Most CEOs treat a commercial lease renewal like a routine administrative task—something for the legal department to “handle” or for a junior facilities manager to “check off.”

That is the single most expensive mistake you will make this decade. In today’s market, a lease renewal isn’t a paperwork exercise. It is a Strategic Arbitrage Opportunity. If you do it right, you unlock millions in pure profit. If you do it passively, you are signing a high-interest loan on space you don’t use, based on prices that no longer exist.

So, without wasting any more time, let’s explore how to treat your lease like a financial asset instead of a liability.

The Reality: You Are Negotiating in a Time Machine

The office market didn’t just “shift”—it collapsed and rebuilt itself while you were busy running your business.

Most companies are currently sitting in leases negotiated 3, 5, or 7 years ago. Those leases were built on a “Before Times” world:

-

Utilization was linear. (Everyone showed up at 9:00 AM).

-

Landlord leverage was absolute. (Vacancy was low; options were few).

-

Growth meant more desks. (If you made more money, you needed more carpet).

In 2026, all three of those assumptions are dead. The gap between your “Contracted Rent” (what you’re paying now) and “Market Reality” (what the building is actually worth) is likely wider than the Grand Canyon. If you simply “exercise your option” without a diagnostic, you are essentially tipping your landlord millions of dollars for the privilege of staying in an outdated office.

The Four Villains of the Lease Renewal

1. The Familiarity Bias (The “Paperwork” Trap)

Tenants assume staying put is “safe.”

You know the commute, you like the coffee shop downstairs, and your employees know where the bathrooms are.

In reality, familiarity is a tax. Landlords count on you resigning without proper due dilligence.

They know that moving costs money and time, so they offer you a “fair” renewal that is actually 15% above the net-effective market rate. They are charging you a “Convenience Surcharge.”

2. Blind Portfolio Economics

Most companies negotiate renewals in a vacuum.

They look at the current rent and try to knock a dollar off. But they don’t look at the Remaining NPV (Net Present Value) of the lease. They don’t see how the 3% escalations are compounding into a massive balloon payment in year eight. If you don’t know the “Total Cost of Ownership” of that location compared to your top five competitors, you aren’t negotiating—you’re begging.

3. The “Ghost Square Footage”

This is the biggest profit killer. You are paying for 50,000 square feet because that’s what you needed in 2019. But your badge-swipe data shows that on Tuesdays—your peak day—you only use 28,000. Every square foot you don’t use is Dead Capital. If you renew for the same footprint, you are essentially setting piles of cash on fire every month to heat and cool empty air.

4. The “No Alternative” Bluff

Landlords are expert poker players. If they don’t see you touring other buildings, they know they have you trapped. Leverage doesn’t come from being a “good tenant.” Leverage comes from Credible Alternatives. If you don’t have three other buildings “hot on the trail” with net-effective term sheets, the landlord has no reason to give you the concessions you actually deserve.

The “Value Stack” of a Modern Renewal

When we talk about “optimizing” a renewal, we aren’t just talking about lower rent. We are talking about the Total Value Stack. In a buyer’s market, you should be negotiating for:

-

TI Dollars (Tenant Improvement): The landlord should be paying to refresh your space, not you.

-

Abatement (Free Rent): You should get months of free rent just for signing the extension.

-

Contraction Rights: The ability to give back 20% of the space if your hybrid policy shifts.

-

OpEx Caps: Protecting yourself from the landlord’s rising insurance and tax bills.

How to Build a Finance-Grade Decision (The REoptimizer® Way)

If you want the CEO and CFO to sign off on a real estate decision, you can’t bring them “feelings” or “anecdotes.”

You need a Visual Truth Engine. This is where REoptimizer® comes in.

We didn’t build a database; we built a Leverage Machine.

1. Stop Guessing, Start Measuring

REoptimizer® centralizes your portfolio data so you can see the Remaining NPV of every lease in one click. You can instantly see which locations are “financial outliers”—the ones where you are paying 2021 prices in a 2026 world.

2. The Utilization Diagnostic

Instead of asking, “How much space do we cut?”, we ask, “How should our space actually work?” Our platform helps you map true utilization against your footprint. If you’re at 40% capacity, we model the exact “Right-Sizing” scenario that preserves your culture while slashing your OpEx.

3. Side-by-Side Scenario Modeling

This is the “Grand Slam” move. We take your current renewal terms and put them side-by-side with the top 3 relocation options in the market.

-

Option A: Renew (The “Standard” Path)

-

Option B: Restructure (The “Blend and Extend” Path)

-

Option C: Relocate (The “Maximum Leverage” Path)

We calculate the Net Effective Cost of all three, including moving costs, IT build-out, and downtime. When you show the landlord that Option C is $2 million cheaper over 10 years, the “negotiation” suddenly gets a lot shorter.

The Timeline of Leverage

If you start your renewal 6 months before your lease ends, you have already lost. You are a hostage to the clock.

To win, you must start 18 to 36 months out. * 36 Months: Start the diagnostic. What is the NPV? What is the utilization?

Time is the only thing you can’t buy back. If you have time, you have the power to walk away. If you don’t have time, the landlord owns you.

The Bottom Line: Renewals are Where Portfolios are Won or Lost

You can’t manage what you don’t measure. In 2026, “winging it” with a spreadsheet is a recipe for a $5 million mistake.You need a platform that turns your fragmented lease data into Market Power. You need to see the “Matrix” of your portfolio before you sit down at the table.

The Question: Are you going to pay the “Paperwork Tax” for another five years, or are you going to optimize your footprint for the way you actually work?

Ready to Find the “Ghost Space” in Your Portfolio?

Don’t sign another lease until you’ve seen the data. Whether you have 5 locations or 500, REoptimizer® gives you the finance-grade intelligence to make renewals your biggest win of the year.

Stop overpaying for “Dead Air.” Request a demo today to explore the leverage and cost-saving abilities REoptimizer® can have on your portfolio.

Request a Demo

Commercial Lease Renewal FAQs (The Cheat Sheet)

Q: When should I start planning? A: 18–36 months before expiration. If you’re under 12 months, you’re already losing leverage.

Q: Should I exercise my “Renewal Option”? A: Almost never as the first move. Options usually reset to “Fair Market Value,” which is subjective. Negotiate a fresh deal first; use the option as a safety net only.

Q: How do I know if I’m overpaying? A: If your rent has 3% compounded escalations and you signed before 2023, you are almost certainly overpaying.

Q: What is “Remaining Lease NPV”? A: It’s the value of your future debt in today’s dollars. It’s the only way to compare a “Stay” vs. “Go” decision with total financial clarity.

Q: Can REoptimizer® help with just one location? A: Yes, but it’s a superpower for companies with 10+ locations that need to see where the “bleeding” is happening across the entire map.

By early 2026, the real estate market has reached a critical inflection point. For institutional building owners and global corporate tenants, the conversation around office to residential conversion has matured from a speculative “doom loop” narrative into a surgical, data-driven trade. We are no longer discussing the death of the office market; we are analyzing the strategic birth of high-yield residential use from the chassis of obsolete office space.

The following points illustrate the nuance of this new conversion story:

- Beyond “Cutting Losses”: The narrative has moved past being a desperate solution to mitigate the drag of unoccupied space. It is now a proactive strategy to unlock value. As high-quality Class A+ assets find their footing, the commodity-grade older office buildings that once anchored the central business district have become “stranded assets”—properties whose utility has been outpaced by shifting market needs and strict ESG requirements.

- The “Basis Reset” as a Structural Catalyst: The current trend is not a reaction to a temporary vacancy spike; it is a permanent structural response to a fundamental valuation shift. This “Basis Reset” occurs as office investment values decline, allowing developers to acquire vacant office space at a low entry price (the “basis”). This reset is essential to offset conversion costs.

- A Shift in Management Philosophy: For the sophisticated owner, the story has shifted from merely managing occupancy to maximizing the terminal value of their portfolio. In 2026, the math is clear: if an office building can no longer compete for high-yield office space demand, its highest and best use is inevitably residential housing.

