In a year that once again tested expectations across commercial real estate, 2025 emerged not as a dramatic turnaround story but as a strategic inflection point—particularly for office and industrial sectors.

For corporate tenants and CRE teams navigating hybrid work, supply chain shifts, and capital market stress, the data tell a clear story: performance now hinges on precision, not prediction.

1. Office Market: Stabilizing — But Still Reshaping Demand

After years of pandemic-era contraction, the U.S. office market showed meaningful signs of stabilization in 2025—even if the recovery remains uneven and deeply contextual.

Attendance Patterns Point to Growing Stability

Office traffic has steadily climbed throughout the year, with national office attendance approaching 72.6% of pre-COVID levels in 2025 according to foot-traffic analytics. This marks a dramatic increase from the pandemic troughs and represents one of the strongest rebounds since 2020.

These attendance gains have real economic implications. Not only do they support stabilization in rental dynamics and tenant confidence, but they also provide the workforce presence necessary to justify continued investment in office space, amenities, and hybrid collaboration zones.

Additionally, the proportion of corporations actively tracking attendance jumped to 69%, reflecting a growing recognition that employee attendance data are not just operational but strategic for measuring impact on productivity, utilization, and tenant experience.

Vacancy Remains High, But Market Fundamentals Are Improving

Office vacancy, though elevated compared to historical norms, edged slightly lower in 2025. National vacancy hovered around 18.6% in late 2025, a modest dive relative to the record highs it experienced through 2023–24.

In major gateway markets like New York City, vacancy pressure is easing. Moody’s data show that while vacancy rates remain above long-term averages, net absorption turned marginally positive in 2025, a sign that employers with clear hybrid strategies are contributing to localized demand growth.

Meanwhile, leasing activity in key submarkets underscored renewed confidence. Downtown Manhattan saw vacancy fall to 23% with average asking rents rising by over 3% year-over-year—a strong performance relative to broader national trends.

Flight to Quality Persists

Vacancy is no longer a single market condition—it’s a two-tier outcome tied to asset quality. And the 18.6% average vacancy can be misleading when we look at it as a whole. The more important story for occupiers is the duality inside that number.

The office market isn’t recovering uniformly; it’s splitting by asset quality and by submarket, creating a widening performance gap between buildings that can win talent back (and justify on-site days) and those that can’t.

Across major markets, leasing activity continues to tilt toward Trophy/Class A, while Class B/C’s share shrinks—a pattern that effectively pulls fundamentals upward for the best assets while leaving commodity stock behind.

Manhattan is one of the clearest examples of this duality: Trophy properties captured 61.6% of Manhattan leasing activity in Q1 2025 (by class), an unusually concentrated signal that tenants are choosing “best-in-market” space even when overall demand is still recovering.

Why This Matters For Corporate Tenants

Flight to quality is often framed as a landlord story. For occupiers, it’s a portfolio performance lever:

- Trophy/Class A is becoming the “utilization bet.” If your workplace strategy relies on consistent in-office patterns to drive collaboration and culture, premium assets increasingly act like the infrastructure that makes that behavior easier to sustain.

- Class B/C is becoming a repositioning / pricing bet. There can be value, but the underwriting has to assume higher volatility and larger gaps between “leased” and “used” space—plus greater reliance on concessions and landlord capex to stay relevant. (This is why conversion/repositioning talk keeps rising in market reports.) Not to mention a lot of these assets are being phased out of the market completely as conversions take shape.

2. Industrial: Continued Demand, With Nuanced Supply Dynamics

Industrial real estate sustained its long run of relative strength in 2025, even as supply and demand shifted toward equilibrium.

Long-Term Occupancy Growth Is Unbroken

Industrial tenant demand remained positive for the 60th consecutive quarter, a streak that now spans nearly 15 years—a testament to structural drivers such as e-commerce logistics and manufacturing rebalancing.

However, industrial vacancy did tick higher, reaching around 7.3% in Q2 2025, as move-outs and completions both contributed to slight softening.

Rent Growth Moderates, but Demand Diversity Expands

Industrial rent growth softened compared to the rapid gains of the pandemic era.

That said, diversification within the sector—especially toward cold storage, last-mile logistics, and automation-ready assets—continues to support strategic leasing and long-term tenant retention.

For tenants, this trend underscores the increasing importance of site selection analytics that match inventory with evolving supply chain footprints rather than broad assumptions of generalized growth.

The Construction Pipeline: Why Rent Growth Didn’t Collapse

That demand diversification is landing at the exact moment the industrial pipeline is drying up—which is a big reason rent growth moderated instead of falling off a cliff.

- Space under construction fell ~61% from the 2022 peak, dropping to ~279M SF in Q1 2025, with forecasts calling for the pipeline to dip below 250M SF by year-end.

- At the start of 2025, nationwide industrial construction was already down ~25% year-over-year, signaling a clear pullback in new supply.

The supply picture also explains the “two-speed” industrial market corporate tenants are feeling: vacancy rose to ~7.1% nationally in Q2 2025, yet small warehouses (<100K SF) stayed tight at ~4.4% vacancy—exactly the segment most aligned with last-mile and serviceable infill demand.

Net: 2025’s pipeline reset is quietly supporting pricing power in the right product types—especially smaller, well-located, higher-spec space—while pushing tenants toward sharper site selection analytics to avoid being trapped between soft big-box supply and scarce infill options.

3. Capital Markets and CRE Valuations: Discipline and Divergence

2025’s capital markets landscape accentuated a central reality: value is emerging at the intersection of risk management and operational data.

- Persistent headwinds in office valuations continued, with commercial property values still well below pre-pandemic levels in many categories.

- Conversely, industrial and select retail assets maintained relative valuation resilience due to consistent demand fundamentals and niche structural drivers.

For CRE teams, this divergence is a reminder that portfolio performance is not monolithic. Markets like Sun Belt logistics hubs and high-amenity urban cores are commanding differentiated risk premiums based on robust utilization and tenant demand clarity.

4. CRE Tech & Analytics: A Strategic Imperative

Perhaps the most pervasive trend of 2025 is the integration of advanced analytics, automation, and real-time occupancy intelligence into every layer of CRE decision-making.

From attendance tracking that informs space allocation and workplace strategy to predictive models that anticipate lease expirations and submarket pricing shifts, CRE technology is now a core operational competency—not a novelty.

This evolution reflects a broader shift from reactive portfolio maintenance to strategic portfolio optimization powered by reliable, real-time data.

And no where is the promise of real time data more profonde than the emergence of AI. It’s really the elephant in the room when we talk about the trends that have taken shape in 2025.

A Global Real Estate Technology Survey captures the moment bluntly: ~90% of organizations are piloting AI, yet only ~5% report achieving all (or most) of their AI goals—a gap that signals both massive momentum and a lot of wasted spend if the data foundation isn’t ready.

What AI Changes For Corporate Tenants And CRE Teams

AI isn’t just making reporting faster. It’s starting to rewire how portfolios are run:

- From static planning to continuous optimization: AI-enabled platforms can blend utilization, lease terms, operating costs, and market data to surface opportunities in near-real time (not quarterly).

- From “attendance” to predictive operations: The next step after occupancy dashboards is AI that flags leading indicators—teams drifting off hybrid norms, sites with creeping underutilization, rising overtime exposure, or policy exceptions that create compliance risk—early enough to intervene.

- From workflow automation to measurable efficiency: Morgan Stanley Research estimates AI could drive $34B in efficiency gains for the real estate industry over the next five years (through 2030) by automating tasks and improving productivity—exactly the kind of savings corporate occupiers will expect their CRE orgs to capture.

Right now, companies are pouring billions of dollars into the development of AI technology. For now, we’re in a bit of a watch and wait mode to understand how its full potential will affect workforce dynamics. But not to mention, it stands ready to slash hundreds of thousands of jobs.

Looking Ahead: 2026 and Beyond

As we close the books on 2025, a few imperatives emerge for corporate tenants and CRE teams:

- Measure utilization meaningfully: Moving beyond nominal occupancy figures to correlated productivity and performance metrics will define competitive advantage.

