover rent”—often 150% to 300% of the base rent

-

Convert the lease to a month-to-month tenancy, which can be terminated with minimal notice

-

Pursue damages if the holdover delays a new tenant’s move-in or causes income loss

The reasoning is simple: landlords need predictability. If your company’s extended occupancy prevents them from leasing to someone else, they lose revenue. The higher rent functions as both a deterrent and compensation for that risk.

The Hidden Risk

In a tight or shifting office market, a holdover clause can become a financial trap. For tenants with large or complex portfolios, one delay in move-out can translate into hundreds of thousands in unexpected costs.

And the danger isn’t limited to rent alone—holdovers can also lead to consequential damages, including construction delays for the next tenant, accelerated restoration costs, or even litigation fees.

The Numbers Behind Holdover Exposure

According to CBRE, lease expirations are peaking across U.S. office markets through 2026, as companies continue to right-size and renegotiate post-pandemic. That means more tenants are juggling multiple end dates and move-outs—conditions ripe for accidental holdover.

Recent data from JLL’s 2024 Occupier Sentiment Survey shows:

-

43% of corporate tenants report difficulty aligning lease expirations with new space delivery schedules.

-

Nearly 1 in 5 tenants have incurred holdover rent penalties in the past five years.

-

The average rent premium charged for holdover occupancy ranges from 175% to 250% of base rent.

For a tenant paying $50 per square foot on a 20,000-square-foot lease, even one month of holdover at double rent can cost $50,000 to $80,000 in unbudgeted expenses—not counting downstream legal costs or operational disruption.

In an era when CFOs are laser-focused on real estate optimization, that’s a financial risk no portfolio should absorb.

How Tenants End Up in Holdover

Even the most sophisticated tenants can find themselves unintentionally overstaying their leases. The causes often stem from operational realities rather than negligence.

1. Construction and Delivery Delays

One of the top causes of holdover tenancy is delayed occupancy in the next location. Build-outs rarely run exactly on schedule—per a 2024 NAIOP study, more than 60% of office construction projects experience completion delays averaging 30–90 days.

If your new space isn’t ready, staying in your current location may feel unavoidable. But unless your current landlord agrees in writing to an extension, that stay likely triggers the holdover clause—and the rent hike that comes with it.

2. Portfolio Complexity and Lease Overlaps

Corporate real estate portfolios have become more dynamic, with tenants adjusting space footprints, hybrid schedules, and subleases. Managing these transitions introduces new timing risks.

In a multi-location portfolio, just one missed expiration date or miscommunication between facilities and finance can lead to a costly holdover. Even a few days of delay can set off billing disputes and strained landlord relations that ripple across other properties.

3. Negotiation or Renewal Delays

In some cases, tenants find themselves in holdover limbo because lease renewal negotiations drag past the expiration date. When internal approvals or market uncertainty slow decision-making, the holdover clause becomes an expensive stopgap.

The Real-World Consequences

Holdover tenancy doesn’t just mean higher rent. The consequences compound quickly—financially, legally, and operationally.

1. Financial Impact: Rent and Damages

Most holdover clauses stipulate a rent increase of 150% to 200% of the final year’s rent. For large tenants, that can escalate costs by six figures in a single month.

Beyond rent, landlords can also claim consequential damages, including:

-

Lost income from delayed occupancy by a new tenant

-

Expedited restoration costs, such as overtime labor or rush fees for contractors

-

Reimbursement for relocation or storage expenses incurred by the incoming tenant

Even if you eventually vacate, you may still be responsible for these additional costs.

2. Legal and Reputational Risk

If the landlord files for eviction, your company could incur legal fees and damage its reputation in the landlord community—complicating future lease negotiations.

In some jurisdictions, accepting rent during a holdover period can inadvertently create a periodic tenancy, complicating the legal process further. Landlords often respond by refusing rent payments and initiating formal eviction to protect their rights.

3. Operational Disruption

Holdover periods create cascading effects: delayed moves, double rent payments, rushed relocations, and project overruns. Teams end up reacting instead of planning.

How to Avoid Becoming a Holdover Tenant

The best defense against holdover risk is proactive lease management and careful negotiation—long before your lease approaches expiration.

1. Negotiate Smarter Terms Upfront

When negotiating a new lease, pay attention to the fine print in your holdover clause:

-

Cap the rent multiplier. Push for a maximum of 125–150% instead of the default 200%.

-

Include a grace period. Negotiate a short window—typically 5–10 days—before penalties apply.

-

Clarify consequential damages. Limit liability to direct rent and exclude indirect or third-party damages.

These small adjustments can save significant costs if a delay ever occurs.

2. Leverage Lease Management Technology

Many holdovers happen because teams simply lose track of critical dates. With REoptimizer®, tenants can track lease expirations, critical clauses, and move timelines across every location in one dashboard—automatically flagging upcoming deadlines months in advance.

Visibility turns reactive management into proactive strategy.

3. Start Early on Renewals and Relocations

Industry best practice is to begin the renewal or relocation process at least 12–18 months before lease expiration for spaces over 10,000 square feet.

