In a year that once again tested expectations across commercial real estate, 2025 emerged not as a dramatic turnaround story but as a strategic inflection point—particularly for office and industrial sectors.

For corporate tenants and CRE teams navigating hybrid work, supply chain shifts, and capital market stress, the data tell a clear story: performance now hinges on precision, not prediction.

1. Office Market: Stabilizing — But Still Reshaping Demand

After years of pandemic-era contraction, the U.S. office market showed meaningful signs of stabilization in 2025—even if the recovery remains uneven and deeply contextual.

Attendance Patterns Point to Growing Stability

Office traffic has steadily climbed throughout the year, with national office attendance approaching 72.6% of pre-COVID levels in 2025 according to foot-traffic analytics. This marks a dramatic increase from the pandemic troughs and represents one of the strongest rebounds since 2020.

These attendance gains have real economic implications. Not only do they support stabilization in rental dynamics and tenant confidence, but they also provide the workforce presence necessary to justify continued investment in office space, amenities, and hybrid collaboration zones.

Additionally, the proportion of corporations actively tracking attendance jumped to 69%, reflecting a growing recognition that employee attendance data are not just operational but strategic for measuring impact on productivity, utilization, and tenant experience.

Vacancy Remains High, But Market Fundamentals Are Improving

Office vacancy, though elevated compared to historical norms, edged slightly lower in 2025. National vacancy hovered around 18.6% in late 2025, a modest dive relative to the record highs it experienced through 2023–24.

In major gateway markets like New York City, vacancy pressure is easing. Moody’s data show that while vacancy rates remain above long-term averages, net absorption turned marginally positive in 2025, a sign that employers with clear hybrid strategies are contributing to localized demand growth.

Meanwhile, leasing activity in key submarkets underscored renewed confidence. Downtown Manhattan saw vacancy fall to 23% with average asking rents rising by over 3% year-over-year—a strong performance relative to broader national trends.

Flight to Quality Persists

Vacancy is no longer a single market condition—it’s a two-tier outcome tied to asset quality. And the 18.6% average vacancy can be misleading when we look at it as a whole. The more important story for occupiers is the duality inside that number.

The office market isn’t recovering uniformly; it’s splitting by asset quality and by submarket, creating a widening performance gap between buildings that can win talent back (and justify on-site days) and those that can’t.

Across major markets, leasing activity continues to tilt toward Trophy/Class A, while Class B/C’s share shrinks—a pattern that effectively pulls fundamentals upward for the best assets while leaving commodity stock behind.

Manhattan is one of the clearest examples of this duality: Trophy properties captured 61.6% of Manhattan leasing activity in Q1 2025 (by class), an unusually concentrated signal that tenants are choosing “best-in-market” space even when overall demand is still recovering.

Why This Matters For Corporate Tenants

Flight to quality is often framed as a landlord story. For occupiers, it’s a portfolio performance lever:

- Trophy/Class A is becoming the “utilization bet.” If your workplace strategy relies on consistent in-office patterns to drive collaboration and culture, premium assets increasingly act like the infrastructure that makes that behavior easier to sustain.

- Class B/C is becoming a repositioning / pricing bet. There can be value, but the underwriting has to assume higher volatility and larger gaps between “leased” and “used” space—plus greater reliance on concessions and landlord capex to stay relevant. (This is why conversion/repositioning talk keeps rising in market reports.) Not to mention a lot of these assets are being phased out of the market completely as conversions take shape.

2. Industrial: Continued Demand, With Nuanced Supply Dynamics

Industrial real estate sustained its long run of relative strength in 2025, even as supply and demand shifted toward equilibrium.

Long-Term Occupancy Growth Is Unbroken

Industrial tenant demand remained positive for the 60th consecutive quarter, a streak that now spans nearly 15 years—a testament to structural drivers such as e-commerce logistics and manufacturing rebalancing.

However, industrial vacancy did tick higher, reaching around 7.3% in Q2 2025, as move-outs and completions both contributed to slight softening.

Rent Growth Moderates, but Demand Diversity Expands

Industrial rent growth softened compared to the rapid gains of the pandemic era.

That said, diversification within the sector—especially toward cold storage, last-mile logistics, and automation-ready assets—continues to support strategic leasing and long-term tenant retention.