- Anticipate hybrid dynamics: The office is no longer “either dead or alive”; it is a flexible, culture-dependent asset whose value must be quantified, not assumed.

- Diversify CRE strategy by sector insight: Industrial dynamics will continue to strengthen, but their performance will be location and use-case specific.

- Embed analytics in every decision: From attendance data to portfolio repositioning, advanced data platforms are no longer optional—they are essential.

2025 wasn’t a year of simple narratives. It was one defined by data-informed nuance, measured progress, and strategic recalibration. For forward-thinking tenants and CRE professionals, the lesson is unmistakable: precision beats prediction.

Turn Insight Into Action With REoptimizer®

If precision beats prediction, then 2026 belongs to the teams that can see their portfolios clearly—and act faster than the market.

REoptimizer® gives corporate tenants a single, decision-ready view of performance across office and industrial portfolios, connecting utilization, attendance, market dynamics, and workforce signals into one strategic platform. Instead of reacting to headlines or relying on averages, CRE teams can identify what’s working, what’s at risk, and where to optimize—before costs, compliance, or underutilization compound.

With REoptimizer®, you can:

-

Measure real utilization—not just leased space

-

Align hybrid strategy with actual attendance and productivity signals

-

Compare asset performance across markets, building types, and use cases

-

Surface risks and opportunities early, using reliable, real-time data

The next CRE cycle won’t be managed quarterly—it will be optimized continuously.

See how leading corporate tenants are using REoptimizer® to turn insight into advantage.

👉 Book a demo and get a portfolio-level view of what your data is already telling you about 2026.

Book a Demo

November 2025 delivered the strongest November office occupancy since 2019 when measured by average visits per working day, even though total visits remain below pre-pandemic levels. In other words: office attendance is rising, but it’s rising unevenly—and the “headline” number can be misleading if you don’t normalize for working days.

For corporate tenants managing large-scale portfolios, that distinction matters. Because when you’re making lease, space-planning, and operating decisions across multiple markets, you’re ultimately trying to answer a simple question:

Are we getting the physical presence we’re paying for—and is it improving team productivity and business operations?

This is where attendance tracking, workforce analytics platform capabilities, and disciplined employee attendance management separate reactive portfolio management from proactive strategy.

Why “Visits” Aren’t Enough For Corporate Tenants

Placer.ai’s index can tell you how buildings are being used at the market level. But inside an enterprise portfolio, you need accurate attendance intelligence that connects:

- Employee attendance and attendance patterns by site, day, and team

- Time and attendance and employee hours for operational planning

- Productivity metrics and outcomes (not just bodies in seats)

- Compliance with labor laws, especially for non exempt employees

- Labor costs, including monitor overtime controls and scheduling waste

The gap between “the city is recovering” and “our portfolio is performing” is often just one thing: reliable, decision-grade attendance records and accurate records you can trust.

The New Reality: Market-Level Office Attendance Is Diverging

The November 2025 story is not a single national narrative—it’s a set of local stories that impact tenant strategy.

Sun Belt Momentum And Commute Dynamics

Miami maintained its lead in the office recovery and widened the gap versus New York, supported by corporate relocations and commute dynamics.

Weather, Transit, And Attendance Softness

New York saw attendance ease, with seasonal weather and transit-heavy commutes weighing on in-office days.

Tech Markets Showing Real Rebound Signals

San Francisco recorded some of the strongest year-over-year gains, signaling a meaningful turnaround, with other tech-influenced markets (Denver, Chicago, Boston) also improving—while still below pre-pandemic levels.

Policy And Local Economics Still Create Downside Risk

Houston and Washington, D.C. posted year-over-year declines tied to local industry/policy headwinds, including shutdown spillover. For tenants, this widening divergence means you should stop assuming one return-to-office playbook works everywhere. The portfolio winners will be the ones who can measure attendance precisely, then adapt site strategy accordingly.

From Counting Heads To Managing Risk: Attendance Monitoring As A Control System

In large portfolios, tracking employee attendance isn’t just an HR function—it’s risk management. Weak attendance monitoring can create:

- Compliance issues and compliance risks (meal/rest rules, overtime, scheduling documentation)

- Payroll errors and payroll mistakes caused by bad time capture

- Time theft and buddy punching when systems rely on unchecked manual inputs

- Higher employee absenteeism, poor attendance, and lost productivity

- Inconsistent treatment that can trigger disputes or disciplinary action risk

If you’re still relying on manual systems (spreadsheets, ad hoc badge checks, manager estimates), you’re not just missing insight—you’re increasing operational exposure.

What A Modern Attendance Solutions Stack Looks Like

Corporate tenants increasingly need attendance solutions that unify workplace utilization with employee time controls—without turning the office into a surveillance zone.

A pragmatic enterprise approach usually includes:

1) Employee Attendance Software That Produces Reliable Data

Look for employee attendance software and attendance software that supports:

- Real time tracking and real time attendance

- Automated systems for clock-ins, exceptions, and approvals

- Comprehensive reports for leaders and hr teams

- Clean integrations for payroll processing and time off requests

- Auditable employee attendance records and attendance records

2) Time Tracking That Matches How People Actually Work

In hybrid reality, you need time tracking that can:

- Track time for remote employees and remote workers

- Support flexible schedules and modern work patterns

- Help monitor overtime without punishing legitimate flexibility

- Provide valuable insights into staffing, not micromanagement

3) Optional Stronger Identity Controls Where Risk Requires It

In certain environments (high-security, regulated, or high time-theft exposure), organizations may consider:

- Biometric time clocks

- Facial recognition

- Secure on-site check in workflows: These can reduce security risk, prevent buddy punching, and improve the integrity of employees clock events—but should be deployed with clear purpose, transparency, and policy governance to protect a positive work environment.

Portfolio Use Cases That Actually Move The Needle

Here’s how tenants use attendance monitoring and analytics to improve outcomes (without “cramming” a mandate everywhere):

Space Planning And Lease Strategy

Use attendance data to identify underutilized sites, then right-size footprints, adjust amenity investment, or renegotiate renewal terms based on real demand.

Team Collaboration And In-Office Design

If your goal is better team collaboration, don’t guess. Compare attendance patterns to meeting density and project milestones. Design on-site days around collaboration, not routine solo work.

Productivity And Cost Control

Tie employee productivity and team productivity to a small set of measurable signals:

- Focus time vs. meeting time

- Cycle times and throughput

- Productivity metrics by team and site: Then decide where “in office” truly improves outcomes—and where remote execution is more effective.

Early Signs And Intervention

Use analytics to spot early signs of systemic issues: spikes in unplanned absences, schedule friction, approval bottlenecks, or manager-level inconsistencies. Pair this with wellness programs or workload adjustments before problems become attrition.

Maintain Compliance Without Killing Culture

Corporate tenants can ensure compliance and still support flexibility if they treat attendance as policy + systems + fairness:

- Document clear attendance policies and how exceptions work

- Configure rules by employee category (especially non exempt employees)

- Keep work hours and overtime logic consistent across locations

- Use systems to reduce disputes: auditable accurate records prevent “he said / she said”

When done well, managing attendance becomes a trust-building operating rhythm—not a morale drain.

Frequently Asked Questions About Employee Attendance Tracking

What’s The Difference Between Office Attendance And Employee Attendance?

Office attendance often measures building usage (visits), while employee attendance tracking focuses on who worked, where, and when—supporting scheduling, compliance, and payroll accuracy.

Why Do Corporate Tenants Need Attendance Tracking If They Have Access Control Data?

Badge swipes can indicate entry, but they often don’t produce compliant employee attendance records, don’t support time and attendance rules, and can miss hybrid patterns or onsite duration needed for operational decisions.

How Do We Monitor Attendance Without Micromanaging?

Focus on outcomes and exceptions. Use attendance monitoring to run business operations (staffing, space, compliance), not to scrutinize every minute. Make reporting transparent and limit access to role-based needs.

How Does Attendance Tracking Reduce Payroll Errors?

By automating capture and approvals, and integrating with payroll, you reduce manual edits, missed punches, and inconsistent rounding—common causes of payroll errors and payroll mistakes.