- Financial Feasibility and Yield Spreads: Institutional capital now focuses on the delta between a property’s Net Operating Income (NOI) as a struggling office versus its stabilized value as a multifamily asset. By leveraging tax incentives like NYC’s 467-m program and historic tax credits, developers are bridging the “capital stack” gap to achieve a positive Net Present Value (NPV).

The Strategic Re-Underwriting of Vacant Office Space

By early 2026, office vacancy rates have stabilized near 14% nationally, but this average masks the deep distress in central business districts. Office vacancy rates in major hubs like New York and San Francisco have hit a structural ceiling, often hovering between 20% and 30%.

However, this is not a universal failure; it is a bifurcation. While Class A+ trophy assets maintain a “flight to quality,” older office buildings and Class B/C commercial space are facing terminal economic obsolescence. The financial feasibility of converting these empty office buildings into residential units is driven by the widening delta between office NOI and surging apartment rents.

- The Basis Play: Sophisticated developers are targeting old offices where the acquisition cost is low enough to absorb conversion costs that frequently exceed $250 per square foot.

- Speed to Market: Adaptive reuse allows for residential construction that is 20% cheaper and 8–16 months faster than new construction, a critical advantage in a housing crisis where housing units are needed immediately.

Architectural Nuance: Navigating the Physical “Stranded Asset”

A large scale conversion is a surgical operation on a building’s DNA. Now, owners must move beyond the basic “floor plate” conversation to address the complex engineering required to turn a cube-farm into a luxury apartment.

Deep Core Modification & Natural Light

Most modern office buildings feature massive, deep floor plates (exceeding 100 feet in depth) that are fundamentally incompatible with living space requirements for natural light.

- Structural Voids: To meet building codes, developers are increasingly “carving out” the center of existing buildings to create light wells or atria. This reduces rentable square footage but maximizes the desirability—and the rent—of the units.

- HVAC and Air Conditioning: Transitioning from massive central chillers to individual, unitized air conditioning is one of the highest conversion costs. In 2026, the standard has shifted to high-efficiency VRF (Variable Refrigerant Flow) systems.

Sustainability and the ESG Premium

Reusing a commercial building shell is the “greenest” possible construction method.

- Embodied Carbon: Adaptive reuse saves 50–75% of the embodied carbon compared to a teardown.

- Federal Resources: The White House and federal agencies have unlocked federal resources and historic tax credits specifically for developers who can prove high-carbon savings through building conversions.

The Legislative Catalyst: 2026 Incentives and Tax Breaks

Local governments have finally pivoted from red tape to red carpet. To protect the tax base and the city’s transfer tax revenues, city leaders are aggressively subsidizing the office to residential pipeline.

The 467-m Property Tax Exemption (NYC)

The most significant policy of 2026 is NYC’s 467-m program, designed to turn obsolete buildings into affordable housing.

- The Mandate: 25% of the apartments must be affordable units (rent-restricted at 80% AMI).

- The Benefit: Developers receive a massive property tax abatement for up to 35 years, stabilizing the financial analysis of the most complex conversion projects.

National Comparisons of Conversion Policy

| City |

Primary Incentive |

Objective |

| Pittsburgh |

“By-Right” Zoning |

Bypasses zoning hearings for office conversions. |

| Los Angeles |

Adaptive Reuse Ordinance |

Targets multifamily housing in the urban core. |

| Chicago |

LaSalle Reimagined |

Grants for rent restricted units in high-vacancy zones. |

| Philadelphia |

Historic Tax Credits |

Preserves older office buildings while adding housing supply. |

Strategic Portfolio Defense: Beyond the Conversion Hype

While the headlines focus on large scale conversions, the reality for most global occupiers is a complex chess match of lease management and location strategy. As building owners seek financial feasibility for residential properties, tenants must understand how these shifts impact their specific office space demand.

The REoptimizer® Advantage: 8,000+ Data Points for Precision

REoptimizer® is the industry-standard transaction management software designed to help you play offense in a volatile market. It doesn’t just track dates; it synthesizes over 8,000 data points—from local vacancy rates to shifting building codes—to ensure your portfolio is a driver of value, not a drain on capital.

For the sophisticated corporate leader, REoptimizer® acts as a tactical defense layer:

- Local Market Benchmarking: Access real-time local vacancy rates and comparable lease data to identify exactly where you are paying over market.

- Negotiation Leverage: Armed with granular data, you can approach building owners from a position of strength, identifying opportunities for rent reductions or tenant improvement allowances based on the asset’s true market health.

- Lease Protection: Automatically flag vague or one-sided terms in your leases that could trigger unexpected costs or limit your ability to pivot as the office market bifurcates.

- Dynamic Portfolio Rightsizing: Use workplace analytics to bridge the gap between your current square feet and your actual utilization, allowing you to “shrink to grow” into higher-quality, better-located assets.

In a market where the line between commercial viability and structural obsolescence is thinner than ever, data is the only hedge against uncertainty. By transforming 8,000+ complex variables into clear, actionable intelligence, REoptimizer® ensures you aren’t just reacting to market shifts—you are anticipating them.

Stop overpaying for underutilized space and start optimizing your terminal value.

Book a Demo with REoptimizer® Today

Book a Demo

FAQ: The 2026 Conversion Landscape

What defines a viable office to residential conversion project?

Viability is dictated by floor plate depth, access to natural light, and the acquisition basis. Only about 30% of office buildings are suitable. Ideal candidates are usually older office buildings with shallower depths and high office vacancy.

How do conversion costs impact the financial feasibility of housing?

Conversion costs range from $100 to $500 per square foot. Because of these high costs, most large scale conversions require tax incentives or property tax abatements to produce affordable housing or rent restricted units while remaining solvent.

What are the main benefits of adaptive reuse over new construction?

Adaptive reuse is faster (saving up to 16 months) and more sustainable, as it rehabilitates an existing building. It also avoids the high cost of new foundations and site prep, making it a powerful tool to address the housing shortage.

How do local governments facilitate building conversions?

Local governments use “by-right” zoning, tax breaks, and historic tax credits to reduce the regulatory hurdles for building owners. These policies are designed to revitalize the central business district and increase the housing supply.

In the current labor market, a quiet but profound shift is taking place. While “restructuring” and “streamlining” are the headlines, the complete reality is a structural technological disruption driven by artificial intelligence. This isn’t just about productivity gains; it’s a fundamental change in how companies calculate their need for human capital and, by extension, office space.

Recent data from 2025 and early 2026 shows that artificial intelligence loss of jobs is no longer a theoretical risk—it is a measurable trend. Tech giants and financial institutions are trading human headcount for AI infrastructure, leading to a new economic formula: fewer employees, more AI models, and significantly smaller office footprints.

Recent College Graduates and the “First Kill Zone”

The AI revolution is not affecting all workers equally. Recent labor statistics show a “white-collar bloodbath” concentrated among recent college graduates and early-career workers. Research indicates that junior positions are shrinking at businesses integrating AI automation. This technological change hits the “First Kill Zone” hardest: roles defined by repetitive tasks and structured workflows that once served as the “bottom rungs” of the career ladder.

“We are seeing the ‘hollowing out’ of the entry-level tier. Companies are no longer hiring five juniors to find one star; they are hiring one star equipped with an AI agent.” — Sector Analysis, 2025 Global Workforce Report.

Software Development: Smaller Teams, Fewer Desks

The classic model of massive engineering departments occupying multiple floors is dissolving. Software development is seeing significant job displacement as AI agents move from simple code completion to full-scale architecture.

- Efficiency Gains: Tools like GitHub Copilot and Amazon CodeWhisperer allow a single developer to do the work that previously required a small team.

- Space Impact: Projects that once justified 50-person “bullpens” are now being handled by 10-person specialist pods, leading to immediate office contraction.

- Junior Hiring: Many firms are reducing their intake of entry-level developers, preferring a lean team of senior staff who can audit AI-generated code.

Legal and Compliance: The End of the Associate Army

In the legal sector, the “army of junior associates” once required for document review and research is being replaced by sophisticated AI platforms.