For tenants, this trend underscores the increasing importance of site selection analytics that match inventory with evolving supply chain footprints rather than broad assumptions of generalized growth.

The Construction Pipeline: Why Rent Growth Didn’t Collapse

That demand diversification is landing at the exact moment the industrial pipeline is drying up—which is a big reason rent growth moderated instead of falling off a cliff.

- Space under construction fell ~61% from the 2022 peak, dropping to ~279M SF in Q1 2025, with forecasts calling for the pipeline to dip below 250M SF by year-end.

- At the start of 2025, nationwide industrial construction was already down ~25% year-over-year, signaling a clear pullback in new supply.

The supply picture also explains the “two-speed” industrial market corporate tenants are feeling: vacancy rose to ~7.1% nationally in Q2 2025, yet small warehouses (<100K SF) stayed tight at ~4.4% vacancy—exactly the segment most aligned with last-mile and serviceable infill demand.

Net: 2025’s pipeline reset is quietly supporting pricing power in the right product types—especially smaller, well-located, higher-spec space—while pushing tenants toward sharper site selection analytics to avoid being trapped between soft big-box supply and scarce infill options.

3. Capital Markets and CRE Valuations: Discipline and Divergence

2025’s capital markets landscape accentuated a central reality: value is emerging at the intersection of risk management and operational data.

- Persistent headwinds in office valuations continued, with commercial property values still well below pre-pandemic levels in many categories.

- Conversely, industrial and select retail assets maintained relative valuation resilience due to consistent demand fundamentals and niche structural drivers.

For CRE teams, this divergence is a reminder that portfolio performance is not monolithic. Markets like Sun Belt logistics hubs and high-amenity urban cores are commanding differentiated risk premiums based on robust utilization and tenant demand clarity.

4. CRE Tech & Analytics: A Strategic Imperative

Perhaps the most pervasive trend of 2025 is the integration of advanced analytics, automation, and real-time occupancy intelligence into every layer of CRE decision-making.

From attendance tracking that informs space allocation and workplace strategy to predictive models that anticipate lease expirations and submarket pricing shifts, CRE technology is now a core operational competency—not a novelty.

This evolution reflects a broader shift from reactive portfolio maintenance to strategic portfolio optimization powered by reliable, real-time data.

And no where is the promise of real time data more profonde than the emergence of AI. It’s really the elephant in the room when we talk about the trends that have taken shape in 2025.

A Global Real Estate Technology Survey captures the moment bluntly: ~90% of organizations are piloting AI, yet only ~5% report achieving all (or most) of their AI goals—a gap that signals both massive momentum and a lot of wasted spend if the data foundation isn’t ready.

What AI Changes For Corporate Tenants And CRE Teams

AI isn’t just making reporting faster. It’s starting to rewire how portfolios are run:

- From static planning to continuous optimization: AI-enabled platforms can blend utilization, lease terms, operating costs, and market data to surface opportunities in near-real time (not quarterly).

- From “attendance” to predictive operations: The next step after occupancy dashboards is AI that flags leading indicators—teams drifting off hybrid norms, sites with creeping underutilization, rising overtime exposure, or policy exceptions that create compliance risk—early enough to intervene.

- From workflow automation to measurable efficiency: Morgan Stanley Research estimates AI could drive $34B in efficiency gains for the real estate industry over the next five years (through 2030) by automating tasks and improving productivity—exactly the kind of savings corporate occupiers will expect their CRE orgs to capture.

Right now, companies are pouring billions of dollars into the development of AI technology. For now, we’re in a bit of a watch and wait mode to understand how its full potential will affect workforce dynamics. But not to mention, it stands ready to slash hundreds of thousands of jobs.

Looking Ahead: 2026 and Beyond

As we close the books on 2025, a few imperatives emerge for corporate tenants and CRE teams:

- Measure utilization meaningfully: Moving beyond nominal occupancy figures to correlated productivity and performance metrics will define competitive advantage.

- Anticipate hybrid dynamics: The office is no longer “either dead or alive”; it is a flexible, culture-dependent asset whose value must be quantified, not assumed.

- Diversify CRE strategy by sector insight: Industrial dynamics will continue to strengthen, but their performance will be location and use-case specific.

- Embed analytics in every decision: From attendance data to portfolio repositioning, advanced data platforms are no longer optional—they are essential.

