Florida’s been on a roll.

For years, the Sunshine State has built a reputation as one of the most business-friendly places in the country — no state income tax, competitive corporate taxes, pro-growth policies, and sunshine in more ways than one. When the pandemic scrambled where and how companies operate, Florida became a magnet. Firms relocated headquarters, expanded logistics footprints, and snapped up office space from Miami to Tampa to Orlando.

And now, that friendly environment just got friendlier — especially if you’re a tenant. Let’s discuss how the repeal of the state’s commercial lease sales tax changes the game for office and industrial users.

A Big CRE Tax is Gone

As of October 1, 2025, tenants across Florida no longer have to pay a state sales tax on commercial leases.That’s a huge deal for businesses.

Until now, Florida was the only state in the country that taxed businesses simply for renting commercial space.

The so-called “business rent tax,” created back in the 1960s, hit almost every type of commercial property — office, industrial, retail — and even applied to many of the extra line items baked into modern leases.

If you leased space in Florida, you weren’t just paying tax on base rent. You were also paying tax on CAM charges, insurance, utilities, property-management fees, and even real-estate taxes passed through by your landlord.

For large occupiers, that translated to six- or seven-figure annual costs.

Governor Ron DeSantis signed the repeal into law in June 2025, and it officially took effect this fall. The Florida Department of Revenue confirmed that the change wipes out both the state sales tax and county surtaxes on commercial leases.

Analysts estimate tenants will save around $900 million a year, collectively. (CoStar News).

Breaking Down What Changes (And What Doesn’t)

Here’s the simple version:

- What’s gone: the sales tax on commercial real-estate rent and related pass-throughs (for occupancy periods starting October 1, 2025 or later).

- What stays: short-term residential leases, storage, parking, and equipment rentals remain taxable under separate laws.

- Who wins: any business leasing office, warehouse, or flex space in Florida.

The nuance matters. The repeal applies to occupancy periods beginning on or after October 1 — not the payment date. So, if you paid October rent early but it covered September occupancy, that old tax still applies. Prepaid rent for periods starting October or later? No tax due.

Landlords also have to retool their billing systems to make sure they’re not accidentally charging sales tax after that date — and tenants should double-check invoices.

What This Means for Industrial Tenants

Florida’s industrial sector has been one of the state’s biggest economic engines since 2020.

According to Q1 2025 Industrial Figures, the state recorded over 4.5 million square feet of positive net absorption and maintained a robust 23.9 million sq ft under construction. Average asking rents reached $11.43 per sq ft, up nearly 9 percent year-over-year, reflecting steady demand from logistics, manufacturing, and e-commerce operators.

Those same companies — the ones leasing big-box warehouses in Lakeland, Jacksonville, or along the I-4 corridor — now get a quiet but powerful boost from the lease tax repeal. Under the previous rules, Florida levied a 2 percent state sales tax (plus local surtaxes) on commercial rent. That charge extended to CAM, insurance, and property-tax pass-throughs, which make up a meaningful share of total occupancy costs in most NNN industrial leases.

Starting October 1, 2025, that layer disappears. The impact isn’t flashy, but it’s financially real. For example, a tenant occupying 500,000 sq ft at roughly $12.50 per sq ft all-in would have paid about $150,000–$175,000 annually in lease-related sales tax, depending on county surtaxes.

Over a 10-year term, that’s $1.5–$1.7 million kept inside the business instead of remitted to the state. The takeaway for industrial occupiers is straightforward: Florida’s already-competitive logistics market just got cheaper to operate in.

It also improves Florida’s competitive position when companies run site-selection models against other Sunbelt markets.

Texas might still win on land availability, but Florida just erased a recurring tax expense that often tipped the scales.

What This Means for Office Tenants

The office world is a little different, but the benefit is just as tangible.

For multi-tenant buildings, landlords typically gross up operating expenses and pass them through based on a tenant’s share of the building. Those line items — janitorial, management fees, repairs, security — were all previously taxed. Starting this fall, they’re not.

That makes Florida offices slightly cheaper to occupy at a time when companies are re-evaluating what “right-sizing” really means. For tenants expanding into markets like Miami, Tampa, or Orlando, it’s one more reason the math works.

It also simplifies negotiations. Without the sales-tax line, deals can focus on the true economics — base rent, tenant-improvement dollars, and renewal flexibility — instead of calculating “tax on rent on pass-throughs.”

The Ripple Effects:

Easier modeling: CFOs and real-estate teams can now model Florida sites more cleanly. No extra step for sales tax on rent, no need to layer it into TCO formulas. For large portfolios comparing states, that clarity matters.

Portfolio expansion: Many companies that planted a flag in Florida after 2020 are now looking to grow. With this tax gone, expansion economics improve — whether that’s an extra industrial building on a logistics campus or additional office space in a mixed-use hub.