What Corporate Tenants Should Do Next With REoptimizer®

If you’re managing a large portfolio, the next phase of the office recovery isn’t about guessing—it’s about governing with data.

REoptimizer® helps corporate tenants:

- Create a single source of truth for employee time and attendance across every location—so leadership, HR teams, and operations are aligned.

- Replace manual systems with automated, reliable data that supports accurate records, fewer payroll errors, and stronger compliance.

- Track what matters in one portfolio view: real time attendance, overtime exposure, absence trends, and site utilization—so you can spot issues early and act fast.

- Use workforce insights to refine hybrid strategy so in-office time improves collaboration and team productivity—not just policy compliance.

Office attendance may be hitting post-pandemic highs, but portfolio advantage comes from what you do next. When markets diverge and every square foot has to justify itself, REoptimizer® turns attendance data into clear actions—so you can reduce risk, control labor costs, and optimize space with confidence.

Ready to see what your portfolio is really telling you? Request a REoptimizer® demo and get a portfolio-level attendance and utilization readout tailored to your footprint.

Book a Demo

Commercial leases don’t just have “terms.” They have deadlines—and missing one can cost you renewal rights, expansion space, tenant improvement dollars, or trigger default. This guide breaks down the most important lease dates to track, what they mean, and how to stay protected.

Quick Answer: What Are The Key Dates In A Commercial Lease?

The most important dates in a commercial lease usually include:

-

Delivery Date (when the space must be ready)

-

Lease Commencement Date (when the lease legally starts)

-

Rent Commencement Date (when billing begins)

-

Rent Escalation Dates (when rent increases)

-

Option Notice Windows (renew, terminate, expand, downsize)

-

CAM / Operating Expense Reconciliation & Audit Deadlines

-

Insurance & Certificate of Insurance (COI) Renewal Dates

-

Security Deposit / Letter of Credit (LOC) Expiration & Step-Down Dates

-

Assignment/Sublease Consent & Recapture Deadlines

-

Restoration, Surrender, and Move-Out Dates

-

Termination Date and Holdover Period Triggers

If you track nothing else, track these.

Why Key Lease Dates Matter (And Why Tenants Lose Money)

Most commercial leases make it 100% the tenant’s responsibility to:

-

remember critical dates, and

-

deliver notice exactly the way the lease requires.

Landlords don’t have to remind you. And many are perfectly happy if you miss a renewal window, lose a right to expand, or default on an administrative technicality.

The Portfolio Problem: One Lease Is Manageable—Twenty Isn’t

Tracking lease dates for a single location is hard enough. Tracking them across an entire portfolio is where tenants get hurt.

Because once you scale to multiple sites, you’re no longer managing a “lease.” You’re managing a deadline ecosystem, with hard stops and serious liability.

One missed renewal window can wipe out your leverage. One missed CAM audit deadline can lock in overcharges. One delayed delivery can force holdover tenancy with penalty rent and potential damages. And spreadsheets? They don’t protect you when the real landmines are notice requirements—the exact method, address, timing, and proof that make or break your rights.

If you manage multiple locations, you need more than reminders—you need a system built for lease deadlines. REoptimizer® helps track critical dates, notice windows, escalations, and portfolio exposure in one place, so you don’t lose options, overpay rent, or get trapped in holdover. See how it can streamline your portfolio and book a demo today.

Book a Demo

The “Trigger Chain”: Dates That Control Other Dates

A best practice is to map your lease like a domino run:

Delivery Date → Lease Commencement → Rent Commencement → Escalations → Option Windows → Termination/Surrender

A surprising number of disputes come down to: which date triggered which obligation.

1. Delivery Date (When The Space Must Be Ready)

Definition: The date the landlord must deliver the premises in the condition required by the lease.

What Tenants Should Tie To The Delivery Date

-

Required Condition Standard (code-compliant, clean, safe, systems working)

-

Utilities/Services Live (HVAC, electric, water, internet readiness)

-

Punch List Process (walkthrough, deficiency list, cure timeline)

-

Remedies If Late (rent delay, per diem penalties, termination right, reimbursement)

Why It’s Critical

A late delivery can force a business into:

Tenant tip: Your lease should define “delivered” clearly—otherwise a landlord can argue the space is “ready” when it’s not ready for your operations.

2. Lease Commencement Date (When The Lease Legally Starts)

Definition: The date the lease term officially begins.

This date often controls:

-

The Lease Term End Date

-

When Options Can Be Exercised

-

When Certain Obligations Begin (insurance, maintenance responsibilities, reporting)

Watch for: “earlier of” and “later of” language. Many leases say commencement is the earlier of occupancy or a set date—meaning you might trigger obligations by moving in early.

3. Rent Commencement Date (When You Start Paying)

Definition: The date rent starts accruing—often different from lease commencement.

Common Rent Commencement Structures

Free Rent Isn’t Always Free

Many leases make free rent conditional:

-

Base Rent Only (not CAM/operating expenses)

-

Abatement Ends If You Default

-

The “Free Months” Extend The Lease Term (e.g., 120 months of paid rent becomes 132 months total)

4. Rent Escalation Dates (When Rent Increases)

Definition: The recurring date rent increases (often annually).

Common Rent Escalation Types

-

Fixed Percentage Increases

-

CPI Adjustments (with caps/floors sometimes)

-

Stepped Increases (pre-set schedule)

-

Fair Market Adjustments (typically at renewal)

Why It Matters

Escalations are cumulative—they compound across long terms. A “small” clause can become a major cost driver over 7–15 years.

Tenant tip: Track escalation dates and the formula inputs (CPI base year, index month, cap/floor, rounding rules).

5. Option Notice Windows (Renew, Terminate, Expand, Downsize)

Definition: A set window when a tenant must give notice to exercise a right.

This is the #1 category tenants miss.

Options Usually Include

-

Renewal / Extension Options

-

Early Termination Options

-

Contraction Or Downsize Options

-

Expansion Options (ROFO/ROFR or fixed space options)

The Real Trap: Notice Rules

A tenant can “send notice” and still lose the right if:

-

Notice Method Is Wrong (email not allowed)

-

Sent To The Wrong Address

-

Missed The Window By A Day

-

Lacked Required Enclosures (financials, proposed terms)

Best practice: Track both:

6. Right of First Offer (ROFO) (Expansion Timing Advantage)

Definition: Before the landlord markets certain space, they must offer it to the existing tenant first.

Key dates to track:

If you can’t respond fast, you lose the shot.

7. Right of First Refusal (ROFR) (Match A Third-Party Deal)

Definition: Landlord can market space, but must let the existing tenant match the third-party deal.

Key dates to track:

Practical difference: ROFR can slow deals, but gives the tenant a chance to “match” a real market offer.

8. CAM / Operating Expense Reconciliation And Audit Deadlines

This is one of the most expensive “hidden” date categories.

Key dates:

-

Annual Reconciliation Statement Delivery Date

-

Tenant Dispute Window (often 30–180 days)

-

Audit Request Deadline

-

Payment Due Date For Under-Billings

Tenant tip: If you miss the dispute window, many leases treat the landlord’s statement as final—even if it’s wrong.

9. Insurance Renewal And COI Deadlines

Many leases require:

-

Specific Coverage Types/Limits

-

Landlord Named As Additional Insured

-

COIs Delivered Annually or upon renewal

Key dates:

-

Policy Expiration

-

COI Delivery Deadline

-

Renewal Bind Date

Missing this can be a technical default even if you’re otherwise a perfect tenant.

10. Security Deposit / Letter Of Credit (LOC) Dates

If you have an LOC, date tracking is non-negotiable.

Key dates:

Tenants get defaulted all the time for simply failing to renew an LOC on time.

11. Assignment / Sublease Consent And Recapture Deadlines

If you plan to sublease or assign the lease:

Key dates:

-

Tenant Request Submission Date

-

Landlord Response Deadline

-

Recapture Election Deadline

-

Execution Deadline For Sublease/Assignment

12. Restoration, Surrender, And Move-Out Dates (The Endgame)

The termination date isn’t your only end-of-lease date.