2025 wasn’t a year of simple narratives. It was one defined by data-informed nuance, measured progress, and strategic recalibration. For forward-thinking tenants and CRE professionals, the lesson is unmistakable: precision beats prediction.

November 2025 delivered the strongest November office occupancy since 2019 when measured by average visits per working day, even though total visits remain below pre-pandemic levels. In other words: office attendance is rising, but it’s rising unevenly—and the “headline” number can be misleading if you don’t normalize for working days.

For corporate tenants managing large-scale portfolios, that distinction matters. Because when you’re making lease, space-planning, and operating decisions across multiple markets, you’re ultimately trying to answer a simple question:

Are we getting the physical presence we’re paying for—and is it improving team productivity and business operations?

This is where attendance tracking, workforce analytics platform capabilities, and disciplined employee attendance management separate reactive portfolio management from proactive strategy.

Why “Visits” Aren’t Enough For Corporate Tenants

Placer.ai’s index can tell you how buildings are being used at the market level. But inside an enterprise portfolio, you need accurate attendance intelligence that connects:

- Employee attendance and attendance patterns by site, day, and team

- Time and attendance and employee hours for operational planning

- Productivity metrics and outcomes (not just bodies in seats)

- Compliance with labor laws, especially for non exempt employees

- Labor costs, including monitor overtime controls and scheduling waste

The gap between “the city is recovering” and “our portfolio is performing” is often just one thing: reliable, decision-grade attendance records and accurate records you can trust.

The New Reality: Market-Level Office Attendance Is Diverging

The November 2025 story is not a single national narrative—it’s a set of local stories that impact tenant strategy.

Sun Belt Momentum And Commute Dynamics

Miami maintained its lead in the office recovery and widened the gap versus New York, supported by corporate relocations and commute dynamics.

Weather, Transit, And Attendance Softness

New York saw attendance ease, with seasonal weather and transit-heavy commutes weighing on in-office days.

Tech Markets Showing Real Rebound Signals

San Francisco recorded some of the strongest year-over-year gains, signaling a meaningful turnaround, with other tech-influenced markets (Denver, Chicago, Boston) also improving—while still below pre-pandemic levels.

Policy And Local Economics Still Create Downside Risk

Houston and Washington, D.C. posted year-over-year declines tied to local industry/policy headwinds, including shutdown spillover. For tenants, this widening divergence means you should stop assuming one return-to-office playbook works everywhere. The portfolio winners will be the ones who can measure attendance precisely, then adapt site strategy accordingly.

From Counting Heads To Managing Risk: Attendance Monitoring As A Control System

In large portfolios, tracking employee attendance isn’t just an HR function—it’s risk management. Weak attendance monitoring can create:

- Compliance issues and compliance risks (meal/rest rules, overtime, scheduling documentation)

- Payroll errors and payroll mistakes caused by bad time capture

- Time theft and buddy punching when systems rely on unchecked manual inputs

- Higher employee absenteeism, poor attendance, and lost productivity

- Inconsistent treatment that can trigger disputes or disciplinary action risk

If you’re still relying on manual systems (spreadsheets, ad hoc badge checks, manager estimates), you’re not just missing insight—you’re increasing operational exposure.

What A Modern Attendance Solutions Stack Looks Like

Corporate tenants increasingly need attendance solutions that unify workplace utilization with employee time controls—without turning the office into a surveillance zone.

A pragmatic enterprise approach usually includes:

1) Employee Attendance Software That Produces Reliable Data

Look for employee attendance software and attendance software that supports:

- Real time tracking and real time attendance

- Automated systems for clock-ins, exceptions, and approvals

- Comprehensive reports for leaders and hr teams

- Clean integrations for payroll processing and time off requests

- Auditable employee attendance records and attendance records

2) Time Tracking That Matches How People Actually Work

In hybrid reality, you need time tracking that can:

- Track time for remote employees and remote workers

- Support flexible schedules and modern work patterns

- Help monitor overtime without punishing legitimate flexibility

- Provide valuable insights into staffing, not micromanagement

3) Optional Stronger Identity Controls Where Risk Requires It

In certain environments (high-security, regulated, or high time-theft exposure), organizations may consider:

- Biometric time clocks

- Facial recognition

- Secure on-site check in workflows: These can reduce security risk, prevent buddy punching, and improve the integrity of employees clock events—but should be deployed with clear purpose, transparency, and policy governance to protect a positive work environment.