- Research Speed: AI models like Harvey can parse thousands of NDAs and case files in seconds, a task that used to take weeks of human labor.

- Headcount Reduction: When one platform does the work of 20 junior associates, the need for large Manhattan or D.C. office suites disappears.

- Lease Risks: Law firms often hold long-term, expensive leases; AI is making the square footage per partner metric look increasingly bloated.

Bank Tellers and Finance: The Automation of Logic

Bank tellers and routine accounting staff are facing a new wave of job losses as structured data meets automated logic.

- Reconciliation: AI now handles account balancing, anomaly detection, and routine reporting before a human even logs in.

- Branch Closures: The shift toward digital-only interactions has rendered traditional bank branches and regional finance hubs obsolete.

- Departmental Shrinkage: Finance departments that once required 100 people are right-sizing to 30-40 specialists, leaving vast amounts of “shadow vacancy” in their office portfolios.

The World Economic Forum predicts that by 2030, over 200,000 U.S. accounting jobs will vanish due to AI-driven reconciliation.

Customer Support: The Death of the 500-Seat Floorplate

Customer support centers were once a primary driver of suburban office demand. Today, they are the primary example of the job market being reshaped by AI agents. Klarna revealed its AI assistant performed the work of 700 full-time agents, handling two-thirds of customer service chats in its first month.

- Tier 1 Resolution: AI chatbots and voice agents now resolve up to 95% of routine queries, including refunds and scheduling.

- Footprint Collapse: Companies no longer need massive call centers with break rooms and parking lots when the majority of the “workforce” exists on a server.

- Outsourcing Shifts: Even offshore BPO hubs are seeing a decline in demand as companies bring support back in-house via localized AI models.

Job Displacement and the Commercial Real Estate Disruption

The potential for widespread displacement has a direct, evolving impact on commercial real estate (CRE). For decades, employers leased space based on headcount. Today, AI adoption means a firm can double its output while eliminating half of its physical desks.

- Shrinking Floorplates: Companies like Amazon and UPS have confirmed thousands of layoffs as they shift capital toward AI products. The demand is moving from “seats for people” to “racks for servers.”

- The Rise of the “Jewel Box” Office: Organizations are exiting massive, automated back-office cubicle farms in favor of smaller, high-quality “collaboration hubs.”

- Early Signs of Distress: Class B and C assets in cities that once relied on healthcare admin and insurance support are seeing record-high vacancies as those jobs lost to automation do not return.

Amazon recently confirmed an additional 14,000 layoffs as it shifts over $100 billion in capital expenditures toward AI products and logistics tech.

Artificial Intelligence: Navigating the New Job Market

As technological innovation creates new occupations in AI oversight, it simultaneously renders legacy employment models obsolete. To avoid being locked into a firm’s past, occupiers must treat their future real estate as an elastic asset. In the current job market, the square footage requirements of 2026 are fundamentally different from those of 2020.

- Renegotiate on Reality: Use recent data on your AI-driven headcount projections to right-size now.

- Focus on Flexibility: Shift to 3-5 year terms. In an economy where a single department can be automated overnight, a 10-year lease is a significant risk.

- Audit the “Kill Zones”: Identify which departments are seeing the highest risk of displacement and reduce those specific square footages first.

How REoptimizer® Keeps You Ahead

The AI revolution moves faster than typical cyclical downturns. To stay competitive, you need more than just general labor statistics—you need a process to identify excess space before it becomes a liability.

REoptimizer® provides the real-time intelligence needed to model workforce changes and negotiate from a position of strength. Don’t let your portfolio be defined by job losses; define it by the productivity gains of a leaner, smarter organization.

Book a demo today to see how AI and REoptimizer® can revolutionize your portfolio.

Book a Demo

Commercial real estate has officially entered a “sorting year.” Lenders are no longer just looking at property types; they are conducting “ruthless” forensic audits on Debt Service Coverage Ratios (DSCR), sponsorship liquidity, and Capex runways.

For corporate tenants with massive office and warehouse footprints, this financial pressure on landlords translates directly into operational risk. From “jingle mail” ownership transfers to the sudden evaporation of Tenant Improvement (TI) allowances, the stability of your lease is now tied to the “financeability” of your landlord’s asset.

The 2026 CRE Underwriting Outlook

For the last decade, corporate real estate (CRE) was a game of location and scale. In 2026, the game has changed to intelligence and liquidity.

As a corporate tenant managing a diverse portfolio of high-stakes office space and mission-critical warehouse hubs, you are about to feel the ripple effects of a lending market that has gone from “wait-and-see” to “search-and-destroy.”

Trepp’s research team calls it a “sorting year”—a period where the line between a stable asset and a distressed one is drawn with a red pen.

Here is the data-driven reality of how 2026’s ruthless underwriting will impact your bottom line—and why your transaction management strategy needs an immediate upgrade.

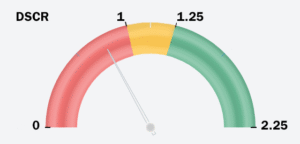

1. The DSCR Death Spiral: Why Your Rent Isn’t Enough Anymore

In 2021, a 1.25x DSCR was the gold standard. In 2026, lenders are recalibrating for a “higher-for-longer” rate environment. Lenders are now stress-testing assets against flatter or even negative rent growth.

-

The Impact on You: If your landlord’s loan is coming due and they can’t clear the new, higher DSCR bar, they are in “triage.”

-

The Risk: A landlord in triage mode will cut every “non-essential” expense. This means the lobby renovations stop, security shifts are reduced, and the HVAC system you complained about six months ago will continue to fail.

-

The Office/Warehouse Divide: While industrial assets generally have stronger cash flow, the “ruthless” underwriting of 2026 is hitting older distribution centers hard, forcing landlords to choose between paying the mortgage or upgrading your loading docks.

2. The “Capex Runway” Test: Is Your TI Allowance Real?

Lenders are now probing Capex runways with unprecedented scrutiny. They want to know if the money for “story” assets—those value-add warehouses or “reimagined” office spaces—is actually in the bank or just a line item in a pitch deck.

-

The “Haves” vs. the “Have-Nots”: Institutional sponsors with deep pockets are being welcomed by lenders. Small-to-mid-cap landlords are being told to “re-up” or “walk.”

-

The Tenant Trap: If you are negotiating a renewal that includes a significant Tenant Improvement (TI) allowance, beware. A landlord who cannot pass the 2026 underwriting test may sign your lease today but lack the liquidity to pay your contractors tomorrow.

3. The “Jingle Mail” Resurgence and Ownership Volatility

“Jingle mail”—the practice of a landlord mailing the keys back to the lender—is no longer a ghost story; it’s a 2026 strategy. With a “maturity wall” of loans hitting the market, many owners are opting for deed-in-lieu transfers.

A foreclosing lender could technically terminate your lease in certain jurisdictions if you are paying below-market rent.For a corporate tenant, a building’s financial distress is a direct threat to your business continuity. Use the following checklist to evaluate your current exposure:

The 2026 Corporate Portfolio Risk Checklist

When lenders apply 2026’s heightened DSCR and Capex Runway tests, they triage properties into winners and losers. As a tenant with millions in lease obligations, you must monitor these three critical factors:

-

Ownership Volatility (The Lender Takeover):

-

Office Portfolio Impact: High risk of “accidental landlords”—banks or special servicers who lack the incentive to provide a high-quality tenant experience. You may face delayed responses to lease inquiries and a lack of long-term vision for the asset.

-

Warehouse/Industrial Impact: A lower risk of total abandonment, but often leads to “loan-to-own” private equity takeovers. New owners may look for technical lease defaults or hike “pass-through” expenses to maximize short-term yield.

-

The Maintenance Deficit (Cost-Cutting as Survival):

-

Office Portfolio Impact: Visible degradation such as slower elevators, dated common areas, and cooling issues. This makes “return-to-office” (RTO) mandates nearly impossible to enforce for your staff.

-

Warehouse/Industrial Impact: Manifests as deferred structural maintenance. Neglecting roof repairs or parking lot integrity can lead to localized flooding or equipment damage, impacting your supply chain.