Lease clean-up time: Now’s the moment to check your leases. Any clause that says “tenant shall pay sales tax on rent” needs an update. So do your AP systems and CAM-reconciliation templates.

Landlords’ accounting software may lag; tenants should flag invoices that still include the old tax after October 1.

And for tenants negotiating renewals or new space, this is leverage. Ask for updated language confirming no tax will be charged on rent or pass-throughs, and a refund if it is.

What Tenants Should Do Now

If you’re a tenant with Florida operations (or planning to expand there), here’s your quick checklist:

- Audit your leases. Flag every Florida lease referencing “sales tax” or “business rent tax.” Update those clauses.

- Confirm with landlords. Make sure invoices for occupancy starting October 1, 2025, no longer include sales tax.

- Update your models. Remove the tax line from your TCO and NPV calculations for Florida locations.

- Communicate with finance/AP. Train teams on the timing rule — tax is based on occupancy month, not payment date.

- Use the moment. If you’re negotiating renewals or expansions, leverage the cost savings in rent discussions.

The Bottom Line for Tenants

Florida has always marketed itself as open for business. The repeal of its decades-old lease tax takes that slogan from marketing to reality.

For office and industrial tenants, this is a rare kind of win: a genuine, no-strings-attached reduction in occupancy cost. It’s cleaner books, easier modeling, and more cash to reinvest in operations.

So if your company moved to Florida during the pandemic or is thinking about expanding there now, it’s worth revisiting your real-estate strategy. The market was already hot — and after this change, it’s only heating up.

Smarter Site Selection Starts Here

Changes like Florida’s lease-tax repeal are exactly the kind of hidden factors that can make or break a location strategy.

CRESiteIQ™ by REoptimizer® tracks every one of them — from shifting tax policies and labor costs to transportation access and local market trends — so you’re never making decisions in the dark.

Whether you’re comparing warehouse sites across states or balancing rent savings against workforce reach, Site IQ surfaces the real numbers behind each option.

After a year of waiting for the commercial real estate rebound that never quite arrived, 2026 is shaping up as the year when patience finally pays off.

Sure, macro uncertainty is still in the air—interest rates are high, trade negotiations are messy, and policy changes are giving investors heartburn. But look past the noise and the story is clear: the foundations for a recovery are solidifying.

According to Deloitte’s latest 2026 Commercial Real Estate Outlook, more than 850 global CRE executives are cautiously optimistic. The industry isn’t sprinting toward a comeback—it’s jogging with purpose. And those who know where to look are already seeing real opportunities take shape.

Macroeconomics: Still Cloudy, but the Sky’s Lightening

Let’s start with the elephant in every investor’s boardroom: the macro picture.

Last year, most of us expected 2025 to mark a full-fledged turnaround. That didn’t happen. Persistent inflation, “higher-for-longer” interest rates, and trade tensions kept the brakes on. Eighty-three percent of Deloitte’s respondents still expect revenue growth by the end of 2026—but that’s down slightly from 88% a year ago. Meanwhile, 68% expect expenses to rise. Translation: optimism remains, but wallets are tightening.

And yet, the sentiment index Deloitte tracks—a quick read on overall optimism—sits at 65, down a touch from last year’s 68, but miles above the 2023 trough of 44. This isn’t despair. It’s disciplined optimism.

Executives still expect improvement across core CRE fundamentals—leasing, rents, and capital costs—over the next 12 to 18 months. The biggest concerns now? Capital availability, interest rates, and the cost of capital. No surprise there. But an encouraging twist: cyber risk dropped off the worry list, while employee retention rose. That’s a signal that firms are finally pivoting from “crisis mode” toward rebuilding teams and strategy.

Debt Markets: From Distress to Opportunity

If 2024 was the year of the loan maturity cliff, 2025–2026 could be the year lenders and borrowers finally climb it.

There’s no denying the hangover from legacy loans. Over $1.7 trillion in U.S. commercial mortgages are facing maturity, many underwritten when rates were in the 3–4% range. With today’s rates closer to 6.5%, refinancing is painful—and only one in five firms expect to pay off upcoming maturities in full.

But here’s the silver lining: new debt is healthier. With valuations stabilizing and underwriting standards tightening, new loan origination volume rose 13% in early 2025—and a staggering 90% year-over-year. Spreads have tightened, capital access is improving, and even traditional banks are easing standards.

Private credit is leading the charge. Alternative lenders—private funds, insurance companies, high-net-worth investors—now make up 24% of U.S. CRE lending volume, well above the 10-year average of 14%. Globally, private credit markets hit $238 billion in 2024 and are on track for $400 billion in assets under management by decade’s end.

The message? The “shadow lenders” are now the sunlight. With $585 billion in CRE dry powder waiting to deploy, liquidity is coming back, just from new directions.

Partnerships and Alliances: Power in Numbers

CRE has always been cyclical—but this cycle is also collaborative. The report highlights a major shift toward strategic partnerships and joint ventures as the go-to growth strategy.