Portfolio Use Cases That Actually Move The Needle

Here’s how tenants use attendance monitoring and analytics to improve outcomes (without “cramming” a mandate everywhere):

Space Planning And Lease Strategy

Use attendance data to identify underutilized sites, then right-size footprints, adjust amenity investment, or renegotiate renewal terms based on real demand.

Team Collaboration And In-Office Design

If your goal is better team collaboration, don’t guess. Compare attendance patterns to meeting density and project milestones. Design on-site days around collaboration, not routine solo work.

Productivity And Cost Control

Tie employee productivity and team productivity to a small set of measurable signals:

- Focus time vs. meeting time

- Cycle times and throughput

- Productivity metrics by team and site: Then decide where “in office” truly improves outcomes—and where remote execution is more effective.

Early Signs And Intervention

Use analytics to spot early signs of systemic issues: spikes in unplanned absences, schedule friction, approval bottlenecks, or manager-level inconsistencies. Pair this with wellness programs or workload adjustments before problems become attrition.

Maintain Compliance Without Killing Culture

Corporate tenants can ensure compliance and still support flexibility if they treat attendance as policy + systems + fairness:

- Document clear attendance policies and how exceptions work

- Configure rules by employee category (especially non exempt employees)

- Keep work hours and overtime logic consistent across locations

- Use systems to reduce disputes: auditable accurate records prevent “he said / she said”

When done well, managing attendance becomes a trust-building operating rhythm—not a morale drain.

Frequently Asked Questions About Employee Attendance Tracking

What’s The Difference Between Office Attendance And Employee Attendance?

Office attendance often measures building usage (visits), while employee attendance tracking focuses on who worked, where, and when—supporting scheduling, compliance, and payroll accuracy.

Why Do Corporate Tenants Need Attendance Tracking If They Have Access Control Data?

Badge swipes can indicate entry, but they often don’t produce compliant employee attendance records, don’t support time and attendance rules, and can miss hybrid patterns or onsite duration needed for operational decisions.

How Do We Monitor Attendance Without Micromanaging?

Focus on outcomes and exceptions. Use attendance monitoring to run business operations (staffing, space, compliance), not to scrutinize every minute. Make reporting transparent and limit access to role-based needs.

How Does Attendance Tracking Reduce Payroll Errors?

By automating capture and approvals, and integrating with payroll, you reduce manual edits, missed punches, and inconsistent rounding—common causes of payroll errors and payroll mistakes.

What Corporate Tenants Should Do Next With REoptimizer®

If you’re managing a large portfolio, the next phase of the office recovery isn’t about guessing—it’s about governing with data.

REoptimizer® helps corporate tenants:

- Create a single source of truth for employee time and attendance across every location—so leadership, HR teams, and operations are aligned.

- Replace manual systems with automated, reliable data that supports accurate records, fewer payroll errors, and stronger compliance.

- Track what matters in one portfolio view: real time attendance, overtime exposure, absence trends, and site utilization—so you can spot issues early and act fast.

- Use workforce insights to refine hybrid strategy so in-office time improves collaboration and team productivity—not just policy compliance.

Office attendance may be hitting post-pandemic highs, but portfolio advantage comes from what you do next. When markets diverge and every square foot has to justify itself, REoptimizer® turns attendance data into clear actions—so you can reduce risk, control labor costs, and optimize space with confidence.

Ready to see what your portfolio is really telling you? Request a REoptimizer® demo and get a portfolio-level attendance and utilization readout tailored to your footprint.

Book a Demo

CRE transaction management software is a platform that helps you run commercial real estate deals end-to-end—from requirements and site selection through negotiations, approvals, documentation, and close—so every deadline, cost, and decision is tracked in one place (instead of living in spreadsheets, inboxes, and scattered folders).

REoptimizer® is built for exactly this: centralizing portfolio data and automating reporting, alerts, and workflows so teams can move faster and negotiate from a stronger position.

Who Can Benefit from CRE Transaction Management Software?

If your organization has more than a few locations—or multiple deals happening at once—transaction management software becomes a necessity, not a “nice to have.”