-

Expansion Constraints (The Capital Lockdown):

-

Office Portfolio Impact: Landlords may be fundamentally unable to fund build-outs for new floors. Even with a signed expansion option, the lack of liquidity can leave you with a half-finished shell.

-

Warehouse/Industrial Impact: A severe lack of capital for infrastructure upgrades. If you need more power for automation or cold-storage conversions, a landlord struggling to refinance will likely deny the request or demand you fund 100% of the cost.

Critical Strategy Note: In an era of ownership volatility, the SNDA (Subordination, Non-Disturbance, and Attornment) agreement is your most important legal shield. Without it, a foreclosing lender could technically terminate your lease in certain jurisdictions if you are paying below-market rent.

Learn More

The U.S. commercial real estate market is not behaving uniformly — and that matters for enterprise real estate strategy. Let’s look at the market from a bird’s eye view.

Five data-backed realities are shaping tenant leverage heading into 2026:

- Pricing divergence is driven by liquidity and asset quality, not geography

- New supply is collapsing faster than demand is recovering

- Net absorption remains negative at the macro level

- Lower interest rates are increasing transaction velocity — not equalizing leverage

- Negotiating power is now asset-specific, not market-wide

For Fortune 1000 occupiers, this environment rewards precision, speed, and portfolio-level visibility — not broad market assumptions.

So let’s dive into these trends and discuss how to keep your portfolio nimble an well-performing in this environment.

The CRE Market Isn’t Splitting — It’s Sorting

Most commentary describes today’s commercial real estate environment as a “two-tier market.” That framing suggests a simple divide between winners and losers. The data tells a different story.

What’s happening instead is a sorting of assets and owners based on constraint — specifically, who can afford to wait and who cannot.

This sorting is driven by three measurable factors:

- Access to capital: Well-capitalized owners can refinance, carry vacancy, and delay leasing decisions. Less-capitalized owners often must trade rent, concessions, or term flexibility to secure occupancy.

- Ability to hold through uncertainty: Owners with longer investment horizons can withstand slower leasing velocity and evolving space utilization. Others are forced to reprice assets in real time.

- Flexibility to reposition assets: Buildings that can be upgraded, re-tenanted, or adapted to shifting tenant needs are retaining value. Assets without repositioning options are absorbing the bulk of pricing pressure.

As a result, pricing is adjusting selectively, not uniformly.

The market is clearing quietly — through deal terms, concessions, and asset-level repricing — rather than through broad distress or forced sales.

Pricing: Two Indexes, Two Operating Realities

If we look at CoStar’s Commercial Repeat Sale Indices (CCRSI), we can observe two distinct pricing behaviors occurring at the same time.

Premium / Core Assets (Value-Weighted Index):

- +0.4% month over month (November)

- Six consecutive monthly gains

- +1.1% quarter over quarter

- −1.3% year over year

This index is driven by larger, higher-value transactions, typically involving institutionally owned assets in liquid markets.

Smaller / Secondary Assets (Equal-Weighted Index):

- −0.9% month over month

- −0.7% quarter over quarter

- Flat year over year

This index reflects the more numerous, lower-priced transactions that dominate secondary and tertiary properties.

Why These Two Indexes Matter To Corporate Tenants

This divergence is not simply “major markets outperforming secondary markets.” It reflects who still has pricing power — and why.

- Assets with institutional liquidity and long-term relevance are being priced on their ability to withstand uncertainty, not on near-term occupancy alone.

- Assets without capital buffers are being repriced to clear — often quietly — through lower transaction values and more flexible leasing terms.

For corporate occupiers, the practical implication is clear: lease economics now vary sharply by building, even within the same submarket.

Market averages increasingly obscure:

- Where landlords are willing to concede

- Where pricing discipline is holding

- Where renewal leverage actually exists

Supply: The Construction Cliff Is A 2026–2028 Problem

Today’s availability reflects yesterday’s development decisions. The construction data now coming into focus shows that far fewer projects are replacing the space currently delivering — setting up a materially different supply environment in 2026–2028.

Key Construction Data:

- Total completions across office, retail, and industrial: 3M SF in 2025

- Down 34.2% year over year

- Q4 new property openings fell below 100M SF, the lowest level since 2013

This decline reflects a sharp reduction in projects entering and advancing through the development pipeline — not a temporary delay.

Why The Impact Is Delayed For Corporate Tenants

Current leasing conditions still benefit from:

- Projects approved prior to rate hikes

- Developments already under construction reaching completion

These deliveries create the impression of adequate supply today.

The constraint emerges later, when:

- Fewer new projects replace delivered space

- The pool of modern, functional buildings shrinks

- Tenants compete for the same subset of “approved” assets

As a result:

- Premium space tightens even if headline vacancy remains elevated

- Choice narrows faster than market statistics suggest

- Negotiating leverage shifts unevenly across buildings

This pattern is already evident in newer Class A office properties and select industrial corridors, where availability has tightened despite broader market softness.

Demand: Net-Negative Doesn’t Mean Evenly Weak

Macro Demand Snapshot

- U.S. commercial nonresidential space is projected to lose ~100M SF of net tenants in 2025

- This is the most negative absorption since 2009

The Important Nuance

Demand is not disappearing uniformly — it is rotating:

- Enterprises are consolidating footprints

- Tenants are upgrading into higher-quality assets

- Commodity space is bearing the brunt of vacancy

Recent data shows improving absorption in prime office assets, even while the broader market remains soft.

Translation: Your leverage depends on where you are moving — not just whether you are moving.

Interest Rates: Easier Capital, Uneven Impact

What Changed In 2025

- The Federal Reserve cut rates three times since September

- Target range dropped to 3.50%–3.75% by December

- Borrowing costs are now at their lowest level since 2022

What Didn’t Change

Lower rates:

- Increase transaction activity

- Improve refinancing options for strong owners

- Support pricing for premium assets

They do not:

- Force well-capitalized landlords to concede aggressively

- Restore leverage uniformly across all buildings

- Eliminate distress in secondary assets

Rate cuts increased movement — not symmetry.

What This Means For Corporate Tenants

1. Leverage Is Now Asset-Specific

The idea of a universally “tenant-friendly market” no longer holds.

Negotiating strength depends on:

- The owner’s capital position

- The asset’s long-term relevance

- How critical your tenancy is to the landlord’s strategy

2. Secondary Assets Offer Tactical Opportunity

Buildings facing:

- Refinancing pressure

- Tenant concentration risk

- Limited repositioning options

are often more willing to:

- Trade rent for occupancy

- Extend TI packages

- Reset economics at renewal

These opportunities require visibility and speed.

3. Supply Constraints Will Show Up Later — Not Now

The sharp drop in construction today increases the odds of:

- Fewer high-quality options in 2026–2028

- Less choice for ESG-, talent-, or logistics-driven requirements

- More competition for newer assets

Planning ahead matters more than reacting later.

Why Transaction Management Has Become A Strategic Control Point

The current commercial real estate environment is not just fragmented — it is asymmetric.

Pricing, supply, and leverage now vary by building, by owner, and by timing. In this kind of market, outcomes are no longer driven by where you operate, but by how quickly and consistently decisions move from insight to execution.

For large occupiers, the real risk is not misreading the market, but allowing sound strategy to erode through slow, inconsistent execution.

-

Concessions negotiated but not captured

-

Approvals delayed while leverage shifts

-

Inconsistent deal terms across similar assets

-

Portfolio decisions made on incomplete or outdated data

This is where transaction management moves from administrative support to strategic infrastructure.

What REoptimizer® Enables In Practice

REoptimizer® gives corporate real estate teams a single operational system to manage complexity at scale:

-

Asset-Level Intelligence At Portfolio Scale

Centralizes deal data across regions, asset types, and brokers so negotiations reflect real-time leverage — not market averages.

-

Disciplined, Defensible Decision-Making

Standardizes underwriting assumptions, approval workflows, and deal inputs to reduce variability and governance risk.