Why? Scale and specialization. As the cost of capital rises, teaming up allows firms to spread risk, share expertise, and unlock new markets faster than going it alone.

Take the April 2025 alliance between Blackstone, Wellington Management, and Vanguard. It’s designed to integrate public and private market exposure and bridge active and passive investment strategies. The takeaway: partnerships are becoming the new M&A—leaner, faster, and more adaptable.

Survey data backs this up. Seventeen percent fewer respondents plan to pursue traditional mergers or acquisitions in 2026, but alliances are trending up. Larger asset managers (with AUM over $15B) are partnering for operational expertise—especially in data centers, healthcare, and specialized housing—while smaller firms (AUM under $5B) are using partnerships to enter new markets.

Even REITs are getting in on it. Ventas partnered with GIC, Singapore’s sovereign wealth fund, to co-invest in life-science and healthcare assets. Expect more of that: REITs teaming up with private capital to diversify and scale.

And it’s not just finance. Across the data-center boom, partnerships with energy suppliers and tech firms are emerging to manage power costs and sustainability goals. Equinix’s collaboration with Bloom Energy for on-premise natural gas generation is a leading example of how CRE and infrastructure are converging.

Sector Highlights: Digital, Industrial, and Office Make a Comeback

The Deloitte outlook underscores a clear reordering of property-type opportunities—and some surprises.

Digital infrastructure—data centers and cell towers—has reclaimed the top spot as the most promising asset class. Demand far exceeds supply; in nine major global markets, 100% of new construction is already pre-leased. Power constraints are creating new growth hubs in Central Washington, Berlin, and Singapore.

Industrial and logistics properties, while cooling slightly after years of outperformance, remain strong. Short-term trade turbulence is slowing leasing, but long-term fundamentals are robust thanks to onshoring and the need for supply-chain flexibility.

And here’s a headline few expected two years ago: offices are finding their footing. Both suburban and downtown spaces are rising again in investor rankings. With record-low new construction and a gradual return to workplace normalcy, top-tier office assets are gaining favor.

Beyond the “core four,” alternative sectors—healthcare, grocery-anchored retail, and senior housing—are drawing competition even in a low-growth environment. Deloitte notes that the share of “nontraditional” property types in CRE portfolios has grown 10% annually since 2000 and is set to accelerate through the next decade.

AI in Real Estate: From Hype to Hands-On

Last year, everyone in CRE was talking about AI. This year, they’re asking: “Okay, how do we actually make it work?”

According to Deloitte, 19% of organizations are still early in their AI journey, and 27% report implementation challenges—mainly around data quality, technical expertise, and change management. The hype has matured into a realism that’s actually more productive.

AI’s real traction is happening in specific, high-impact areas: tenant relationship management, lease drafting, and portfolio optimization. Smaller, domain-specific models—rather than giant general-purpose systems—are becoming the tools of choice.

Think of this as the “fit-for-purpose” phase of AI in real estate. Instead of one giant model doing everything, firms are deploying small language models trained on industry-specific data—like lease clauses, property valuations, or zoning rules. These models deliver faster, more relevant results without the heavy computing costs of big AI.

Deloitte’s guidance is spot-on here:

-

Embed explainability and human oversight into all AI workflows.

-

Make AI literacy a company-wide initiative, not just an IT project.

-

Tie AI pilots to clear business outcomes—lease efficiency, underwriting speed, or tenant retention—rather than chasing headlines.

The message is clear: AI isn’t magic—it’s a multiplier. When paired with strong data governance and human expertise, it can supercharge operational efficiency.

What CRE Leaders Should Do Now

Deloitte closes the outlook with a reminder that the early-mover advantage is fading. In other words, this is the window to act before the crowd floods back in.

Here’s the 2026 playbook in plain language:

-

Stay selective and agile. Don’t chase every shiny deal. Focus on sectors insulated from short-term shocks and keep dry powder ready for opportunistic buys.

-

Rebalance with discipline. Use data-driven portfolio reviews to shift capital toward resilient, income-generating assets.

-

Expand through partnerships. Whether it’s a joint venture or a capital alliance, collaboration is now a competitive edge.

-

Stress-test everything. From refinancing exposure to asset valuations, know your weak spots before the market does.

-

Deploy AI strategically. Invest in targeted applications that drive measurable performance, not buzzword compliance.

The Bottom Line: The Opportunities Are Real

The commercial real estate story for 2026 isn’t one of doom—or euphoria. It’s one of preparation and pragmatism.

Yes, macro headwinds remain. But capital is coming back. Lending standards are easing. Digital and industrial assets are growing. And AI is shifting from promise to practice.

For leaders willing to move decisively, the opportunities are real. The recovery may be slower than expected, but it’s still on track—and the market rewards those who don’t wait for certainty to act.