Typical users include:

- Corporate Real Estate (CRE) And Portfolio Strategy teams managing growth, consolidation, relocations, and renewals

- Finance / FP&A tracking budgets, approvals, and forecast vs. actual

- Legal managing LOIs, redlines, and compliance documentation

- Operations / Workplace / Facilities aligning space with headcount and utilization

- Executives who need a clear view of deal risk, savings, and timing

REoptimizer® is positioned for enterprise teams dealing with complexity—replacing “spreadsheets, siloed systems, and manual processes” with a single system of record.

What CRE Transaction Management Software Does

At its core, CRE transaction management software helps you:

- standardize the process (repeatable workflows and checklists)

- coordinate people and deadlines (ownership, reminders, accountability)

- organize documents (versions, approvals, audit trail)

- track costs line-by-line (so overages don’t hide in the noise)

- report in real time (so leadership isn’t waiting on a “Friday spreadsheet”)

REoptimizer® adds a key layer: it’s designed to help teams compare deal economics against comps and benchmarks and generate reporting fast with templates—because the real money is won or lost in the details.

Where It Fits (And Why It’s Not The Same As Lease Management)

A simple way to think about the lifecycle:

Before The Deal: Strategy And Site Search

This is where teams define what they need and evaluate options. REoptimizer® supports this with KSDs (Key Site Drivers) and tools like CRESiteIQ™, built to analyze markets, compare sites, and visualize opportunities. More on in the next section…

During The Deal: The Transaction Itself

This is the heavy-lift phase: comps, negotiations, approvals, legal, due diligence, and getting to signature/close.

After The Deal: Lease Management

Lease management is what happens after execution—tracking key dates like renewals, expirations, options, and escalations. REoptimizer® content points out how missed key dates can create real cost and risk at portfolio scale.

Bottom line: lease management is “operate what you signed.” Transaction management is “control what you sign.”

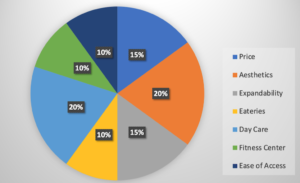

What Are KSDs?

KSDs (Key Site Drivers) are the criteria that define what “best location” means for your business—then you weight and score them so every option can be compared objectively (not emotionally, not anecdotally, and not based on whoever toured last). Consider them your highly unique KPI’s.

REoptimizer® uses KSDs to score each property in real time and calculate a final weighted score per building, instantly ranking your top contenders side-by-side.

Why KSDs Are Invaluable (And Why Teams That Use Them Win More Often)

They Turn “Opinions” Into A Repeatable Decision System. Without KSDs, site selection usually sounds like:

- “This one feels right.”

- “The price is good, but…”

- “Leadership likes that submarket.”

KSDs force alignment upfront. You define the “must-haves” and “deal-breakers” before you tour, so your team is evaluating every property against the same standard.

They Help You Compare The Stuff That’s Hard To Measure

Price and square footage are easy. The real risk is everything else:

- Workforce access and commute patterns

- Truck access and delivery windows

- Power capacity and future expansion needs

- Column spacing, dock ratios, clear height (industrial)

- Customer proximity and logistics cost impacts

- Rent vs market comps (and trend direction)

- Total Occupancy Cost (rent + CAM/NNN + taxes + insurance + utilities)

- Current utilization vs required utilization (desk sharing, peak days)

- Adjacency needs (teams that must be near each other

- Layout efficiency (loss factor, usable vs rentable SF)

REoptimizer’s® KSD approach is designed specifically to capture those “hard-to-quantify” drivers and make them scorable—so the best site isn’t just the cheapest, it’s the lowest total cost of occupancy and best operational fit.

They Save Time By Eliminating Bad-Fit Tours Early

One of the most expensive mistakes companies make is touring before they’ve defined what matters most. REoptimizer calls this out directly: teams waste time touring warehouses without clear KSDs—then end up revisiting assumptions mid-process. When KSDs are set first, you filter faster and only tour buildings that can realistically win.

They Strengthen Negotiations Because You Know Your Leverage

When you can prove (with scoring) that multiple buildings meet your needs, negotiations change:

- You’re selecting from the strongest options and negotiating from leverage.

- You can back up concession requests with evidence, using comps plus the operational requirements that drive real value.

- You reduce waste by not paying extra for features that don’t move the needle for your business.