Key dates:

-

Restoration Notice Deadline (landlord tells you what must be removed)

-

Decommission Start Date (IT, cabling, supplemental HVAC, signage)

-

Final Walkthrough Date

-

Key Return/Access Shutoff Date

-

Move-Out Completion Deadline

13. Termination Date And Holdover Trigger

Definition: The date the lease ends and you must be fully out.

If you stay past it, you can trigger:

Tenant tip: Track a move-out runway (60–180 days out) so surrender doesn’t become a crisis.

The Tenant’s Critical Date System (Best Practice Checklist)

To make lease date tracking actually work, log each critical date with:

-

Deadline Date

-

Earliest Notice Date (if applicable)

-

Notice Method + Address(es)

-

Owner (primary person responsible)

-

Backup Owner

-

Proof-Of-Delivery Requirement

-

Linked Lease Clause Reference

A calendar reminder alone is not enough if your lease requires certified mail to a specific address by a specific time.

FAQ: Key Dates In Commercial Leases

What is the most important date in a commercial lease?

For most tenants: Rent Commencement Date (when payments begin) and option notice deadlines (renewal/termination). These two categories drive the biggest financial outcomes.

Are lease dates the tenant’s responsibility?

In most leases, yes. The tenant is typically responsible for tracking dates and providing proper notice exactly as required.

What happens if I miss a renewal notice deadline?

You may lose the renewal option entirely and be forced to vacate or renegotiate at a much higher rent—often with reduced leverage.

Never Miss a Key Date

Tracking critical dates is a business imperative—but it’s only one part of optimizing a lease.The real advantage comes from seeing every deadline, notice window, escalation, and expansion right across your entire portfolio—before it turns into a costly mistake.

REoptimizer® is built to do exactly that: centralize your lease obligations, surface upcoming risk, and keep you ahead of renewals, CAM deadlines, LOC expirations, and holdover exposure. If you’re still relying on spreadsheets and calendar reminders, you’re one missed notice away from losing leverage.

Book a REoptimizer® demo to see how portfolio-wide critical date management actually works—and how much money and risk you can pull back into your control.

Book a Demo

CRE transaction management software is a platform that helps you run commercial real estate deals end-to-end—from requirements and site selection through negotiations, approvals, documentation, and close—so every deadline, cost, and decision is tracked in one place (instead of living in spreadsheets, inboxes, and scattered folders).

REoptimizer® is built for exactly this: centralizing portfolio data and automating reporting, alerts, and workflows so teams can move faster and negotiate from a stronger position.

Who Can Benefit from CRE Transaction Management Software?

If your organization has more than a few locations—or multiple deals happening at once—transaction management software becomes a necessity, not a “nice to have.”

Typical users include:

- Corporate Real Estate (CRE) And Portfolio Strategy teams managing growth, consolidation, relocations, and renewals

- Finance / FP&A tracking budgets, approvals, and forecast vs. actual

- Legal managing LOIs, redlines, and compliance documentation

- Operations / Workplace / Facilities aligning space with headcount and utilization

- Executives who need a clear view of deal risk, savings, and timing

REoptimizer® is positioned for enterprise teams dealing with complexity—replacing “spreadsheets, siloed systems, and manual processes” with a single system of record.

What CRE Transaction Management Software Does

At its core, CRE transaction management software helps you:

- standardize the process (repeatable workflows and checklists)

- coordinate people and deadlines (ownership, reminders, accountability)

- organize documents (versions, approvals, audit trail)

- track costs line-by-line (so overages don’t hide in the noise)

- report in real time (so leadership isn’t waiting on a “Friday spreadsheet”)

REoptimizer® adds a key layer: it’s designed to help teams compare deal economics against comps and benchmarks and generate reporting fast with templates—because the real money is won or lost in the details.

Where It Fits (And Why It’s Not The Same As Lease Management)

A simple way to think about the lifecycle:

Before The Deal: Strategy And Site Search

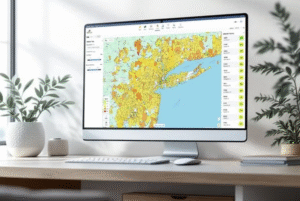

This is where teams define what they need and evaluate options. REoptimizer® supports this with KSDs (Key Site Drivers) and tools like CRESiteIQ™, built to analyze markets, compare sites, and visualize opportunities. More on in the next section…

During The Deal: The Transaction Itself

This is the heavy-lift phase: comps, negotiations, approvals, legal, due diligence, and getting to signature/close.

After The Deal: Lease Management

Lease management is what happens after execution—tracking key dates like renewals, expirations, options, and escalations. REoptimizer® content points out how missed key dates can create real cost and risk at portfolio scale.

Bottom line: lease management is “operate what you signed.” Transaction management is “control what you sign.”

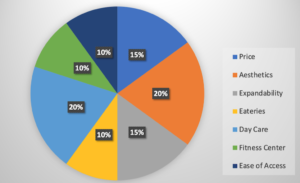

What Are KSDs?

KSDs (Key Site Drivers) are the criteria that define what “best location” means for your business—then you weight and score them so every option can be compared objectively (not emotionally, not anecdotally, and not based on whoever toured last). Consider them your highly unique KPI’s.

REoptimizer® uses KSDs to score each property in real time and calculate a final weighted score per building, instantly ranking your top contenders side-by-side.

Why KSDs Are Invaluable (And Why Teams That Use Them Win More Often)

They Turn “Opinions” Into A Repeatable Decision System. Without KSDs, site selection usually sounds like:

- “This one feels right.”

- “The price is good, but…”

- “Leadership likes that submarket.”

KSDs force alignment upfront. You define the “must-haves” and “deal-breakers” before you tour, so your team is evaluating every property against the same standard.

They Help You Compare The Stuff That’s Hard To Measure

Price and square footage are easy. The real risk is everything else:

- Workforce access and commute patterns

- Truck access and delivery windows

- Power capacity and future expansion needs

- Column spacing, dock ratios, clear height (industrial)

- Customer proximity and logistics cost impacts

- Rent vs market comps (and trend direction)

- Total Occupancy Cost (rent + CAM/NNN + taxes + insurance + utilities)

- Current utilization vs required utilization (desk sharing, peak days)

- Adjacency needs (teams that must be near each other

- Layout efficiency (loss factor, usable vs rentable SF)

REoptimizer’s® KSD approach is designed specifically to capture those “hard-to-quantify” drivers and make them scorable—so the best site isn’t just the cheapest, it’s the lowest total cost of occupancy and best operational fit.

They Save Time By Eliminating Bad-Fit Tours Early

One of the most expensive mistakes companies make is touring before they’ve defined what matters most. REoptimizer calls this out directly: teams waste time touring warehouses without clear KSDs—then end up revisiting assumptions mid-process. When KSDs are set first, you filter faster and only tour buildings that can realistically win.

They Strengthen Negotiations Because You Know Your Leverage

When you can prove (with scoring) that multiple buildings meet your needs, negotiations change:

- You’re selecting from the strongest options and negotiating from leverage.

- You can back up concession requests with evidence, using comps plus the operational requirements that drive real value.

- You reduce waste by not paying extra for features that don’t move the needle for your business.

Because Reoptimizer® scores contenders side-by-side and ranks them instantly, your team walks into negotiation with clarity: what matters, what doesn’t, and what you can walk away from.

They Keep The Portfolio Aligned With The Business (Not Just The Deal)

The biggest value of KSDs isn’t picking a building—it’s ensuring every location decision supports the business:

- growth plans

- service levels

- labor strategy

- cost targets

- utilization and waste reduction

REoptimizer’s® broader positioning is exactly this: giving teams visibility into overspending and underused space, then translating that into action through dashboards and metrics—so site decisions don’t live in a one-time spreadsheet, they become an operational advantage.

How REoptimizer® Makes KSDs Practical (Not Just A Worksheet)

Here’s the difference between “having KSDs” and using KSDs:

- Score Each Property In Real Time: As you evaluate a site, REoptimizer scores how well it delivers on each KSD—immediately, even while touring.