As Deloitte puts it: Don’t wait for the comeback—help build it.

The CRE rebound won’t wait, and neither should you. 2026 is the year for decisive operators. Capital is coming back, data is reshaping strategy, and every square foot counts.

REoptimizer® gives you the clarity, analytics, and foresight to move before the market — and lead the recovery, not follow it.

After decades of offshoring and just-in-time efficiency, U.S. companies are re-examining what it means to own their supply chains.

The next phase of industrial strategy isn’t about chasing cheaper labor overseas; it’s about control, resilience, and proximity.

And the reshoring initiative represents a full-scale corporate realignment reshaping where production happens, how capital is deployed, and what industrial real estate looks like.

Between now and 2028, the U.S. is entering what economists are calling a “reindustrialization window,” a rare convergence of policy, technology, and executive intent that’s pulling manufacturing back home.

But while the movement is powerful, it’s not without friction. For business leaders, tenants, site selectors, and industrial investors, understanding how reshoring plays out in real estate terms is now essential.

The Momentum: Business Leaders Taking Action

The reshoring initiative that once sounded aspirational has matured into measurable activity. According to 2025 outlook data, 29% of US companies are actively reshoring sourcing or production, up sharply from prior years.

Meanwhile, the share of CEOs planning to reshore operations within three years jumped another 15% year-over-year, signaling a decisive shift from strategy to execution.

That corporate intent is reverberating across the global supply chain. 59% of contract manufacturers now report they’ve either reshored production for clients, are in the process, or are quoting new reshoring projects. These cases mark a systemic recalibration in how manufacturing companies think about risk and reliability.

By 2026, 65% of companies expect to buy most key items from regional suppliers, nearly doubling the rate from just a few years ago. For business leaders responsible for keeping factories running, reshoring is powerful risk management.

The Reshoring Initiative and US Jobs

Over the next few years, reshoring momentum is expected to show up where it matters most — in jobs.

Roughly 174,000 new manufacturing positions tied to reshoring and foreign direct investment are projected for 2025, most of them in high- and medium-tech sectors.

That means growth is concentrated in industries like semiconductors, EV batteries, solar manufacturing, and transportation equipment — industries where automation, precision, and proximity to customers outweigh the search for cheap labor.

Federal policy has amplified that momentum. The Inflation Reduction Act and CHIPS and Science Act have been catalytic, turning tax incentives into real investment triggers.

From late 2024 through early 2025, semiconductor projects accounted for only 5% of all reshoring/FDI announcements but captured two-thirds of total foreign capital investment — roughly $102.6 billion. That’s a staggering figure, even in capital-intensive manufacturing.

States are competing hard.

Texas, South Carolina, and Mississippi are projected to lead the nation in reshored jobs this year, with Mississippi alone forecasted to surpass 12,000 new manufacturing positions.

Each of these markets combines a pro-business regulatory environment, labor availability, and access to infrastructure — all key factors in reshoring decisions.

For real estate investors, those jobs translate directly into space absorption.

A single 1,000-employee advanced manufacturing plant can command millions of square feet of high-spec industrial real estate. Add logistics, suppliers, and service providers, and the ripple effect extends across entire industrial corridors.

Why Now: A Combination of Policy, Risk, and Technology

The resurgence of domestic manufacturing is about the failure of the old model to absorb shocks.

After the pandemic exposed the fragility of global supply chains, companies started measuring not just cost, but continuity.

Geopolitical risk has surged to the top of executive agendas.

The share of CEOs citing it as a top reshoring driver has jumped 50% year-over-year, and tariffs have exploded as a motivator — up 454% in 2025 data. The so-called “China +1” strategy (diversifying supply chains away from China while keeping one foot in Asia) is now operationalized by 35% of firms.

This new corporate strategy is prioritizing supply chain resiliency as a competitive advantage.

Business executives increasingly recognize that regionalizing production helps balance efficiency with control. Shorter lead times reduce risk, simplify management, and deliver flexibility that pure cost-cutting can’t.

Forty percent of OEMs now say they’re willing to pay a 10–20% premium to shorten delivery times by five weeks. That’s a complete reversal of decades of cost-centric thinking. By 2026, as much as a quarter of global trade could relocate to new production regions — a tectonic shift in trade flows and logistics infrastructure.

Automation and the Skilled Workforce Puzzle

If the last industrial revolution was about offshoring, this one is about automation. The cost gap between the U.S. and low-cost countries is narrowing not because labor is cheaper, but because machines are smarter.

The global industrial robotics market is projected to hit $81.4 billion by 2028, closing the productivity divide and enabling reshored factories to operate with fewer, higher-skilled employees.

But technology alone can’t fill the talent gap. 28% of manufacturers cite labor shortages as a primary constraint on reshoring. Nearly half say it could take up to three years to fully staff new manufacturing plants. Compounding the issue, 72% report that outdated technology keeps them from attracting younger workers — a generational barrier as much as an operational one.