-

Faster Conversion Of Leverage Into Economics

Shortens LOI-to-close timelines so negotiated advantages are not lost to delay, shifting conditions, or internal friction.

-

Consistent Economics Across The Portfolio

Enables side-by-side comparison of concessions, terms, and obligations so value is captured systematically — not deal by deal.

-

Post-Signature Accountability

Ensures negotiated terms survive execution and are visible beyond the transaction, reducing leakage over the lease lifecycle.

In a market where leverage changes asset by asset, execution discipline becomes a source of leverage itself.

The Bottom Line For Enterprise Occupiers

The defining feature of today’s commercial real estate market is not volatility. It is selectivity.

Capital, supply, and demand are no longer moving together — and neither is negotiating power.

For Fortune 1000 tenants, winning in this environment requires:

-

Asset-level insight, not market generalizations

-

Portfolio-wide visibility, not regional silos

-

Faster, more disciplined execution, not reactive deal-making

Organizations that adapt their operating model — not just their strategy — will secure flexibility, control risk, and preserve value as the market continues to sort. REoptimizer® is your tool to see your entire portfolio strategically in the midst of this environment. Learn more about how it can level up your commercial real estate in 2026 and beyond.

Learn More

Frequently Asked Questions

Is 2026 A Tenant Market Or A Landlord Market?

Neither, broadly speaking. Data shows leverage is asset-specific, with premium properties firming and secondary assets repricing downward.

Why Are Premium Assets Rising If Demand Is Weak?

Capital is prioritizing assets that can absorb uncertainty and remain liquid. At the same time, tenants are rotating into higher-quality space even as total footprints shrink.

How Does Reduced Construction Affect Corporate Tenants?

Lower deliveries today increase the risk of future scarcity in high-quality space, especially for tenants with modern, ESG, or operational requirements.

Triple net (NNN) leases are a go-to structure across commercial real estate, especially for industrial and flex properties. On paper, they’re simple:

Base rent + taxes + insurance + maintenance (CAM/OPEX).

Landlords like the steady return. Tenants like the transparency and control.

But here’s the catch: NNN leases aren’t fixed-cost. They’re variable-cost agreements tied to expense categories that can swing sharply—especially as buildings age. Over time, that volatility can:

If your portfolio includes mixed-age facilities, age-driven OPEX risk may be a bigger financial story than rent. Let’s discuss.

The Built-In Exposure of Triple Net Leases

In a true triple net structure, tenants typically carry most operating expense responsibility beyond base rent, including:

-

Property Taxes: reassessments, mill rate changes, local incentives, shifting valuations

-

Insurance: market cycles, regional risk, asset condition, claims history

-

Maintenance & Repairs (CAM/OPEX): the largest—and least predictable—driver

Think of these as moving variables, not line items. They flex with market conditions, landlord behavior, and building performance. And they rarely move in a straight line.

Why Industrial Tenants Feel It First (and Worst)

Industrial users often see the most immediate impact because so many costs are passed through—and because maintenance decisions are frequently tenant-managed. That means OPEX shifts with:

-

System performance (HVAC, roof, paving, dock equipment)

-

Vendor pricing and availability

-

Seasonality and operational intensity

-

Deferred capital conditions inherited at move-in

A quick reality check:

Across a multi-site network, that spread can translate into six figures of unplanned spend annually.

Building Age Isn’t a Detail—It’s a Cost Multiplier

Under NNN terms, age becomes a direct financial variable. Older properties usually bring:

-

Higher repair frequency

-

Less efficient mechanical systems

-

End-of-life components (roof, RTUs, electrical, paving)

-

Higher emergency maintenance risk

Deferred Maintenance: The “Rent Discount” Trap

In older assets, landlords may delay major capital replacements knowing an NNN tenant absorbs the operating burden. A “competitive” rent rate can hide upcoming expense spikes that show up in year 2, 4, or 7—right when you’re trying to stabilize operations.

Energy and System Inefficiency Adds Up Fast

Older industrial buildings often lack modern efficiency standards—HVAC performance, insulation, lighting, controls. If you’re paying utilities directly (common in NNN), inefficiency becomes a recurring tax that compounds over the full term.

Maintenance Escalation Isn’t Linear

Maintenance doesn’t rise gradually—it often jumps once major systems hit the 15–20 year range. If the roof, mechanical, or electrical systems are near that threshold, your cost curve can steepen mid-term—not at renewal.

Bottom line: a low base rent can mask a high effective rent once age-adjusted OPEX is included.

Model Total Cost of Occupancy (TCO), Not Just Rent

The more durable approach is Total Cost of Occupancy (TCO) modeling across the lease term—rent plus projected OPEX and capital exposure.

Evaluate Life-Cycle Cost, Not Just Lease Cost

Run scenarios that incorporate:

-

Age-based maintenance trajectories (roof, HVAC, lighting, paving)

-

Historical tax reassessment patterns

-

Insurance volatility (especially for older or high-value assets)

Even conservative assumptions will quickly reveal where “cheap rent” becomes high all-in occupancy cost.

Negotiation Moves That Actually Reduce Risk

Tie Tenant Improvements to Asset Condition

If the building needs modernization—mechanical upgrades, lighting retrofits, dock equipment—push for landlord participation. Improvements with residual life beyond your lease term often increase property value, which makes them easier for landlords to justify.

Define Maintenance vs. Capital Replacement—In Writing

This is non-negotiable in older facilities. Lease language must clearly separate:

The difference determines whether a failure becomes a manageable repair—or a major unbudgeted capital hit.

Require OPEX Transparency and Audit Rights

Add provisions for:

-

Detailed CAM/OPEX statements

-

Standardized backup documentation

-

Audit rights and dispute windows

For multi-site occupiers, centralized audits across the portfolio can uncover recurring discrepancies and recover overcharges.

Control vs. Responsibility: The Hidden Trade-Off in NNN

NNN leasing promises visibility and operational control—but across dozens (or hundreds) of sites, that control becomes complexity.

What you gain

-

Cost management through bidding, preventative maintenance, and efficiency upgrades

-

Operational alignment with your temperature, security, and logistics needs

-

Line-item transparency

What you inherit

-

Cost volatility in taxes, insurance, and repairs

-

Administrative burden across vendors, invoices, audits, and site conditions

-

Age amplification: older assets = less predictability

This is where many portfolios get surprised: control doesn’t guarantee predictability.

Turn NNN Exposure Into an Advantage With Operational Discipline

NNN shifts risk to the tenant—but disciplined operators can turn that into cost leadership through structured portfolio management:

-

Preventive maintenance optimization: extend system life and reduce emergency repairs

-

Energy retrofits: lighting and controls upgrades can meaningfully lower utility spend

-

Portfolio-level insights: recurring inefficiencies and overcharges become visible only when data is centralized

Without integrated data, most tenants never see the full trendline—they just keep paying the bills.

The Strategic Shift: From Lease Thinking to Lifecycle Thinking

Triple net leases make one thing clear: you’re not just leasing space—you’re operating an asset. That means performance depends as much on physical condition and operating discipline as on the lease terms.

Sophisticated occupiers are shifting toward lifecycle-based governance, evaluating sites by:

-

Age and deferred maintenance exposure

-

Energy intensity and upgrade potential

-

OPEX volatility mapping

-

Renewal vs. relocation equivalency

That’s where platforms like REoptimizer® become essential—turning occupancy cost into a measurable, optimizable variable.

The Bottom Line

Triple net leases reward diligence and punish complacency. They offer transparency—but they also transfer volatility and aging-asset risk downstream.

In today’s environment of rising maintenance costs, insurance swings, and aging industrial stock, lease structure is strategy.

If you manage a large, mixed-age portfolio, don’t just negotiate rent. Model lifecycle exposure, track OPEX trends, and quantify the real cost of building age.

Because in a triple net world, the number on the lease is only half the story.

Model the real cost of occupancy. Optimize with REoptimizer®. See what REoptimizer® can unlock across your portfolio. Learn More

Learn More

FAQs: Triple Net Leases, Building Age, and OPEX Volatility

What is a triple net (NNN) lease?