- Rank Overall Suitability: REoptimizer calculates a weighted score per building and instantly highlights top contenders.

- Expand Site Intelligence With CRESiteIQ™: For location strategy, CRESiteIQ™ helps define what matters and compare sites using many data points (example categories include demographics, income, fuel costs, population trends, and more).

Why Your Portfolio Needs CRE Transaction Management Software

In CRE, savings (or losses) don’t come from “being organized.” They come from making better decisions earlier and catching issues before they get locked into the deal.

Transaction management software helps you:

- Avoid missed deadlines that weaken leverage

- Prevent “death by a thousand line items” (fees, escalations, TI, concessions, operating assumptions)

- Benchmark against comps instead of negotiating blind

- Expose underutilization and waste so the portfolio improves over time

REoptimizer® specifically highlights eliminating wasted effort by centralizing data and automating alerts/workflows—so teams spend time on strategy, not chasing updates.

Why Spreadsheets Don’t Work For Transaction Management

Spreadsheets are fine for a single deal. They fail when you’re handling:

- Multiple stakeholders and approvals

- Changing versions of assumptions and documents

- Market comps, benchmarks, and reporting needs

- Utilization/waste measurement across a portfolio

That’s why REoptimizer® focuses on replacing spreadsheets and siloed tools with a centralized platform and automation.

FAQs

What Is CRE Transaction Management Software?

It’s software that manages the full commercial real estate deal process—tasks, deadlines, documents, approvals, and costs—from strategy through close, so nothing falls through the cracks.

How Is CRE Transaction Management Different From Lease Management?

Lease management is post-signature administration (key dates, escalations, compliance). Transaction management covers the whole process where the economics and terms are created.

Who Needs CRE Transaction Management Software?

Any company with a multi-location portfolio or frequent transactions—especially when deals involve finance, legal, operations, and leadership approvals.

How Does REoptimizer® Help With CRE Transaction Management?

REoptimizer® helps enterprise teams centralize portfolio data and automate reporting, alerts, and workflows—and supports site selection and deal evaluation with KSD scoring and related tools.

What Is CRESiteIQ™?

CRESiteIQ™ is a REoptimizer® tool for site selection, built to analyze markets, compare sites, and visualize opportunities in one platform.

What Are Key Site Drivers (KSDs) In Commercial Real Estate?

KSDs are your business’s weighted location criteria—used to score and compare properties objectively so you can identify the best-fit sites faster.

Why Should KSDs Be Weighted?

Because not all criteria matter equally. Weighting prevents teams from over-prioritizing “nice-to-haves” (or the loudest opinion) over the drivers that actually impact cost, operations, and performance.

How Does REoptimizer Use KSDs?

REoptimizer® scores each property against your KSDs in real time and produces a final weighted score to rank contenders side-by-side.

Learn more about REoptimizer® today.

Learn More

A Smaller, Sharper, More Selective Office Sector is Taking Shape.

For years, the office market has been cast as commercial real estate’s problem child—too much space, too few tenants, and no clear path forward. But lately, something unusual is happening: the indicators that once screamed decline are now flashing something closer to—dare we say it—stability.

Leasing activity is quietly strengthening in several major metros. Vacancy, after four years of climbing, is flattening and even edging down. And the much-mocked “extend and pretend” approach to refinancing—kicking debt maturities just far enough down the road—has bought landlords enough time for fundamentals to firm up.

But the real story isn’t just demand improving. It’s the supply side undergoing a rapid—and in some cases brutal—reset. Buildings that underperformed for years are finally being dealt with. Some are finding second lives as residential conversions. Others are meeting a bulldozer. Together, these forces are thinning out the least competitive product and reshaping what the office market actually is.

So has the office market reached a bottom? Maybe. But as always in commercial real estate, the more interesting question is why—and what this means for the tenants who occupy, evaluate, and negotiate space at scale. Let’s break down the forces driving this inflection point and how corporate occupiers should position themselves as the office sector enters a very different phase.

Office Space Leasing Has a Pulse Again

After years of “wait-and-see,” occupiers are finally doing something radical: making decisions.

According to BXP CEO Owen Thomas, the office sector likely hit bottom in 2024, a claim backed by fresh data. CBRE reports that the national office vacancy rate fell 20 bps in Q3 to 18.8%, marking the first annual decline since the pandemic began. That’s not a roar, but it is the first real sign that the market has stopped digging.

What’s Driving Recovery in the Office Market Outlook?

- Hybrid work has normalized. Companies now have data, policies, and usage patterns they trust.

- Top Tier Office Space has acted as an anchor for office space demand.

- Leasing is picking up, especially in major metros including NYC, Boston, DC, Miami, and parts of LA.

- Financial and tech firms are stepping back in, expanding in key markets.

- Decision cycles are shortening, reversing years of hesitation.

- Better-quality buildings are seeing real momentum, pulling up market averages.

This isn’t a universal rebound. It’s a selective—borderline picky—recovery. And that selectiveness is key.

“Extend and Pretend” Has Helped U.S. Office Landlords

For two years, landlords and lenders played a quiet but important game: move debt maturities into the future, avoid fire sales, and hope demand recovers in the meantime. Critics called it denial. But it helped sidestep a wave of distressed trades. The sector avoided:

- A cliff-drop in valuations for office properties

- A comp deluge dragging down even healthy buildings

- A psychological “doom loop” among investors and tenants

Landlords essentially bought themselves time—and time is precisely what they needed.

Now with leasing rising and vacancy easing, many of those “pretend” loans are looking increasingly real. You can dislike the strategy, but you can’t deny that it helped stabilize the market long enough for fundamentals to catch up.

Excess Supply is Being Culled

Demand alone didn’t turn the market. Supply tightening is doing just as much—if not more—of the heavy lifting. And the total office inventory is shrinking before our eyes.

And it’s happening through two aggressive, complementary channels.

1. Office-to-Residential Conversions Are Exploding

For decades, conversions were like unicorns: often discussed, rarely spotted. Today they’re galloping through major metros at unprecedented speed.

The numbers are dramatic:

- 2023: 1.6M SF of office-to-resi conversion starts

- 2024: 3.3M SF

- 2025 (through August): 4.1M SF

NYC historically averaged 1.2M SF per year. Now it’s running at 3.5–4x that pace. Lower Manhattan alone has:

- 5.5M SF converted since 2020

- Another 5.8M SF likely in the pipeline

This is no longer a fringe strategy. It is a structural transformation of the urban fabric. Learn more about how conversions are reshaping NYC’s market.

Why is it happening now?

- Values of obsolete offices have dropped enough for conversions to make financial sense.

- Cities—terrified of fiscal spirals—are offering tax breaks, grants, and zoning flexibility.

- Developers can buy low and rebuild into residential buildings, where demand remains strong.

As one senior CoStar economist put it:

“This is the painful but necessary repricing of office risk. The market is finding its new equilibrium—smaller, leaner, and aligned to post-pandemic work habits.”

This is not just supply removal—it’s supply removal that actually improves cities. Because older office buildings sitting empty were creating a major drain on revenue and tax values for cities.

2. Demolitions Are No Longer Unthinkable — They’re Practical

Conversions still can’t solve oversupply alone. Some buildings simply aren’t worth saving.

Owen Thomas bluntly put it:

“The office market is overbuilt. Some buildings will be demolished.”

Welcome to the new reality:If a Class B/C office building can’t be leased, can’t be converted, and can’t generate value—its land might be worth more than the structure.

Demolition has become:

- Economically rational

- Politically supported

- Market-stabilizing

BXP is participating directly in suburban teardown projects. Other REITs and private owners are following suit. Each demolition permanently tightens supply, removes underperforming comps, and makes competitive buildings look stronger.

It’s CRE’s version of a controlled burn.

The Market Is Split: Flight-to-Quality Continues

If the office market has indeed bottomed, it’s only for part of the sector.

Top-Tier Office Buildings are Dominating Leasing Activity

According to BXP:

- Rents in premier buildings are 55% higher

- Vacancy in their top-tier portfolio sits around 11%

- Demand from financial, tech, and legal tenants is rising

These are the buildings corporate tenants actually want—newer, amenitized, efficient, accessible, hybrid-friendly.