This is where industrial policy meets workforce development. Reshoring without education investment is an incomplete process. Skilled workforce pipelines — through community colleges, technical training, and corporate partnerships — are becoming as critical as infrastructure grants. The White House and state governments are responding with strategic incentives, but aligning workforce, capital, and capacity remains a delicate balance.

The Real Estate Impact: Strategic Footprints

For occupiers and investors in industrial real estate, reshoring is reshaping what, where, and how manufacturing space is built.

- Footprint Evolution

The era of massive, labor-dense factories is fading. New manufacturing plants are smaller, smarter, and more automated. Power capacity, data connectivity, and automation readiness now drive location decisions as much as highway access. - Geographic Diversification

While legacy industrial hubs like the Midwest and Sun Belt remain attractive, reshoring projects are spreading production to nontraditional markets — particularly those with affordable land, improving logistics, and a willing workforce. Secondary and tertiary cities with solid infrastructure and education resources are punching above their weight. - Incentive-Driven Site Selection

Tax incentives, energy credits, and streamlined permitting have become central to corporate strategy. Real estate decisions are increasingly tied to industrial policy — from the Inflation Reduction Act to state-level grants that help companies offset higher domestic costs. - Supply Chain Adjacency

Occupiers are clustering near suppliers to shorten supply chain loops. This “local-within-local” model — where manufacturing, assembly, and distribution sit within a few hundred miles — reduces exposure to logistics risk and strengthens supply chain resiliency. For landlords, that means growing demand for well-located, midsized industrial facilities rather than distant mega-centers. - Infrastructure as a Differentiator

Power reliability, broadband, and transportation infrastructure are now part of the corporate location strategy. Markets that can guarantee uptime will command premium rents. Automation requires not just square footage, but stability — and investments in grid and road capacity are fast becoming decisive factors.

The Contradictions: Growth Meets Friction

Despite the momentum, reshoring remains complex. The Kearney Reshoring Index shows that imports from low-cost Asian countries still grew faster than U.S. domestic output in 2024, suggesting that while the reshoring effort is expanding, it’s also encountering resistance. For some firms, it’s a “pause and reassess” moment — balancing ambition against cost pressures and labor availability.

U.S. manufacturing remains 10–50% more expensive than offshore competitors, even after accounting for logistics savings. Without broader reform (from permitting to energy to workforce readiness) reshoring manufacturing could plateau below its potential.

And yet, the momentum persists. Executives understand the economic risk of over-reliance on overseas production. The pandemic, trade disruptions, and regulatory volatility have underscored the importance of regional supply chains. In many cases, the question isn’t whether to reshore — it’s how to make the transition efficient.

Key Takeaways for Industrial Stakeholders

- Reshoring is real — and accelerating. With nearly a third of U.S. companies now executing reshoring strategies, this is no longer theoretical.

- Industrial real estate is ground zero. The push to bring manufacturing back is transforming demand patterns, building design, and corporate site strategy.

- Workforce is the new wildcard. Automation helps, but the skilled workforce gap could be the limiting factor of the decade.

- Policy alignment matters. Industrial policy and tax incentives are the new drivers of private investments. Tenants and developers who can align their projects with federal and state sponsors will capture the upside.

- Resilience is the new efficiency. In an economy defined by uncertainty, reshoring is less about nostalgia and more about risk management — building a supply base that bends, not breaks.

The Outlook: Manufacturing’s Future Is Local — and Strategic

In short, the next decade of U.S. manufacturing growth won’t look like the last. It will be more strategic, more distributed, and far more integrated with the real estate decisions that make it possible.

Reshoring is the new wave… a multi-year reallocation of capital that will determine which portfolios outperform, and which get left behind.

The winners will be the companies that can match manufacturing strategy with real estate agility.

REoptimizer® helps you do exactly that.

If your manufacturing or logistics footprint is evolving, now is the time to benchmark your locations, re-evaluate occupancy costs, and capture the incentives that will shape the next decade of industrial growth.

Learn more about how REoptimizer® helps industrial occupiers align reshoring strategy with real estate performance.

Industrial real estate has been on a wild ride over the past decade. From the e-commerce boom to pandemic-era supply chain reshuffling, warehouses and logistics hubs have gone from the quiet backbone of the economy to one of the most closely watched property sectors.

If you thought the industrial boom was slowing down, think again. Despite national rent growth averaging just 1.6% this year, some U.S. cities are bucking the trend in spectacular fashion.

According to CoStar’s September 2025 data, the top five metros leading the pack in industrial real estate rent growth are:

- Nashville, TN

- Charlotte, NC

- Orlando, FL

- Columbus, OH

- Washington, DC

These metros are seeing industrial asking rents rise at multiples of the national pace…So, let’s break down what’s driving the surge, why it matters, and what it signals for investors, occupiers, and developers.