Because Reoptimizer® scores contenders side-by-side and ranks them instantly, your team walks into negotiation with clarity: what matters, what doesn’t, and what you can walk away from.

They Keep The Portfolio Aligned With The Business (Not Just The Deal)

The biggest value of KSDs isn’t picking a building—it’s ensuring every location decision supports the business:

- growth plans

- service levels

- labor strategy

- cost targets

- utilization and waste reduction

REoptimizer’s® broader positioning is exactly this: giving teams visibility into overspending and underused space, then translating that into action through dashboards and metrics—so site decisions don’t live in a one-time spreadsheet, they become an operational advantage.

How REoptimizer® Makes KSDs Practical (Not Just A Worksheet)

Here’s the difference between “having KSDs” and using KSDs:

- Score Each Property In Real Time: As you evaluate a site, REoptimizer scores how well it delivers on each KSD—immediately, even while touring.

- Rank Overall Suitability: REoptimizer calculates a weighted score per building and instantly highlights top contenders.

- Expand Site Intelligence With CRESiteIQ™: For location strategy, CRESiteIQ™ helps define what matters and compare sites using many data points (example categories include demographics, income, fuel costs, population trends, and more).

Why Your Portfolio Needs CRE Transaction Management Software

In CRE, savings (or losses) don’t come from “being organized.” They come from making better decisions earlier and catching issues before they get locked into the deal.

Transaction management software helps you:

- Avoid missed deadlines that weaken leverage

- Prevent “death by a thousand line items” (fees, escalations, TI, concessions, operating assumptions)

- Benchmark against comps instead of negotiating blind

- Expose underutilization and waste so the portfolio improves over time

REoptimizer® specifically highlights eliminating wasted effort by centralizing data and automating alerts/workflows—so teams spend time on strategy, not chasing updates.

Why Spreadsheets Don’t Work For Transaction Management

Spreadsheets are fine for a single deal. They fail when you’re handling:

- Multiple stakeholders and approvals

- Changing versions of assumptions and documents

- Market comps, benchmarks, and reporting needs

- Utilization/waste measurement across a portfolio

That’s why REoptimizer® focuses on replacing spreadsheets and siloed tools with a centralized platform and automation.

FAQs

What Is CRE Transaction Management Software?

It’s software that manages the full commercial real estate deal process—tasks, deadlines, documents, approvals, and costs—from strategy through close, so nothing falls through the cracks.

How Is CRE Transaction Management Different From Lease Management?

Lease management is post-signature administration (key dates, escalations, compliance). Transaction management covers the whole process where the economics and terms are created.

Who Needs CRE Transaction Management Software?

Any company with a multi-location portfolio or frequent transactions—especially when deals involve finance, legal, operations, and leadership approvals.

How Does REoptimizer® Help With CRE Transaction Management?

REoptimizer® helps enterprise teams centralize portfolio data and automate reporting, alerts, and workflows—and supports site selection and deal evaluation with KSD scoring and related tools.

What Is CRESiteIQ™?

CRESiteIQ™ is a REoptimizer® tool for site selection, built to analyze markets, compare sites, and visualize opportunities in one platform.

What Are Key Site Drivers (KSDs) In Commercial Real Estate?

KSDs are your business’s weighted location criteria—used to score and compare properties objectively so you can identify the best-fit sites faster.

Why Should KSDs Be Weighted?

Because not all criteria matter equally. Weighting prevents teams from over-prioritizing “nice-to-haves” (or the loudest opinion) over the drivers that actually impact cost, operations, and performance.

How Does REoptimizer Use KSDs?

REoptimizer® scores each property against your KSDs in real time and produces a final weighted score to rank contenders side-by-side.

Learn more about REoptimizer® today.

High vacancy rates, a growing wave of landlord defaults, and a lingering oversupply of office space have created a rare market moment: corporate tenants can often secure better buildings on better terms—sometimes for less than they’d have paid years ago.

But there’s a catch. Distressed assets are a major risk and navigating this environment should not be taken lightly for tenants. To make it more difficult, they’re not waving a white flag announcing the trouble. There can be real risk hiding behind an address. This includes the landlord’s broader debt exposure, watchlist status, and cross-collateralized loans that can drag “healthy” properties down with “sick” ones.

That’s why today’s winners aren’t guessing—they’re using REoptimizer® to uncover which landlords are on a watchlist, what loans are at risk, and which properties may be tied together behind the scenes.