A triple net lease is a commercial lease structure where the tenant pays base rent plus operating expenses, typically including property taxes, insurance, and maintenance/CAM. It’s common in industrial, flex, retail, and single-tenant assets.

What does “OPEX” mean in commercial real estate?

OPEX (operating expenses) refers to the ongoing costs to operate a property, such as maintenance, repairs, common area maintenance (CAM), utilities (often), property management, and other pass-through charges, depending on lease language.

Why can OPEX matter more than rent in an NNN lease?

Because rent is usually fixed or escalates predictably, while taxes, insurance, and maintenance can fluctuate significantly. Over time, OPEX volatility can raise your effective occupancy cost enough to outweigh a “good” rent rate.

How does building age increase NNN lease risk?

Older buildings typically have:

-

More frequent repairs

-

Less efficient systems (HVAC, lighting, insulation)

-

Components closer to end of life (roof, paving, electrical)

This results in higher maintenance spend and a greater likelihood of mid-term cost spikes, not just renewal-driven increases.

What is CAM, and how is it different from OPEX?

CAM (common area maintenance) usually refers to shared-area costs in multi-tenant properties, including:

-

Parking lots

-

Landscaping

-

Snow removal

-

Exterior lighting

OPEX is broader and may include CAM plus other operating costs, depending on how the lease defines pass-through expenses.

What are the biggest hidden cost drivers in an NNN lease?

Most surprises come from:

-

Tax reassessments and mill rate changes

-

Insurance premium increases driven by market shifts, risk exposure, or asset condition

-

Maintenance and repair escalation, especially in older assets

-

Unclear responsibility for capital replacement versus routine maintenance

What’s the difference between maintenance and capital replacement?

-

Maintenance: routine service and repairs that keep systems operating, such as filters, minor fixes, and patchwork

-

Capital replacement: replacing major components like roofs, HVAC units, paving, or structural systems

Lease language should clearly define responsibility, as this distinction often determines whether costs remain manageable or escalate rapidly.

Can a landlord push capital costs to a tenant in an NNN lease?

If the lease is vague, yes—especially in older properties. Clear definitions separating repair from replacement and operating costs from capital costs are critical to limiting exposure.

How do I evaluate the real cost of an NNN lease?

Use total cost of occupancy (TCO) modeling across the lease term, including:

-

Base rent

-

Property taxes and reassessment trends

-

Insurance volatility assumptions

-

Age-based maintenance curves

-

Energy and utility impacts if utilities are tenant-paid

What should I request before signing an NNN lease?

Ask for:

-

Three or more years of CAM and OPEX history with line-item detail

-

Recent property tax bills and assessment history

-

Insurance claims history and current premiums

-

Roof and HVAC age, service records, and estimated remaining life

-

Vendor contracts tied to pass-through charges

What lease clauses reduce OPEX volatility?

Common protections include:

-

Detailed CAM statement requirements

-

Audit rights and dispute windows

-

Exclusions for landlord overhead or undefined administrative fees

-

Clear capital replacement responsibility and amortization rules

-

Spending approval thresholds for major repairs

Are NNN leases always a bad deal for tenants?

No. NNN leases can be advantageous for tenants with strong operational discipline because they allow:

-

Competitive vendor bidding

-

Preventive maintenance optimization

-

Energy efficiency and retrofit strategies

Without portfolio-level visibility, however, the cost volatility remains with the tenant.

How can tenants reduce OPEX in older industrial buildings?

High-impact strategies include:

-

Preventive maintenance scheduling, especially for HVAC and roof systems

-

LED lighting and controls retrofits

-

Sealing and insulation improvements

-

Vendor consolidation and standardized scopes of work

-

Portfolio-wide CAM and OPEX audits

What’s the simplest red flag that an older NNN building will get expensive?

A combination of:

-

Below-market base rent

-

Limited building documentation

-

Aging roof and HVAC systems near end of life

-

Vague lease language around maintenance and capital replacement

How does REoptimizer® help with NNN lease management?

REoptimizer® helps occupiers turn occupancy cost into structured intelligence by enabling:

-

Portfolio-wide OPEX trend tracking

-

Anomaly detection and audit readiness

-

Lifecycle exposure modeling tied to asset age

-

Data-driven renewal versus relocation decisions

Rent escalations aren’t inherently “bad.” They’re a normal part of commercial leasing meant to protect a landlord’s revenue over time. The real risk is how the escalation is structured—and how easily the language can shift volatility, compounding, and index-selection power onto the tenant.

This is why escalation clauses are one of the most common “quiet cost drivers” in a lease: the numbers often look acceptable in Year 1, but the clause can create an outsized impact by Year 7, 10, or 15. Let’s talk about how to avoid this.

What Is A Rent Escalation Clause?

A rent escalation clause defines how rent increases over the lease term, including timing (annual, every other year, at specific milestones) and the method used (index-based, fixed, hybrid, or bumps). The nuance most teams miss is that escalations are typically compounding: each increase builds on the last year’s rent, not the original base. That compounding effect is where “small” differences in language become meaningful portfolio-level budget outcomes.

Two subtle points that matter in negotiations:

-

Escalation method interacts with term length. A clause that seems tolerable in a 5-year deal can become a serious exposure in a 12–15 year deal.

-

Escalation language often includes embedded leverage. Index selection, floor/ceiling language, notice timing, and calculation method can all tilt results—without changing the headline escalation “type.”

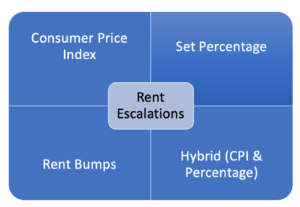

The Four Basic Types Of Rent Escalations

1. CPI Or Inflation-Based Escalations

CPI-based escalations are often presented as “fair”—rent only rises with inflation. But the practical reality is that CPI clauses can be one-sided risk transfer if they don’t include guardrails.

Where CPI gets dangerous (the nuance):

-

Index selection isn’t neutral. Landlords may specify a CPI measure or geography that best supports higher increases. Even small differences in index definition can create materially different outcomes over time.

-

CPI clauses can have “silent” floors. Some CPI clauses include a minimum increase (a floor) even when CPI is low, but still allow full upside when CPI is high. That’s not “inflation protection”—that’s asymmetry.

-

Timing matters more than most people think. CPI is usually measured over a period (e.g., year-over-year). If the clause uses a measurement window that catches an inflation spike, that spike can become embedded in the rent base going forward.

-

Compounding locks in the pain. Even if inflation cools later, the higher rent established during the spike becomes the new baseline for future increases.

How REoptimizer® helps (subtle but powerful):

-

Flags CPI escalation language and the fine print (index, geography, lookback window, floor/ceiling language)

-

Converts the clause into a plain-English summary: “Your rent increases by X, measured by Y, calculated on Z schedule, with limits of A/B”

-

Models multiple inflation scenarios so you can see how “reasonable” becomes “runaway” across the term, especially in longer leases

Negotiation angle that often works:

If CPI is on the table, push for caps and clarity (and avoid floors that create upside-only outcomes). When landlords insist on CPI, the win is often in the guardrails—not in eliminating CPI entirely.

2. Fixed Percentage Escalations

Fixed escalations are typically the most tenant-friendly option because they turn uncertainty into a schedule. But “fixed” doesn’t automatically mean “optimized”—the details still matter.

The nuance in fixed escalations:

-

Fixed is predictable, not always cheap. A fixed 3% may be a win versus CPI during high inflation—but in low-inflation periods it can cost more than what CPI would have done. The key is whether the predictability premium is worth it for your organization.

-

The compounding effect is still real. A fixed increase compounds too, so the difference between 2.5% and 3% is not linear over 10+ years.

-

Fixed escalations can hide in base rent resets. Some leases combine a fixed escalation with periodic “reset to market” language or appraisal mechanisms that function like a second escalation.

-

Fixed increases interact with concessions. A landlord may trade a slightly lower fixed escalation for changes elsewhere (free rent, TI, abatement language, operating expense treatment). The “best deal” is often the one with the best total economics, not the lowest escalation percentage.