Nashville: Music City Becomes Logistics City

Almost overnight, Nashville has become one of the most sought-after logistics markets in the U.S.

Nashville tops the charts with 6.7% annual rent growth, catapulting average asking rents to $12.19 per square foot—the highest in the Southeast. To put that in perspective, rents here are nearly 18% higher than Atlanta, long a heavyweight in the region.

But what’s behind Nashville’s rise?

- Population & Labor Boom: Among the fastest-growing metros in the country, Nashville’s influx of people and companies fuels demand for distribution and logistics space. With this comes a major labor market expansion fueled by corporate relocations and young workforce inflows

- Massive infrastructure investments—from airport expansions to interstate improvements

- Construction Challenges: Rocky soil and tricky topography make building expensive. Developers pass on those costs, inflating asking rents.

- Supply Dynamics: With 2 million square feet under construction—the most since Q3 2023—new supply is on the way, but not enough to dent landlord leverage yet.

Here’s the twist: demand has cooled slightly since early 2024. Net absorption (move-ins minus move-outs) has slowed, even as vacancies hover around a tight 6.1%. Some deals are stalling under the weight of elevated rents.

Even so, Nashville has logged 50% rent growth in the past five years, crushing the national average of 36%. E-commerce players and third-party logistics firms are clamoring for modern space. Forecasts suggest growth will cool to ~4% in late 2025 and 2026 before stabilizing—but in such a tight market, it’s unlikely tenants will find relief anytime soon.

Charlotte: The Big-Box Comeback

Charlotte is riding the wave of big-box leasing—where major tenants absorb vast footprints for logistics. This surge has pushed rents up nearly 6.5% annually, well above peer markets. It has rapidly become an industrial powerhouse of the Southeast.

Its location is no small factor: Charlotte sits at a strategic crossroads for logistics operators serving the Southeast, with easy access to major interstates, ports, and rail networks.

The result? Tenants are competing for limited space, driving rents upward. For institutional investors, Charlotte has become one of the most competitive industrial markets in the U.S., and it’s not slowing down.

- Absorption: Space is disappearing as fast as it’s built. Net absorption consistently outpaces expectations.

- Pipeline Pressure: The construction pipeline is shrinking, which means fewer new buildings to absorb growing demand.

- Strategic Advantage: Charlotte sits at a crossroads for Southeast distribution, making it a must-have for logistics players.

For tenants, Charlotte is a frustrating game of musical chairs. For landlords and investors, it’s music to their ears.

Orlando: Sunshine and Supply Chain Pressure

Orlando’s industrial story is about more than just theme parks. The Central Florida market has quietly become a logistics hotbed.

Key Drivers:

- Population Surge: Central Florida’s demographic expansion drives consumption and logistics needs.

- Sector Diversity: Demand isn’t just e-commerce—it’s aerospace, defense, and advanced manufacturing.

- Constrained Supply: Limited new construction has left high-quality facilities in short supply.

Vacancies remain tight, and leasing velocity is accelerating. Landlords have a strong upper hand in negotiations, and tenants looking for modern, Class A distribution space often find themselves facing bidding wars.

The bigger takeaway: Orlando is no longer just a regional logistics hub; it’s becoming a national player thanks to its diverse demand base.

Columbus: The Midwest Logistics Titan

If Nashville is hot and Orlando is up-and-coming, Columbus is the steady workhorse of industrial rent growth. It’s one of the most strategically important industrial markets in the country. Rents are up ~5.7% annually, making it the Midwest’s strongest performer.

Key Drivers:

- Location, Location, Location: Within a day’s drive of half the U.S. population, Columbus is indispensable for e-commerce and logistics networks.

- Big Tenant Deals: Large-scale logistics and manufacturing commitments are squeezing availability.

- Supply Balance: Construction is steady, but demand remains stronger.

Even with new construction underway, absorption is outpacing supply. Columbus has long been viewed as a “must-have” logistics market, but today it’s showing elite-level rent growth that rivals coastal metros.

For occupiers, this means Columbus is no longer a “cheap alternative”—it’s a competitive battleground where timing is everything.

Washington, DC: A Different Kind of Demand

The Washington, DC industrial market is a fascinating outlier. While the apartment sector there has softened, industrial demand remains rock-solid. Reaching an annual Rent Growth: ~5.6%, key drivers include:

- Defense & Federal Logistics: The government’s outsized footprint ensures steady space absorption.

- Distribution Role: DC serves both local consumption and broader Mid-Atlantic logistics.

- Vacancy Stability: Even as supply enters the market, vacancies remain tight.

In short, the federal government’s presence provides a built-in demand engine that insulates DC’s industrial sector from broader market slowdowns. For investors, it’s one of the few markets where industrial real estate behaves almost like a defensive asset.

