Distressed properties aren’t just someone else’s problem—they’re embedded risks and potential leverage points in your real estate portfolio.

Whether you’re consolidating space, renegotiating a lease, or eyeing a relocation, understanding the financial health of your landlord is critical due diligence in this new age.

Because when buildings face widespread loan delinquencies, expiring anchor leases, or NOI shortfalls, your tenancy is exposed to more than deferred maintenance. You’re looking at unreliable concessions, management instability, or worst case foreclosure-related disruptions. And this is no longer just a nightmare scenario, it’s a real landmine for tenants to dodge

But in the right hands, these same properties become tools for negotiation: below-market rents, flexible terms, and fast-track buildouts.

So, without further ado, let’s get into it. Here’s how sophisticated tenants identify, assess, and capitalize on distressed office assets…before the damage reaches their balance sheet.

What Qualifies as a Distressed Property?

In commercial real estate, a property becomes distressed when its income can no longer support its debt, operating costs, or both.

Often this comes with high vacancy, but beyond those numbers, it’s about financial instability that compromises the building’s ability to retain tenants, fund improvements, or even stay solvent.

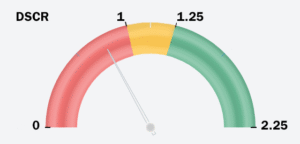

You’ll see the signs: debt service coverage ratios slipping below 1.25, rising rollover exposure, unsustainable concession packages, or a CMBS loan on a servicer’s watchlist.

Think of it as a ticking time bomb with a “For Lease” sign out front.

Red Flags to Watch for Property Distress:

Not all red flags wave in the open. Some are buried in the numbers (and if you miss them, you’re the one left holding the bag). These are the signs that a property’s on the brink:

- Loan Delinquencies: If the landlord can’t pay the mortgage, it’s your problem too. Look for Debt Service Coverage Ratios (DSCR) under 1.25—that’s danger territory.

- Vacancy Rates: High vacancy equals high risk. Fewer tenants mean less income, which makes default more likely.

- Occupancy vs. Vacancy: Don’t be fooled by current occupancy. Look at lease expirations. That 80% occupied tower could be 40% vacant in 12 months. You can consider low occupancy rates a dormant vacancy rate.

- Market Saturation: In oversupplied cities, landlords are bleeding cash just to stay afloat. That creates leverage for you—but also risk.

- Expiring Lease Clusters: Buildings with a high percentage of leases expiring in the next 1-3 years are at risk of a sudden occupancy collapse. If multiple anchor tenants walk, the building’s NOI—and your negotiating power—plummets.

In fact, nearly one-third of national CMBS office loans are distressed. In Chicago, that jumps to 75%. These aren’t isolated problems. They’re systemic. And they’re your opportunity—if you act smart.

Why You Should Care

It’s not just about whether your space looks fine today.

A financially unstable landlord introduces operational and reputational risk—especially in this market. Deferred maintenance, broken TI promises, lease buyouts, or even foreclosure-driven management shakeups can disrupt your business, whether you’re leasing a single floor or managing a 50-site portfolio.

Here’s the reality:

- Delayed Repairs: Capital improvements get slashed. HVAC breaks, and you’re sweating it out.

- Concessions Disappear: Promised TI allowances or free rent? Good luck collecting if the money’s gone.

- Lease Risk: If your landlord defaults, you could get caught in a foreclosure. That means legal headaches and operational chaos.

And here’s the kicker: your landlord might own 10 buildings. You lease in one. If they cross-collateralized their loans and one asset goes under, your “safe” space could get pulled into the mess.

Luckily, platforms like REoptimizer® flags these landlords before you get stuck with them.

The Upside: Strategic Advantages for Tenants

It’s not all doom and gloom. In fact, distressed properties present major opportunities:

- Deep Cost Savings: Lower rents, generous concessions, free rent periods. Landlords will do anything to fill space.

- Flexible Terms: Shorter leases, early termination rights, buildout credits. You hold the cards.

- Upgraded Image: Move into a Class A building for a Class B price. Boost morale, attract talent, and impress clients.

If you know what you’re doing, distressed properties become strategic weapons. But you need the data to play the game right. Because regardless of how you use the information (whether its staying away or acting strategically on the suffering) the data is critical to have.

How to Identify Distressed Properties Like a Pro

Most signs of distress won’t show up in a listing flyer. You have to look under the hood—into the financial health of the asset, the landlord, and the loan behind it. Here’s how the pros do it—and how Reoptimizer® does it for you

Step 1: Dig into CMBS Data

Commercial Mortgage-Backed Securities (CMBS) are pools of loans sold to investors. If the property you’re considering has a CMBS loan, you can find out if it’s in trouble.

Platforms like Trepp and KBRA track these deals. Reoptimizer® integrates insights from these sources and more, flagging landlords on CMBS watchlists.

Key Metrics to Watch:

- Delinquent Loans: Missed payments or loans in special servicing are clear distress signals.

- High LTV (Loan-to-Value) Ratios: Over 70-80%? That’s high risk. The landlord has no equity cushion.

- Low Cap Rates: Falling cap rates mean falling income. A weak income stream = financial pressure.

- Debt Yield Below 8%: This measures how well the property’s NOI covers the debt. Lower yields signal lender anxiety.

Reoptimizer® does the math for you. No need to crunch spreadsheets or decode bond data.

Step 2: Analyze Market Conditions

National trends are one thing. Local market dynamics are what actually matter. Reoptimizer® breaks it down for you by market and submarket.

Watch for:

Vacancy Rates: Not just the city average. Look at your building type and class. Class B/C? Vacancy is often over 30%.

Net Absorption: If more space is leaving the market than coming in, that’s negative absorption. In places like New Jersey or LA, it’s widespread.

But beware of the averages. Even in distressed metros, some submarkets are outperforming. Newark might be losing tenants overall, but industrial corridors or downtown high-rises might still be hot.

Reoptimizer® helps you target these micro-opportunities.

Step 3: Use Tenant Reps + Software

Your real estate strategy is only as strong as the team and tools behind it. Pair experienced tenant reps who understand local market dynamics with software that sees what brokers and landlords won’t say out loud.

So, at the end of the day your portfolio is bolstered by a real estate team that includes experienced tenant reps who know the game and a platform that gives you the data edge.

Tenant reps bring the negotiation muscle. Reoptimizer® brings the insights that back it up.

Together, they help you:

- Avoid distressed assets with hidden risk

- Capitalize on distressed assets with real upside

- Track landlord financial stability across your entire portfolio

- Flag renewals and relocations at risk

Takeaways for Tenants

With every loan default, lease expiration, or capital shortfall, more buildings shift from stable to risky. If you’re still treating real estate decisions as location-first and finance-second, you’re playing yesterday’s game.

Today, strategic tenants are acting like landlords. They’re analyzing debt exposure, tracking ownership groups across markets, and using financial distress not just as a warning—but as an edge.

That level of insight doesn’t come from listing sheets or broker banter. It comes from data.

Reoptimizer® puts that data in your hands—integrated, real-time, and portfolio-wide.

So you don’t just spot trouble—you turn it into leverage.

The next distressed building you look at? It could be a problem you dodge—or an opportunity you own.

Either way, you’ll see it coming.

Get a demo. Start managing risk like it’s your balance sheet—because it is.