Negotiation angle that often works:

Fixed escalations are easiest to justify internally. They also make it easier to create landlord competition because you can compare offers apples-to-apples across properties.

3. Hybrid Escalations (Fixed + CPI Triggers Or Limits)

Hybrid systems are where complexity starts doing real damage—or real good—depending on how they’re structured. A well-built hybrid can be a smart compromise in long-term deals. A poorly built hybrid can quietly recreate CPI risk while looking tenant-friendly.

The nuance in hybrids:

-

Hybrids should reduce volatility, not reintroduce it. The goal is a controlled range of outcomes. If a hybrid clause still allows large CPI swings with minimal limits, it’s not really a hybrid—it’s CPI with extra steps.

-

Trigger design is everything. A “trigger” could be CPI above a threshold, but you need to examine:

-

What measurement period is used?

-

What happens when CPI goes back down?

-

Does the escalation revert, or does it ratchet upward permanently?

-

Caps/floors can create asymmetry. A ceiling (cap) helps tenants. A floor helps landlords. Some hybrids include both—fine—unless the floor is set high and the cap is set too high to matter.

-

Hybrids can be structured as “bands.” For example: 3% unless CPI exceeds X, then 4% for that year only, then revert when CPI normalizes. That approach contains exposure better than “CPI in full if CPI exceeds X.”

Negotiation angle that often works:

Hybrids are a useful concession when landlords won’t commit to fixed increases across long terms. The tenant win is getting the hybrid to behave like a fixed schedule most years while limiting worst-case inflation exposure.

4. Rent Bumps (Set Dollar Increases)

Rent bumps are often viewed as simple, but they can carry their own nuance—especially in how frequently they occur and how they align to market dynamics.

The nuance in rent bumps:

-

Bumps can be more transparent than percentages. Stakeholders can understand “+$0.50/SF” more quickly than compounding percentages—useful for approvals and budgeting.

-

Frequency is negotiable in some markets. Annual bumps are common, but every-other-year bumps can appear when demand is lower or when landlords are trying to stabilize occupancy.

-

Bumps behave differently depending on the starting rent. A $1.00/SF bump is a larger effective percentage when starting rent is low and a smaller effective percentage when starting rent is high. That matters when comparing proposals.

-

Bumps can be paired with renewal options strategically. Tenants can sometimes negotiate different bump schedules for base term vs. renewal periods, aligning increases to business uncertainty.

Negotiation angle that often works:

If you can’t win on the bump amount, win on the timing (less frequent increases) or on other economic levers that reduce total occupancy cost.

Why CPI Escalations Tend To Be The Most Dangerous

CPI escalations feel reasonable because they’re anchored to “inflation,” which sounds objective. But CPI clauses are often where landlords can embed the most optionality and the least predictability for tenants. The biggest tenant-side risk isn’t CPI itself—it’s CPI without boundaries, combined with compounding.

REoptimizer® helps teams avoid the classic mistake: evaluating escalation clauses based on what inflation has been, rather than what it could be over the life of the lease.

How To Negotiate A More Tenant-Friendly Escalation

A strong escalation strategy typically looks like this:

-

Start with a fixed schedule preference (predictability wins internal buy-in)

-

If CPI enters the deal, contain it with clear caps and transparent definitions

-

Avoid one-way clauses (floors without meaningful caps, or ratchets that never revert)

-

Use competition to force landlords to price risk fairly

REoptimizer® supports this by turning lease language into a financial narrative: what you’re paying, when you’re paying it, and what could change under different conditions—so the negotiation isn’t emotional, it’s mathematical.

REoptimizer® Use Cases For Escalation Clauses

-

Clause Risk Flagging: Identify CPI, ratchets, floors, and hybrid triggers early—before late-stage legal review.

-

Scenario Modeling: Test inflation environments so teams can see exposure boundaries, not just the “expected” path.

-

Budget-Ready Rent Schedules: Generate stakeholder-friendly schedules that align to term, options, and renewal structure.

-

Negotiation Prep: Quantify alternatives so you can trade intelligently (e.g., escalation concessions in exchange for TI, free rent, or better renewal terms).

Schedule a demo today to see hoe REoptimizer® can level up your portfolio by strengthening each individual lease.

Book a Demo

FAQ’s Rent Escalation:

Which rent escalation is safest for tenants?

Most tenants prefer 2. Fixed Percentage Escalations because predictability reduces budget risk and approval friction.

Why can CPI escalations become expensive even if inflation falls later?

Because rent is usually compounding. A high CPI year can increase the base rent permanently, and subsequent increases build on that higher number.

Are hybrid escalations good or bad?

3Hybrids can be good when they genuinely limit volatility (caps, bands, reversion). They’re risky when they add complexity without adding real limits.

Are rent bumps better than fixed percentages?

Rent Bumps can be excellent for transparency and, in some cases, negotiable frequency. The “better” option depends on starting rent, bump size, and term length.

Commercial lease renewals are no longer a routine administrative task. In today’s office market, they are one of the most powerful—and underutilized—levers for reducing occupancy costs, improving space utilization, and reshaping a company’s real estate portfolio.

Done strategically, a renewal can unlock millions in savings, flexibility, and optionality. Done passively, it can quietly lock in outdated economics, underused space, and unnecessary risk for years.

This guide explains how to approach commercial lease renewals—and how modern portfolio intelligence tools like REoptimizer® allow tenants to make renewal decisions with clarity, leverage, and confidence.

What Is A Commercial Lease Renewal?

A commercial lease renewal is the process of extending, renegotiating, or restructuring an existing office lease before its expiration. While many leases include renewal options, exercising them without market analysis can be one of the most expensive mistakes tenants make.

A renewal should be treated as a new transaction, evaluated against current market conditions, space utilization, and long-term business strategy—not as a default continuation of the past.

Why Commercial Lease Renewals Matter Right Now

The office market didn’t just “bounce” into a new cycle—it repriced risk and value. That shows up in how landlords underwrite deals, how employees experience offices, and how finance teams judge real estate decisions.

-

Hybrid Work Changed Utilization, Not Just Attendance

It’s not simply “fewer days in-office.” It’s spikier demand (peaks midweek, valleys Monday/Friday), more cross-functional collaboration days, and greater sensitivity to layout quality. Two companies can have the same headcount and radically different space needs depending on scheduling norms, team structure, and meeting behavior.

-

Vacancy Is Elevated, But Leverage Is Uneven

Many submarkets have plenty of availability, yet best-in-class buildings can still command stronger pricing and terms because they’re winning the “flight to quality.” That means renewals aren’t about “rent down” everywhere—they’re about choosing whether you’re paying for quality, flexibility, or pure cost, and negotiating accordingly.

-

The Real Gap Is Between “Contracted Rent” And “Market Reality”

A lot of tenants are sitting in leases negotiated under very different assumptions—growth projections, in-office expectations, and rent trajectories. Even when face rent looks acceptable, the total economics can drift: escalations compound, operating expenses rise, and older leases often lack modern flexibility (givebacks, expansion rights, sublease freedom, termination options).

-

Capital Markets And Building Health Now Matter To Tenants

Lease decisions used to be mostly about space and price. Now, tenants also have to think about landlord capacity to fund improvements, maintain services, and execute capital work. Building-level financial stress can translate into operational friction—or become leverage if you understand the owner’s incentives and timing.

-

Costs To Move Or Build Out Are Higher And More Variable

The renewal vs. relocate math isn’t just about rent. It’s about TI dollars, construction timelines, permitting risk, downtime, furniture/IT, and change management. In many cases, the “cheapest rent” option loses once you model the full cost and risk to execute.

-

Leadership Teams Want Finance-Grade Decisions

CFOs and executives increasingly expect real estate choices to be justified like any other investment: NPV impact, scenario planning, risk tradeoffs, and measurable utilization—not anecdotes like “people like the building.” That’s why the renewal window is so valuable: it’s one of the few times you can make a high-impact change with a clear decision point and negotiation leverage.