Beyond the Top Five: Other Strong Performers

While Nashville, Charlotte, Orlando, Columbus, and DC are the headline-makers, several other metros deserve attention:

- Louisville, KY (~5.5%): Anchored by UPS’s Worldport, Louisville remains one of the nation’s premier air freight hubs.

- Milwaukee, WI (~5.4%): Steady growth driven by manufacturing and Midwest logistics positioning.

- St. Louis, MO (~4.3%): Strategic Mississippi River location fueling demand.

- Tampa, FL (~4.2%): Growth tied to population expansion and Gulf Coast trade.

- Philadelphia, PA & Chicago, IL (~4%): Large, mature markets where steady demand keeps rents climbing, though at a more moderate pace than the high-flyers.

The Bigger Picture: Why This Matters

So what’s the common denominator across these markets? Three themes emerge:

- Population Growth = Warehousing Demand

- Cities like Nashville and Orlando are seeing demographic booms that directly translate into more goods flowing in and out.

- E-Commerce and Logistics Power

- Columbus, Charlotte, and Louisville benefit from their strategic locations for national distribution.

- Constrained Supply Pipelines

- Even as construction has surged, supply is struggling to keep up with tenant demand, giving landlords pricing power.

In short, industrial real estate remains the darling of commercial property because it sits at the intersection of demographics, technology, and logistics—a trifecta few other asset classes can claim.

Final Word for Industrial Tenants

Industrial real estate is one of the hottest, active markets right now and when demand collides with constrained supply, rents don’t just rise; they soar.

But the race isn’t just about finding space anymore…it’s about knowing where and when to act.

Markets are moving fast, and tenants who benchmark against yesterday’s numbers risk locking themselves into costly deals that don’t reflect today’s realities.

That’s why benchmarking the is your competitive advantage. By tracking real-time rent growth, vacancy, and construction pipelines, companies can identify when to negotiate, where to expand, and how to avoid overpaying.

This is exactly where REoptimizer® comes in. Our platform empowers occupiers to:

- Benchmark markets with live, data-driven insights

- Spot opportunities in high-growth regions before competitors do

- Negotiate smarter by arming teams with transparent, comparable data

- Align portfolios with shifting population and logistics trends

Industrial real estate may be red-hot, but with the right tools, you don’t just keep up—you capitalize on growth.

Because in this market, the winners won’t just be those who secure space. The winners will be those who optimize it. Learn more today about how REoptimizer® can give your industrial portfolio a razor sharp edge Act before your competition does.

Distressed properties aren’t just someone else’s problem—they’re embedded risks and potential leverage points in your real estate portfolio.

Whether you’re consolidating space, renegotiating a lease, or eyeing a relocation, understanding the financial health of your landlord is critical due diligence in this new age.

Because when buildings face widespread loan delinquencies, expiring anchor leases, or NOI shortfalls, your tenancy is exposed to more than deferred maintenance. You’re looking at unreliable concessions, management instability, or worst case foreclosure-related disruptions. And this is no longer just a nightmare scenario, it’s a real landmine for tenants to dodge

But in the right hands, these same properties become tools for negotiation: below-market rents, flexible terms, and fast-track buildouts.

So, without further ado, let’s get into it. Here’s how sophisticated tenants identify, assess, and capitalize on distressed office assets…before the damage reaches their balance sheet.

What Qualifies as a Distressed Property?

In commercial real estate, a property becomes distressed when its income can no longer support its debt, operating costs, or both.

Often this comes with high vacancy, but beyond those numbers, it’s about financial instability that compromises the building’s ability to retain tenants, fund improvements, or even stay solvent.

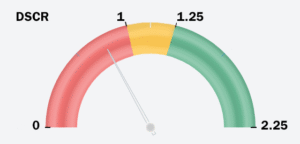

You’ll see the signs: debt service coverage ratios slipping below 1.25, rising rollover exposure, unsustainable concession packages, or a CMBS loan on a servicer’s watchlist.

Think of it as a ticking time bomb with a “For Lease” sign out front.

Red Flags to Watch for Property Distress:

Not all red flags wave in the open. Some are buried in the numbers (and if you miss them, you’re the one left holding the bag). These are the signs that a property’s on the brink:

- Loan Delinquencies: If the landlord can’t pay the mortgage, it’s your problem too. Look for Debt Service Coverage Ratios (DSCR) under 1.25—that’s danger territory.

- Vacancy Rates: High vacancy equals high risk. Fewer tenants mean less income, which makes default more likely.

- Occupancy vs. Vacancy: Don’t be fooled by current occupancy. Look at lease expirations. That 80% occupied tower could be 40% vacant in 12 months. You can consider low occupancy rates a dormant vacancy rate.

- Market Saturation: In oversupplied cities, landlords are bleeding cash just to stay afloat. That creates leverage for you—but also risk.

- Expiring Lease Clusters: Buildings with a high percentage of leases expiring in the next 1-3 years are at risk of a sudden occupancy collapse. If multiple anchor tenants walk, the building’s NOI—and your negotiating power—plummets.