Meanwhile, Class B/C buildings are in existential limbo.

Landlords are:

- Renovating where possible

- Discounting aggressively

- Converting strategically

- And demolishing the hopeless

The divergence is so sharp that any “average market stat” conceals more than it reveals. This is really two markets operating under the same banner.

For tenants, this split creates both opportunity and risk.

What Corporate Tenants Need to Know Now

This turning point in the office market has real consequences for occupiers. In fact, many of the dynamics favor tenants—but the window is finite and narrowing in some asset classes.

If You Want Premier Space, Don’t Wait

Top-tier space is tightening fast:

- Landlords are cutting back concessions

- Rents are rising in select submarkets

- Best-in-class buildings are leasing earlier in the cycle

If your organization is considering a flight-to-quality move, the smart money says act before 2026, not after.

If You Occupy or Are Considering Class B/C, Leverage Is Still Yours

But it won’t be forever.

These landlords are offering:

- Massive TI packages

- Flexible terms

- Lease structures tailored to hybrid demand

- Below-market rents, particularly for multi-year commitments

But as the conversion pipeline grows and demolition accelerates, this abundance of choice will shrink. Bargaining power will go with it.

Market Timing Now Varies Wildly by City

Occupation strategy can no longer treat office markets as a monolith.

Cities like:

- NYC, Boston, Miami, DC → stabilizing fast

- Chicago, SF, Seattle → still working through deep supply issues

- Sunbelt markets → seeing mixed results as pandemic-era overbuilding unwinds

Portfolio optimization requires granular, metro-by-metro intelligence.

What’s Next: A Leaner, Healthier, More Polarized Office Sector

Developers like BXP are doubling down on ground-up projects—including a $2B development at 343 Madison Avenue—a signal that premier office space can still commands investor confidence.

But the broader lesson of 2024–2025 is this:

The office sector is not dying.It’s shrinking. And in shrinking, it’s strengthening.

The market is shedding obsolete space and reinforcing the buildings that work for modern corporate needs. It’s not a V-shaped recovery. It’s more like commercial real estate’s version of intermittent fasting: cut the excess, strengthen the core.

Bottom Line for C-Suites and Corporate Tenants

Has the office market hit bottom? Most signs point to yes—but selectively. The average office is still struggling.The best offices are thriving.And the worst offices are being converted, demolished, or discounted into oblivion.

For tenants, this is both an opportunity and a warning: the leverage you enjoy today will not look the same in 24–36 months. The market is rebalancing.The inventory is tightening. And the window to secure high-quality space on favorable terms is narrowing.

Strategic occupiers who move now—not later—will capture the tail end of a tenant-friendly cycle before the true recovery becomes unmistakable.

As the market shifts, the question isn’t just where you should be—but when you should move. With supply tightening and competition for top-tier space accelerating, tenants need real-time intelligence and precision, not guesswork.

That’s where REoptimizer® comes in. Our platform gives corporate occupiers the data, modeling tools, and scenario planning needed to navigate this evolving landscape—so you can lock in opportunity before the market turns.

The bottom may be here. Your advantage is knowing what comes next. Start planning with REoptimizer®.

Learn More

For much of the past two years, commercial real estate headlines have read like weather alerts: debt storm approaching, maturity wall incoming, investors brace for impact.

Yet as we close 2025, the data tells a quieter story — one that matters deeply for corporate occupiers and executives planning their next move.

Despite the turbulence, U.S. delinquency rates across commercial banks remain contained. The Federal Reserve’s most recent data points show only modest increases in commercial real estate loan delinquencies and no broad deterioration across the banking system.

That stability — paired with lenders’ discipline and the gradual thawing of transaction activity — suggests something unexpected: corporate real estate strategy can start to shift from defensive to opportunistic again.

The U.S. Delinquency Rate: What the Federal Reserve Data Shows

Let’s start with the numbers.

According to the Federal Reserve, the overall delinquency rate on all loans and leases at commercial banks stood near 1.5% in Q2 2025, down slightly from early in the year. That’s low by any historical measure.

In plain English: the U.S. banking system, and by extension its CRE exposure, is steady. Loan quality has not deteriorated in any systemic way.

That’s not because all borrowers are thriving — it’s because banks are managing risk intelligently, extending terms, and prioritizing sponsors with credible repayment or recapitalization plans.

Still, every cycle has its limits. The next question isn’t if lenders can manage risk ; it’s how long they can keep doing it. How long can you extend loans and leases before patience turns into pressure?

How Long Can You Extend Loans and Leases?

That’s the trillion-dollar question — quite literally. The CMBS market alone holds nearly $1 trillion in loans originated in the post-pandemic cycle, much of it tied to office, retail, and hospitality assets still finding their post-COVID footing. With that kind of exposure on the books, the industry has spent much of 2025 asking whether lenders are managing through the storm or merely buying time.

According to Newmark’s Jimmy Hinton, roughly $180 billion in U.S. commercial real estate loans have already matured but remain outstanding. On paper, that might look like risk postponed — a slow-motion wave of refinancing that never quite hits shore.

In practice, though, it’s far more calculated — what insiders now call “extend and defend.” Banks are extending performing loans, adjusting terms, and working with credible sponsors to stabilize assets rather than forcing them into fire-sale territory. It’s a posture born from discipline, not denial.

Here’s why it differs from the “extend and pretend” era of 2009’s financial crisis:

- Real performance data, not wishful thinking. Today’s extensions are being underwritten against hard metrics — rent rolls, DSCR, and forward leasing — rather than faith in an eventual rebound.

- Conservative leverage and real equity. The pandemic forced lenders and sponsors alike to reset expectations. Capital stacks are tighter, sponsors have more skin in the game, and lenders have clearer sightlines into collateral performance.

- Asset quality over asset quantity. This cycle’s extensions are selective. Data-center, industrial, and multifamily assets — properties with genuine demand — are being refinanced or extended. Obsolete offices? Less so.

So yes, lenders are extending — but they’re doing it to defend, not to pretend.

In short, banks are defending their balance sheets, not pretending their problems don’t exist. The Federal Reserve’s data points back that up: the delinquency rate for commercial real estate loans booked in domestic offices at commercial banks was just 1.6% at midyear — a level that would be impossible to maintain if lenders were simply hiding nonperforming assets.

Here’s what that means for occupiers and C-suite real estate leaders:

- Fewer fire sales mean less disruption in who owns or manages your properties. Continuity in ownership leads to more predictable leasing relationships.

- Longer resolution timelines create breathing room for capital expenditure and repositioning — particularly in office assets adapting to post-pandemic demand.

- Selective liquidity remains available for strong borrowers and projects, keeping credit channels open even as rates remain elevated.

Banks are buying time for fundamentals to normalize rather than writing off performing loans in a recovering market. That patience is precisely why U.S. delinquency rates across loans and leases remain steady and why commercial banks continue to serve as shock absorbers rather than amplifiers in this cycle.

This stands in sharp contrast to the market murmurs of an impending CRE crash we’ve been hearing for the last few years.

CRE Fundamentals: From Fear to Functionality

While lenders have been cautious, market fundamentals have turned a corner.

Experts are projecting double-digit growth in transaction volume for 2026, with 2025 already trending up 16–17% from last year. What’s fueling that optimism isn’t just cheaper capital, it’s operational performance.

Occupancy is improving, rental growth is reappearing in select submarkets, and capital is starting to differentiate between functional offices, resilient retail, and logistics assets rather than painting the sector with one brush.

In other words: investors aren’t buying hope, they’re buying execution.

For corporate tenants, this recovery means two things:

- Better clarity on pricing — landlords are recalibrating rent expectations based on performance, not speculation.

- Shorter decision windows — as liquidity returns, high-quality space will move faster than it has in two years.

Mortgage Delinquencies and Domestic Office Exposure

The headline risk remains office, particularly domestic offices in older urban cores.