This timeline allows for:

-

Market analysis and benchmarking

-

Negotiation flexibility

-

Adequate build-out and move-in scheduling

Early action gives you leverage—and leverage saves money.

4. Audit Landlord Financial Stability

If your landlord faces distress, ownership changes, or asset sales, holdover risks can multiply. Financially unstable landlords may accelerate enforcement, file claims aggressively, or even refuse short-term extensions.

Before signing or renewing, review the landlord’s financial health and ownership structure. A stable landlord relationship creates predictability for both sides.

The Market Context: Why Holdover Risks Are Rising

The commercial real estate market of 2025 is anything but stable. Hybrid work, elevated vacancy rates, and capital market pressures have forced landlords to scrutinize every dollar.

According to Cushman & Wakefield, U.S. office vacancy rates reached 20.1% in Q2 2025, with sublease availability at an all-time high. For landlords navigating declining asset values, every lease and every rent payment matters.

That means enforcement of holdover clauses is stricter than ever. Where landlords once showed flexibility, today they’re protecting income aggressively. Tenants that haven’t planned ahead are finding themselves with fewer options—and higher bills.

The Bottom Line

Holdover clauses may seem like boilerplate legalese, but their impact can be enormous. In a post-pandemic, high-vacancy market, landlords can’t afford leniency—and tenants can’t afford oversight.

The key takeaway? Never let a holdover clause surprise you.

By negotiating smart terms, tracking critical dates, and planning relocations well in advance, corporate tenants can avoid the steep costs and disruptions of holdover tenancy.

And with tools like REoptimizer®, you can stay ahead of every lease deadline, manage risk across your portfolio, and ensure your real estate strategy stays aligned with your business goals—not at the mercy of your landlord’s calendar.

Key dates drive your portfolio performance.

Lease expirations, renewals, rent escalations—REoptimizer® tracks them all in one platform, keeping your team aligned and your strategy proactive. Stop managing by spreadsheet and start optimizing with automation. Learn more about how the platform can level up your portfolio optimization.

Welcome to the Wall

There’s a wall coming — and it’s made of debt. Roughly $1.5 trillion in commercial real estate loans are set to mature between now and 2027, much of it originated in the low-rate world of 2019–2021.

Those loans were priced when money was free, values were peaking, and tenants were expanding. Fast forward to today:

- Interest rates have tripled.

- Asset values have fallen 20–40% in key sectors.

- Refinancing is both harder and costlier.

According to the Federal Reserve Bank of St. Louis, CRE loan modifications surged 66% year-over-year by mid-2025 — the clearest sign that lenders and owners are scrambling to avoid a reckoning .For investors, it’s a headache. For corporate tenants, it’s an opening. Let’s discuss.

What’s Driving the Crunch

Three converging pressures are creating the maturity wall:

- Rate shock.

Loans written under the Zero Interest Rate Policy (ZIRP) era now face refi rates in the 6–8% range. Debt service coverage ratios that once worked at 3% don’t pencil anymore. - Value erosion.

Office vacancies remain historically high, cap rates have widened, and even industrial yields are normalizing. That means many buildings are “underwater”—worth less than their debt. - Lender triage.

To avoid forced sales, banks are modifying loans: extending maturities, cutting interest, or adding covenants. That buys time—but also creates a market full of cash-strapped owners under lender supervision.

In short: liquidity is scarce, and certainty is gold.

Which makes creditworthy tenants the most valuable currency in the system.

How This Hits the Market

The maturity wall doesn’t just affect landlords — it cascades across the entire CRE ecosystem.

- Capex freezes. Owners with refi stress delay building upgrades, preventive maintenance, and tenant improvements.

- Leasing paralysis. Every new lease triggers lender review. Decision cycles lengthen, and creative deal structures become the norm.

- Valuation gaps. Appraisals are falling faster than debt paydowns, making some assets “zombie buildings” — operational but financially trapped.

- Market bifurcation. Trophy assets with stable tenants still attract capital; Class B and secondary-market buildings are in limbo.

For tenants, this means you’ll see polarized market behavior: some landlords aggressive and flexible, others frozen or non-responsive. Knowing which is which becomes a competitive advantage.

Why This Is Good News for Tenants

Yes, instability sounds scary — but large tenants can use it to win.

- You are the solution to their problem.

Your lease is the collateral they need to refinance. That gives you leverage to demand better economics, more flexibility, and stronger protections. - You can negotiate from strength.

Lenders love predictability. Offer it — in exchange for real value:- Blend-and-extend deals with free rent and TI funded upfront.

- Operating-expense caps and renewal options priced today.

- Termination or contraction rights that preserve flexibility.

- Vacancy equals opportunity.

As some owners capitulate, sublease and distressed assets create low-cost entry points for expansion, consolidation, or relocations. - Distress unlocks creativity.

Sale-leasebacks, credit-tenant structures, and JV developments are back on the table as owners hunt for cash flow.

The Risks You Can’t Ignore