In fact, nearly one-third of national CMBS office loans are distressed. In Chicago, that jumps to 75%. These aren’t isolated problems. They’re systemic. And they’re your opportunity—if you act smart.

Why You Should Care

It’s not just about whether your space looks fine today.

A financially unstable landlord introduces operational and reputational risk—especially in this market. Deferred maintenance, broken TI promises, lease buyouts, or even foreclosure-driven management shakeups can disrupt your business, whether you’re leasing a single floor or managing a 50-site portfolio.

Here’s the reality:

- Delayed Repairs: Capital improvements get slashed. HVAC breaks, and you’re sweating it out.

- Concessions Disappear: Promised TI allowances or free rent? Good luck collecting if the money’s gone.

- Lease Risk: If your landlord defaults, you could get caught in a foreclosure. That means legal headaches and operational chaos.

And here’s the kicker: your landlord might own 10 buildings. You lease in one. If they cross-collateralized their loans and one asset goes under, your “safe” space could get pulled into the mess.

Luckily, platforms like REoptimizer® flags these landlords before you get stuck with them.

The Upside: Strategic Advantages for Tenants

It’s not all doom and gloom. In fact, distressed properties present major opportunities:

- Deep Cost Savings: Lower rents, generous concessions, free rent periods. Landlords will do anything to fill space.

- Flexible Terms: Shorter leases, early termination rights, buildout credits. You hold the cards.

- Upgraded Image: Move into a Class A building for a Class B price. Boost morale, attract talent, and impress clients.

If you know what you’re doing, distressed properties become strategic weapons. But you need the data to play the game right. Because regardless of how you use the information (whether its staying away or acting strategically on the suffering) the data is critical to have.

How to Identify Distressed Properties Like a Pro

Most signs of distress won’t show up in a listing flyer. You have to look under the hood—into the financial health of the asset, the landlord, and the loan behind it. Here’s how the pros do it—and how Reoptimizer® does it for you

Step 1: Dig into CMBS Data

Commercial Mortgage-Backed Securities (CMBS) are pools of loans sold to investors. If the property you’re considering has a CMBS loan, you can find out if it’s in trouble.

Platforms like Trepp and KBRA track these deals. Reoptimizer® integrates insights from these sources and more, flagging landlords on CMBS watchlists.

Key Metrics to Watch:

- Delinquent Loans: Missed payments or loans in special servicing are clear distress signals.

- High LTV (Loan-to-Value) Ratios: Over 70-80%? That’s high risk. The landlord has no equity cushion.

- Low Cap Rates: Falling cap rates mean falling income. A weak income stream = financial pressure.

- Debt Yield Below 8%: This measures how well the property’s NOI covers the debt. Lower yields signal lender anxiety.

Reoptimizer® does the math for you. No need to crunch spreadsheets or decode bond data.

Step 2: Analyze Market Conditions

National trends are one thing. Local market dynamics are what actually matter. Reoptimizer® breaks it down for you by market and submarket.

Watch for:

Vacancy Rates: Not just the city average. Look at your building type and class. Class B/C? Vacancy is often over 30%.

Net Absorption: If more space is leaving the market than coming in, that’s negative absorption. In places like New Jersey or LA, it’s widespread.

But beware of the averages. Even in distressed metros, some submarkets are outperforming. Newark might be losing tenants overall, but industrial corridors or downtown high-rises might still be hot.

Reoptimizer® helps you target these micro-opportunities.

Step 3: Use Tenant Reps + Software

Your real estate strategy is only as strong as the team and tools behind it. Pair experienced tenant reps who understand local market dynamics with software that sees what brokers and landlords won’t say out loud.

So, at the end of the day your portfolio is bolstered by a real estate team that includes experienced tenant reps who know the game and a platform that gives you the data edge.

Tenant reps bring the negotiation muscle. Reoptimizer® brings the insights that back it up.

Together, they help you:

- Avoid distressed assets with hidden risk

- Capitalize on distressed assets with real upside

- Track landlord financial stability across your entire portfolio

- Flag renewals and relocations at risk

Takeaways for Tenants

With every loan default, lease expiration, or capital shortfall, more buildings shift from stable to risky. If you’re still treating real estate decisions as location-first and finance-second, you’re playing yesterday’s game.

Today, strategic tenants are acting like landlords. They’re analyzing debt exposure, tracking ownership groups across markets, and using financial distress not just as a warning—but as an edge.

That level of insight doesn’t come from listing sheets or broker banter. It comes from data.

Reoptimizer® puts that data in your hands—integrated, real-time, and portfolio-wide.

So you don’t just spot trouble—you turn it into leverage.

The next distressed building you look at? It could be a problem you dodge—or an opportunity you own.

Either way, you’ll see it coming.

Get a demo. Start managing risk like it’s your balance sheet—because it is.