Yes, delinquency rates for office-backed loans — particularly in CMBS — have climbed to around 8%. But remember: CMBS and bank balance sheets tell different stories. The Federal Reserve data, focused on loans booked in domestic offices at commercial banks, shows overall CRE delinquencies still below 2%.

What that tells us: distress is contained, not contagious. The stress is concentrated in legacy office assets with misaligned location, age, or floorplate efficiency — not in the broader CRE credit system.

This distinction matters for executives making footprint decisions. It means you can still find competitive terms and stable landlords in well-capitalized portfolios, even as weaker assets shake out.

Reading Between the Data Points: Timing the Cycle

Delinquency data is always a lagging indicator. But viewed alongside transaction trends, it paints a more dynamic picture.

- Loans and leases data show that credit quality remains strong enough to support renewed lending.

- Lender behavior suggests banks are willing to work with credible borrowers — a key condition for recapitalization activity to restart.

- Federal Reserve trendlines imply that Q3 and Q4 2025 could mark the floor for CRE credit softening.

That combination — resilient credit, patient capital, and stabilizing fundamentals — gives corporate tenants a rare advantage: you can plan against stability, not volatility.

If 2024 was about “wait and see,” 2026 may well be about “move and optimize.”

Credit Health, Capital Access, and What It Means for Tenants

Here’s where the data translates directly into strategy:

- Capital markets: Stable delinquency rates mean banks and life companies will re-enter lending markets sooner, widening financing options for build-to-suit, sale-leaseback, and expansion projects.

- Occupier strategy: Low delinquency rates reduce the risk of sudden ownership changes or property-level instability — a critical consideration when signing multi-year leases.

- Negotiation leverage: While office remains soft, landlords with solid credit backing and manageable debt will negotiate from strength. Knowing which side of that line your counterpart falls on can inform timing and terms.

- Long-term planning: The efficiency shift driven by AI and corporate restructuring (think Amazon and peers) is shrinking overall demand footprints — but the quality bar for the space companies do keep is rising.

That last point is worth noting: efficiency isn’t retreat — it’s reinvention. The next phase of workplace evolution will merge digital productivity with curated physical presence.

Looking Ahead: 2026 as the “Efficiency Era” for CRE

When we combine Federal Reserve delinquency data with market insights, a consistent theme emerges: discipline is paying off.

Lenders didn’t flood the market with distressed assets; they managed through.

Borrowers didn’t panic; they recapitalized strategically.

And now, investors are re-emerging with dry powder ready to deploy — cautiously, but decisively.

For corporate real estate executives, this is the phase where:

- Occupancy planning should focus on flexibility and resilience rather than contraction.

- Lease negotiations should weigh capital exposure and loan maturity profiles.

- Portfolio decisions should integrate both finncial health (credit data) and operational agility (AI-enabled efficiency).

And that’s exactly where we are: better data, clearer visibility, smarter real estate strategy.

Bottom Line: Delinquency Rates Are the Calm Beneath the Headlines

The U.S. delinquency rate is doing more than tracking late payments — it’s quietly confirming that the system is working. Credit is holding. Lenders are patient. And the commercial real estate market is recalibrating on fundamentals, not fear.

This isn’t the panic-driven cycle of the past; it’s a disciplined one — where organizations with accurate data and flexible portfolios have a measurable advantage.

For corporate real estate and finance leaders, the signal is clear:

This is not the time to retreat — it’s the time to rethink.

And that’s where REoptimizer® comes in.

Our platform helps tenants and portfolio managers use this same data-driven discipline to make smarter decisions — benchmarking rent performance, tracking lease exposure, and modeling future occupancy scenarios across locations and asset types. When the market is defined by subtle credit shifts rather than seismic shocks, having that intelligence in real time isn’t a luxury — it’s leverage.

So, as the 2026 landscape takes shape, think of REoptimizer® as your operating system for what’s next:

- Analyze your holdings against emerging credit and market data.

- Forecast renewal and relocation costs as capital markets evolve.

- Optimize your footprint for both efficiency and resilience.

The companies that thrive in the next phase of CRE won’t just follow the data — they’ll act on it.

Use the data. Use the discipline. Use REoptimizer®. Because in this market, clarity is the new advantage — and we’re built for exactly that. Learn more about how REoptimizer® gives your portfolio the edge it needs in this market.

Learn More

For years, San Francisco has been the cautionary tale of the post-pandemic city — a boomtown turned ghost town, the epicenter of what economists started calling an urban doom loop.

When the tech exodus began and downtown towers emptied out, the city’s troubles metastasized: a hollowed-out workforce, shuttered storefronts, rising visible homelessness, and viral crime headlines,

By 2023, the city that once minted the world’s most valuable startups had become shorthand for what happens when innovation meets inertia.

Office vacancy topped 30%, population loss hit 8%, and property owners watched tower valuations drop by as much as 70%. The ripple effects were brutal: less foot traffic meant less retail activity, less tax revenue meant fewer city services, and fewer city services meant — you guessed it — even fewer tenants willing to come back downtown.

But after three years of decline, the numbers are finally tilting in the other direction. The question now isn’t whether San Francisco is still in freefall. It’s whether it has reached escape velocity.

Signs of Life in a Stalled Market

For the first time in years, there are genuine signals of momentum. The city’s office market (once written off as unfixable) is showing measurable improvement.

Tenants leased more than 5 million square feet in the first half of 2025, setting the stage for San Francisco’s strongest leasing year since before the pandemic.

The second quarter alone saw 2.7 million square feet of activity, the most since late 2019 and more than 60% higher year-over-year. Year-to-date leasing is up 40% compared to 2024.

A huge share of that volume comes from a single industry: artificial intelligence.

AI: The Unexpected Hero of Downtown San Francisco

Just when it seemed the tech exodus was irreversible, a new breed of companies began moving in. Artificial intelligence firms, flush with venture capital and global attention, are now the city’s fastest-growing office tenants.

- Vercel, a web-development platform recently valued at $3.5 billion, leased 42,150 square feet at 201 Mission Street, backfilling space vacated by Indeed.

- OpenAI signed for nearly 800,000 square feet of Uber’s former offices and is reportedly hunting for another 300,000.

- Harvey AI took 92,000 square feet at 201 Third Street.

- Motive grabbed a portion of Twitter’s old headquarters in Mid-Market.

Collectively, AI companies now occupy more than 5 million square feet of office space in San Francisco. CBRE estimates that figure could exceed 21 million square feet within five years — enough to cut the city’s current 23% vacancy rate nearly in half.

This surge has had real statistical impact: sublease availability, once among the highest in the nation, has fallen 30% in two years. For the first time since 2019, the city’s overall office vacancy ticked downward.

In a market starved for good news, these moves are evidence that leasing demand, however narrow, is returning.

A Towering Vote of Confidence

Perhaps no signal is bolder than what developer Hines is planning on Beale Street. The Texas-based giant recently unveiled designs for a 1,225-foot-tall office tower on the site of PG&E’s former headquarters — a building that would surpass every structure on the West Coast and stand just 25 feet shorter than the Empire State Building.

It’s not Hines’s first attempt at remaking the skyline. A 2022 proposal for a 1,066-foot residential tower at 50 Main Street was blocked by planners adhering to the city’s 2012 Transit Center District Plan, which effectively set Salesforce Tower’s 1,070-foot height as the limit. But this time, the city’s tone is markedly different.

Mayor Daniel Lurie praised the proposal as “exactly the kind of progress our city needs,” calling it a sign that San Francisco’s comeback “depends on bold ideas and real investment.” Planning Director Sarah Dennis Phillips described the project as “an incredible vote of confidence” in downtown’s future.

Symbolism matters in commercial real estate. A skyline once defined by cranes and ambition has been stuck in stasis for half a decade. If Hines’s proposal gains traction, it won’t just add square footage — it will mark a psychological turning point.

Momentum with an Asterisk

Optimism, however, doesn’t erase math. The hole left by the pandemic is deep.

Vacancies remain above 22%, and in some submarkets — particularly South of Market and the Financial District fringe — availability still approaches 30%.