Net: the renewal window is one of the only moments where tenants can reset economics, right-size intelligently (not blindly), and rebalance portfolios—but only if they have visibility into things like remaining lease NPV, true utilization by site, comparable deal terms, and relocation scenarios (exactly the inputs tools like REoptimizer® are built to centralize).

The Four Most Common Commercial Lease Renewal Mistakes

1. Treating A Renewal Like A Paperwork Exercise

Tenants often assume that staying put is the safest option. Familiarity with the space, landlord, and commute patterns can create a false sense of security.

But renewing without analysis often means:

-

Overpaying above market rent

-

Carrying excess or poorly configured space

-

Locking into outdated lease terms and escalations

A renewal is a multi-year financial commitment and should receive the same scrutiny as a new lease—sometimes more.

2. Negotiating Without Understanding True Portfolio Economics

Many tenants negotiate renewals in isolation, looking only at:

-

Current rent

-

Renewal option language

-

Short-term savings

What’s often missing is visibility into how each lease performs inside the broader portfolio.This is where modern portfolio analytics change the game.With REoptimizer®, tenants can:

-

See the remaining Net Present Value (NPV) of each lease

-

Understand how future rent escalations compound over time

-

Compare the cost of staying versus relocating or restructuring

-

Identify which locations are financial outliers

Without this data, tenants negotiate blind.

3. Ignoring Utilization And Right-Sizing Opportunities

Excess space is one of the largest hidden costs in corporate real estate.

Many organizations no longer need the same footprint they signed for years ago—but that doesn’t always mean a simple reduction. The real opportunity lies in nuanced optimization. REoptimizer® enables tenants to:

-

Measure utilization at each site

-

Identify underused locations and redundant footprints

-

Evaluate whether satellite offices can be consolidated

-

Model scenarios like combining locations into a single, higher-quality hub

Instead of asking, “How much space do we cut?” The better question is, “How should our space actually work?”

4. Failing To Leverage The Market With Real Alternatives

Landlords negotiate differently when they know a tenant has credible options.

However, “alternatives” only create leverage if they are:

-

Comparable in quality and function

-

Priced accurately on a net-effective basis

-

Evaluated alongside renewal economics

REoptimizer® allows tenants to:

-

Match renewal terms against true market comparables

-

Compare new locations side-by-side with the existing lease

-

Model total occupancy costs across multiple scenarios

-

Create defensible competition for their tenancy

This transforms negotiations from reactive to strategic.

How REoptimizer® Changes The Commercial Lease Renewal Process

Traditional renewal planning relies on spreadsheets, fragmented data, and anecdotal market knowledge. REoptimizer® replaces that with a centralized decision platform.

Portfolio-Level Intelligence

Utilization And Strategy Alignment

-

Site-level utilization insights

-

Identification of consolidation and combination opportunities

-

Alignment with hybrid work policies and growth plans

Market And Scenario Comparison

-

Comparable lease benchmarking

-

Renewal vs. relocation modeling

-

Side-by-side evaluation of multiple options

Faster, Better Decisions

-

Clear visuals for executives and finance teams

-

Scenario modeling that supports internal buy-in

-

Data-backed negotiation strategies

The result: better outcomes with less guesswork.

When Should You Start Planning A Commercial Lease Renewal?

For most office tenants, renewal planning should begin 18–36 months before lease expiration, depending on portfolio size and complexity.

Starting early allows tenants to:

-

Identify leverage well before deadlines

-

Avoid costly extensions or rushed decisions

-

Use time as a negotiating advantage

-

Align real estate decisions with broader business planning

With tools like REoptimizer®, early planning becomes practical—not overwhelming.

The Bottom Line: Renewals Are Where Portfolios Are Won Or Lost

Commercial lease renewals are no longer about simply staying or leaving. They are about optimizing an entire portfolio—financially, operationally, and strategically.

Tenants who succeed will:

-

Treat renewals as new investments

-

Use data, not assumptions

-

Understand utilization at a granular level

-

Leverage market alternatives intelligently

-

Equip themselves with the right technology and representation

REoptimizer® doesn’t replace strategy—it enables it.Want to see how it can level up your portfolio? Book a demo today.

Book a Demo

Commercial Lease Renewal FAQs

When Should I Start Planning A Commercial Lease Renewal?

Most tenants should begin planning 18–36 months before lease expiration. Starting early gives you time to benchmark the market, build internal alignment, and create real negotiating leverage—without risking costly extensions or rushed decisions.

Should I Exercise My Renewal Option Or Renegotiate?

A renewal option is not automatically the “best deal.” Many option clauses reset only some terms (or lock in above-market economics). The safest approach is to price the option against market comparables and alternative locations, then choose the path with the best net-effective outcome.

How Do I Know If I’m Overpaying Rent?

You’re likely overpaying if your lease was signed in a stronger market and has compounding escalations, or if comparable buildings are offering better economics (rent, concessions, flexibility). The most reliable test is a true side-by-side comparison of:

-

Base rent + escalations

-

Operating expenses (and caps)

-

Tenant improvement allowance

-

Free rent / abatement

-

Move, build-out, and downtime costs

What Are The Biggest Negotiation Levers In A Lease Renewal?

Most renewal wins come from negotiating the full value stack, not just rent:

-

Tenant improvement (TI) dollars

-

Free rent / rent abatement

-

Operating expense protections (caps, exclusions, audit rights)

-

Flexibility clauses (expansion, contraction, termination options)

-

Parking, signage, and amenities

-

Sublease and assignment rights

Can I Reduce My Square Footage During A Renewal?

Often, yes—but it depends on building layout, the landlord’s leasing strategy, and timing. Many tenants pursue:

-

A direct reduction (smaller suite)

-

A re-stack within the building

-

A blend-and-extend with resizing

-

A partial giveback paired with a longer term

The key is to make the new footprint worth it to the landlord (term, credit, stability, or avoided vacancy risk).

How Do I Measure Office Utilization Before A Renewal?

Utilization should reflect how people actually use the space—by day, department, and peak periods—rather than assumptions. Measuring utilization helps you avoid renewing excess space and can reveal opportunities like consolidating teams, redesigning layouts, or combining nearby satellite locations.

What Is Remaining Lease NPV And Why Does It Matter?

Remaining lease NPV (Net Present Value) estimates the value of your remaining lease obligations in today’s dollars. It helps decision-makers compare options like:

-

Renewing vs. relocating

-

Downsizing vs. reconfiguring

-

Shorter term vs. longer term

-

Paying more now vs. avoiding higher long-term cost

NPV makes “stay vs. go” a finance-grade comparison instead of a gut call.

How Can REoptimizer® Help With Lease Renewals?

REoptimizer® helps tenants turn renewals into a portfolio optimization decision by enabling you to:

-

See the remaining NPV of each lease

-

Understand escalation exposure and term risk

-

View utilization by site to identify right-sizing opportunities

-

Spot nuanced consolidation plays (like combining satellite locations)

-

Match market comparables and benchmark deal terms

-

Compare renewal vs. new location scenarios side-by-side

How Do I Create Leverage In A Renewal Negotiation?

Leverage comes from credible alternatives and a clear plan. The best path is to:

-

Identify 2–4 realistic relocation options

-

Compare them against the renewal on a net-effective basis

-

Communicate that you can execute (not just “shop around”)

-

Keep options alive until the renewal is fully documented

Do I Need A Tenant Representative For A Renewal?

It’s not required, but it’s often the difference between an average deal and an optimized one. A tenant rep brings:

-

Market benchmarks and comp visibility

-

Negotiation strategy and leverage building

-

Term and legal-risk awareness

-

Time savings and process control

What If I Wait Too Long To Start The Renewal Process?

If you wait, you risk:

-

Losing renewal rights or negotiation windows

-

Paying for expensive short-term extensions

-

Accepting unfavorable terms due to time pressure

-

Missing better market opportunities

Time is leverage—starting early protects it.

By this year, the U.S. office market had settled into a fragile balance built on expensive stability.Tenant Improvement Allowances (TIAs)—the cash landlords provide for tenant buildouts—had soared to unprecedented levels, up a whopping 112% since 2016 according to Savills and CompStak.