In this article, you’ll learn how to:

-

Define what makes a commercial property “distressed”

-

Understand why distressed buildings can be strategically valuable for tenants

-

Identify risk and opportunity using landlord watchlists and cross-collateral exposure

-

Negotiate smarter by knowing what the landlord can’t afford to lose

And while distressed properties aren’t automatically “bad,” the danger is leasing from a landlord whose portfolio-level risk can create operational, financial, and continuity headaches for your business. Let’s discuss.

What Defines a Distressed Commercial Property?

A commercial property is “distressed” when financial or operational pressure makes it undervalued, unstable, or at elevated risk of default, foreclosure, or forced restructuring. Common indicators include:

Loan Distress and Servicing Red Flags

-

Delinquencies (missed or late payments)

-

Special servicing transfers (a major warning sign that the lender has stepped in)

-

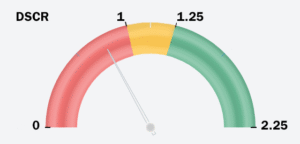

Weak DSCR (Debt Service Coverage Ratio) where income doesn’t comfortably cover debt payments

-

As a rule of thumb, DSCR below ~1.0–1.25 often signals heightened risk, depending on the lender and asset profile.

-

High Vacancy and “Silent Vacancy”

-

Vacancy rates: obvious indicator of weaker tenant demand and unstable cash flow

-

Under-occupancy (“dormant vacancy”): space that looks occupied today, but is functionally vacant the moment a lease rolls.

Market Saturation

Oversupplied submarkets create fire-sale leasing conditions—especially in older classes of inventory. Distress, in other words, isn’t just about a building. It’s about cash flow + debt + market pressure converging in a way that reduces stability and increases urgency.

How to Identify Distressed Properties (and Risky Landlords) the Smart Way

Whether you want to avoid distressed assets, audit your current portfolio, or capitalize on tenant-favorable conditions, your method matters. A quick “market scan” won’t cut it anymore.

1. Use Distress and Watchlist Intelligence (Not Just Comps)

Traditional leasing analysis is backwards-looking. Watchlist intelligence is forward-looking.

With REoptimizer®, you can evaluate a target building through the lens that matters most:

-

Is the landlord on a watchlist?

-

Is the loan associated with the property showing elevated risk signals?

-

Are there other properties in the owner’s portfolio that appear connected (cross-collateralized) to loans under stress?

This is how corporate tenants avoid signing a long-term lease under a landlord who may be forced into reactive decision-making.

2. Leverage CMBS and Loan-Performance Data for Negotiation Power

Platforms like Trepp and KBRA aggregate CMBS and credit performance data that can help identify pressure points. Key metrics to watch include:

-

Special servicing and delinquency flags

-

High LTV (Loan-to-Value): often signals thin equity and urgency to stabilize cash flow

-

Debt yield weakness: low debt yield indicates lenders may view the loan as higher risk

-

NOI declines and cap rate pressure: signals reduced income stability

Even if you don’t live in these datasets day-to-day, REoptimizer®’s watchlist visibility helps translate “credit stress” into real-world leasing decision support.

3. Track Market Indicators (At the Submarket Level)

Big headline vacancy numbers don’t negotiate your lease—micro conditions do.

Look at:

-

Vacancy by class (A vs. B/C)

-

Vacancy composition (shadow vacancy, near-term rollovers)

-

Net absorption trends by submarket, not just city-wide averages

-

Employer movement patterns and infrastructure investment

The best opportunities often sit in the gaps—where a submarket is weak overall, but a specific pocket is still strategically valuable.

Risks When Leasing a Distressed Building

The biggest risk is not the space—it’s the landlord’s financial position and what’s happening across their portfolio.

Key tenant risks:

-

Service degradation (maintenance delays, understaffed management)

-

Deferred capex (systems fail, upgrades stall)

-

Ownership disruption (sale, receivership, lender control)

-

Lease administration issues during restructures

Most importantly: a building that looks “fine” can still be risky if the owner is exposed elsewhere.

Why Distressed Properties Can Be a Strategic Advantage (If You Avoid the Wrong Risks)

Distressed office environments are brutal for landlords and lenders—but that stress can translate into meaningful tenant upside:

Cost Savings and Concessions

Distressed owners are often more willing to offer:

-

Lower base rent

-

Bigger TI (tenant improvement) allowances

-

Longer rent-free periods

-

Flexibility on term length, options, signage, etc.

