In the last few years, the balance of power in commercial real estate has shifted.

Tenants are no longer blindly trusting landlords with their lease commitments.

Today, a savvy tenant demands hard proof of financial health—and the single most important metric to assess a landlord’s ability to stay afloat is the Debt Service Coverage Ratio (DSCR).

If you’re searching for office space, failing to evaluate a landlord’s DSCR could cost you more than just rent.

Deferred maintenance, unresponsive management, or worse—being stuck in a failing building heading toward foreclosure are more than likely.

The good news? REoptimizer® flags buildings on financial watchlists, including properties with a low DSCR, landlords linked to weak-performing assets, or even those cross-collateralized with distressed properties.

Here’s why checking the Debt Service Coverage Ratio (DSCR) is no longer optional.

What Is DSCR in Real Estate?

The Debt Service Coverage Ratio, also known as the debt coverage ratio, is a key financial ratio that measures whether a property generates enough net operating income (NOI) to meet its debt obligations. This includes loan payments, interest obligations, and principal repayments across the same period.

How to Calculate DSCR

DSCR = Net Operating Income (NOI) / Total Debt Service

Where:

- NOI (Net operating Income) is calculated as total income minus operating expenses, including cash taxes, capital expenditure, and income taxes.

- Total Debt Service includes annual debt payments, interest only payments, and principal and interest obligations.

This ratio is not just an underwriting tool for loan officers. It’s a litmus test of a property’s cash flow and the company’s ability to service debt over the long term.

Why Tenants Need to Understand DSCR

When a building has a low DSCR, it means the landlord may not have sufficient net operating income to cover their mortgage payments and business expenses.

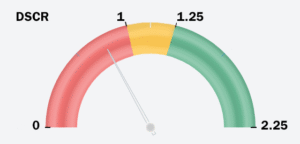

Most lenders set a minimum DSCR of 1.25, meaning the building must generate at least $1.25 in NOI for every $1.00 in annual debt service.

But here’s the catch: Even if the landlord is still making debt payments, a weak DSCR forces them to cut corners. Service disruptions like delayed HVAC repairs, reduced janitorial staff, or lack of security aren’t just possible—they’re likely.

That matters to you, the tenant, because:

- Your operating cash flow depends on a safe, functional workplace.

- Declining building standards hurt employee morale and productivity.

- You could be stuck in a lease while the landlord defaults.

REoptimizer’s® platform can help you avoid this risk altogether by highlighting:

- Properties with a DSCR below 1.25 (or another custom threshold)

- Landlords associated with negative cash flow or on lender watchlists

- Assets cross-collateralized with distressed buildings

This isn’t theory. It’s active risk mitigation for your real estate portfolio.

What Happens When DSCR Falls Below 1.0?

A DSCR below 1.0 means the landlord is not generating enough income to cover principal and interest payments. That can trigger a loan default, especially when most commercial banks enforce strict covenants in the loan agreement.

And when defaults happen:

- The lender may file for foreclosure

- A special servicer or court-appointed receiver may take over

- Routine operating expenses and capital improvements get deprioritized

In essence, long-term debt takes precedence over everything else—including your comfort, service quality, and workplace standards.

If your broker isn’t telling you this, REoptimizer® will.

A Healthy DSCR Indicates Healthy Cash Flow

A higher DSCR means the property generates enough NOI to:

- Cover debt service

- Invest in improvements

- Plan for long-term capital expenditures

Think of DSCR like a pressure gauge on the landlord’s financial health. Anything above 1.35 is generally considered financially stable. This tells you the property:

- Can handle market fluctuations

- Is likely to remain solvent even if a tenant defaults

- Has room to fund tenant improvements, lobby upgrades, or amenity additions

As a tenant, you want to be in an investment property that’s healthy, not just surviving.

How REoptimizer® Flags Problem Properties Using DSCR Data

When searching for space using REoptimizer®, you don’t just get square footage and price. You get access to debt coverage data that identifies risky assets upfront.

REoptimizer® helps you:

- Avoid buildings with red-flag financing structures

- Identify properties with low NOI relative to annual debt service

- See if your prospective space is cross-collateralized with a failing asset

This empowers your strategic planning process, helping you focus only on financially sound properties.

What Tenants Can Do to Protect Themselves

Tenants are no longer powerless in lease negotiations. If a building’s DSCR looks weak, you should:

- Request the landlord’s income statement and debt schedule

- Ask to review the loan terms for interest only payments, balloon payments, or resets

- Demand protections like:

- Right of offset (allowing you to deduct service costs from rent)

- Self-help clauses (so you can pay for repairs and subtract from lease payments)

These lease clauses are critical tools to guard against financial distress on the landlord’s side. But more importantly, don’t even consider these properties if REoptimizer® flags them as unstable.

Don’t Sign Blind—Use REoptimizer® to See the Full Picture

In today’s office market, DSCR matters more than ever. As a tenant, your business’s DSCR may be strong—but if your landlord’s isn’t, you’re the one who will pay the price.

Use REoptimizer® to:

- Ensure your lease is backed by sufficient income and stable debt service

- Eliminate hidden risks like cross-collateralization and ballooning debt

- Focus only on financially sound properties with healthy net operating income

Your workplace matters. So does your landlord’s ability to maintain it.

Explore REoptimizer® now to identify high-risk properties before you ever tour them. Don’t just find space—find space that works for your company’s future.