Net absorption remains uneven: the space AI firms are filling often comes from other tenants giving space back. Class B and C buildings, in particular, continue to struggle as tenants favor newer, amenity-rich environments.

Landlords are still writing large concession checks. Free rent periods of 12 to 18 months and tenant-improvement allowances exceeding $100 per square foot are not uncommon for quality space. And while leasing volume is up, capital markets are still sluggish. High interest rates have frozen many transactions and forced lenders to revalue assets at steep discounts.

In other words, San Francisco’s office recovery isn’t broad — it’s bifurcated. Trophy towers and AI-anchored buildings are gaining traction, while older inventory languishes.

Still, even selective momentum beats the negative absorption that defined 2022 and 2023. The market’s trajectory, for the first time in years, is pointing up instead of down.

A City Searching for Its Second Act

San Francisco’s real challenge may be less about leasing and more about reinvention. Remote work permanently altered the demand curve for urban office space. The city’s pre-pandemic peak (when vacancy rates hovered near 5%) is unlikely to return. Instead, the next chapter will depend on how successfully the city retools itself for hybrid work and diversified use.

That process is already visible.

Older office buildings are being evaluated for residential conversions, though high construction costs and zoning hurdles make progress slow. The city is courting life-sciences tenants, though competition from South San Francisco and the Peninsula remains fierce.

Meanwhile, the AI boom has restored some of the city’s reputation as a magnet for innovation. For local landlords, that matters. Unlike social media or fintech firms that once decamped to Austin or Miami, AI companies depend heavily on in-person collaboration, research infrastructure, and proximity to elite talent — advantages that still favor the Bay Area.

This could give San Francisco a unique edge in the next economic cycle: a concentration of high-value industries that still see physical presence as essential.

Why San Francisco’s Comeback Matters Nationally

Whether San Francisco succeeds or fails will ripple far beyond California. For institutional investors and urban policymakers alike, the city has become a stress test for the modern downtown.

If San Francisco — with its wealth, tech talent, and global brand — can’t revive its core, what hope do second-tier metros have? Conversely, if it can engineer a rebound, the playbook could inform strategies in places like Chicago, Seattle, and Portland, which face similar dynamics of remote work, urban disorder, and fiscal strain.

There’s also a psychological component. Over the past three years, San Francisco became shorthand for the “death of downtown.” A visible turnaround here would challenge that narrative, encouraging capital back into urban cores and providing political cover for other mayors to push pro-growth policies.

The city’s leadership seems aware of the stakes. Mayor Lurie’s administration is emphasizing economic recovery as civic identity, pairing business-friendly rhetoric with investments in safety, cleanliness, and infrastructure. Those steps are modest but meaningful — and they’ve been enough to draw cautious optimism from developers like Hines and investors who once wrote the city off.

The National Lens: CRE at a Crossroads

From a broader commercial real-estate perspective, San Francisco’s recovery attempts intersect with two national trends.

First, the “higher for longer” interest-rate environment has redefined valuation models across every asset class. Investors once spoiled by cheap capital are now forced to underwrite with discipline — and they’re rediscovering the value of markets that can still generate leasing momentum. If San Francisco’s fundamentals continue to stabilize, it could attract contrarian capital hunting for distress-to-recovery upside.

Second, the re-urbanization of innovation is back in focus. The same forces that once decentralized tech — remote tools, distributed teams, digital collaboration — are now bumping against productivity limits. AI development, in particular, thrives on dense networks of talent, hardware, and intellectual cross-pollination. That’s the kind of ecosystem only a handful of cities can deliver, and San Francisco is still one of them.

A Measured Hope

The comeback, then, isn’t guaranteed, but it’s plausible.

San Francisco will likely end 2025 with its best absorption in half a decade, and while vacancies remain elevated, the direction of travel is finally positive. The market is far from healed, but it’s no longer hemorrhaging.

The irony is that the same forces that nearly broke the city — technology, remote work, and inflated expectations — might also be what saves it. If AI becomes the defining economic engine of the next decade, San Francisco’s mix of talent, capital, and cultural gravity positions it to lead once again.

That doesn’t mean the doom loop has been vanquished. It means the feedback loop might finally be turning positive.

The Last Word

San Francisco’s office market may never look like it did in 2019, and that’s probably fine. The city’s value was never in square footage alone; it was in the concentration of ideas that filled those floors. If those ideas are returning even slowly the real estate will follow.

If any city can debug an urban system failure, it’s San Francisco. The only question now is whether it can keep the program running long enough to finish the reboot.

After years of whiplash, New York’s commercial real estate market has finally found its footing — but not in the way anyone expected.

Welcome to 2025, where Manhattan’s office market is roaring back to life while the city’s once white-hot industrial sector is easing off the gas.

It’s a tale of two recoveries: one fueled by confidence and competition, the other by caution and recalibration. The result? A market that’s finally learning to balance ambition with discipline — a rare mix in the city that never sleeps.

For tenants, the shift is full of opportunity — and a few warning lights. As office landlords tighten their grip on top-tier buildings, industrial users are starting to see leverage return to their side of the table. Navigating that split will be the key to winning this next phase of New York real estate.

Office Market: The Comeback No One Saw Coming

For the first time since the pandemic, Manhattan’s office leasing market is really performing.According to CoStar Analytics, 15.8 million square feet of new office space was leased in the first half of 2025 — up 14% from last year and higher than in most pre-pandemic years. That’s not just a rebound; that’s a full-on rally.

Between 2016 and 2019, new leases averaged around 15 million square feet in the first six months. Only 2018 beat that mark. To now surpass those levels after a global disruption that was supposed to “end the office”? That’s pure New York resilience and an inflection point for its real estate. The city’s office story has moved from “Will it recover?” to “How high can it go?”

Flight to Quality: Why Average Just Doesn’t Fly Anymore

If there’s a single phrase defining this recovery, it’s flight to quality — and the numbers back it up. Every one of Manhattan’s top 10 new leases in 2025 has landed in a four- or five-star building.Tenants are largely upgrading — trading tired floorplates for smarter, healthier, amenity-rich spaces that attract employees and reflect brand values.

Since early 2023, availability in New York’s trophy buildings has dropped from 17% to 10.7% — a 630-basis-point plunge. Nationwide? Trophy availability barely budged, slipping from 23.9% to 23.6%. In short, New York’s best buildings are becoming a finite resource. The city’s premier towers are commanding longer terms, stronger rents, and fewer concessions. The market’s message is clear: quality wins — but it doesn’t come cheap.

Read about JP Morgan’s new $3 billion office rebuild.

Midtown: Still the Beating Heart of the Market

Of course, where that quality lives matters just as much as what it looks like.Of the top 10 leases signed this year, seven are in Midtown Manhattan — proving that access, once again, trumps novelty.

Why Midtown? Two words: commuter convenience. With Penn Station and Grand Central funneling workers from New Jersey, Connecticut, Long Island, and Westchester directly into the core, Midtown has a logistical edge no other submarket can replicate. As hybrid work policies settle into the three-day in-office norm, proximity to transit isn’t just nice to have — it’s business-critical. It’s the difference between a packed office on a Tuesday and a ghost town.

What It All Means for Tenants

For occupiers eyeing new leases or renewals through 2026, this market demands strategy, not guesswork.

-

Start Early. Tightening availability means the best spaces don’t linger. Early engagement is the only way to secure flexibility and incentives.

-

Upgrade Smart. Many tenants are shedding underused square footage while upgrading quality. The equation has shifted from “more space” to “better space.”

-

Run the Numbers. Market spreads between Midtown, Downtown, and emerging boroughs remain wide. Tools like REoptimizer can model total occupancy cost scenarios and reveal which submarkets deliver the most value.

The key? Act with intent. The market no longer rewards hesitation — especially when Class A vacancy is trending downward and demand for premium space is intensifying.

Industrial Market: From “Full Throttle” to “Cautious Cruise”

While the office market accelerates, New York’s industrial sector is catching its breath.

After years of record-breaking construction driven by e-commerce demand and pandemic logistics, 2025 has brought a major cooldown. So far this year, just 1.8 million square feet of industrial space has broken ground — down 77% from 2024’s pace.