Better Space for the Same (Or Less) Money

This is where tenants can “trade up” into stronger locations or higher-class assets at reduced effective rates—boosting brand perception and talent attraction.

Negotiating Leverage

A landlord under pressure values predictable cash flow. A strong corporate lease can be the difference between stabilizing the asset—or sliding further toward default.

But here’s the part most tenants miss:

What Lease Protections Should Tenants Request in Distressed Situations?

If a property or owner shows financial stress, tenants should prioritize operational continuity and risk containment, not just pricing. High-value protections to negotiate:

-

Stronger landlord maintenance/service obligations

-

Clear remedies and cure periods

-

Delivery and TI completion guarantees

-

Operating expense transparency / caps (where feasible)

-

Rights tied to building disruption events (practical protections if conditions deteriorate)

The Hidden Risk: A “Fine” Building Owned by a Watchlisted Landlord

Even if your building looks safe, the owner’s portfolio may not be.

Landlords frequently use financing structures that can connect multiple properties to the same debt obligation. In cross-collateralized loans, several properties serve as collateral for a single loan (or interconnected loans). If one asset deteriorates, it can raise risk across all linked assets—even the ones performing well.

That can create tenant risks like:

-

Deferred maintenance or degraded building services

-

Slower response times from ownership/management

-

Surprise ownership changes or lender intervention

-

Disrupted capital plans (elevators, HVAC, lobby, build-out approvals)

-

Lease administration complications during restructures

Where REoptimizer® Changes the Game

Instead of relying on surface-level deal comps and a building tour, REoptimizer® helps tenants:

-

See which landlords are on a watchlist

-

Identify which properties appear tied to debt at risk of default

-

Spot potential cross-collateral exposure so you can avoid getting trapped in a portfolio-wide problem

This means you can pursue “distressed opportunity” while filtering out “distressed operator risk.”

How to Approach Negotiations Once You’ve Found a Target

When REoptimizer® shows ownership pressure (watchlist status, risky debt, portfolio flags), you don’t just “ask for a better deal.” You negotiate around what the landlord must solve.

High-impact asks commonly include:

-

Larger TI allowances (or turnkey build-outs)

-

Longer free rent and phased commencement

-

Stronger landlord work-letter commitments

-

More protective defaults/cure rights

-

Expanded termination/relocation rights (where appropriate)

-

Audit rights / transparency improvements in operating costs

Knowing the landlord’s risk profile helps you structure terms that protect your operations—not just your rent number.

Bottom Line: Distressed Can Be a Win—If You Can See the Landlord Risk

Distressed leasing environments create real opportunity for corporate tenants. But the smartest move isn’t simply finding a “cheap Class A building.”

It’s finding the right building owned by the right landlord, with a clear view into:

-

watchlist risk,

-

loan stress,

-

and cross-collateral exposure that could blindside you mid-lease.

That’s exactly what REoptimizer® is built for: turning opaque landlord risk into actionable intelligence—so your relocation is an advantage, not a gamble. Learn more about how to utilize REoptimizer® for portfolio wide visibility and strategic moves that will keep your portfolio safe for years to come.

After a year of waiting for the commercial real estate rebound that never quite arrived, 2026 is shaping up as the year when patience finally pays off.

Sure, macro uncertainty is still in the air—interest rates are high, trade negotiations are messy, and policy changes are giving investors heartburn. But look past the noise and the story is clear: the foundations for a recovery are solidifying.

According to Deloitte’s latest 2026 Commercial Real Estate Outlook, more than 850 global CRE executives are cautiously optimistic. The industry isn’t sprinting toward a comeback—it’s jogging with purpose. And those who know where to look are already seeing real opportunities take shape.

Macroeconomics: Still Cloudy, but the Sky’s Lightening

Let’s start with the elephant in every investor’s boardroom: the macro picture.

Last year, most of us expected 2025 to mark a full-fledged turnaround. That didn’t happen. Persistent inflation, “higher-for-longer” interest rates, and trade tensions kept the brakes on. Eighty-three percent of Deloitte’s respondents still expect revenue growth by the end of 2026—but that’s down slightly from 88% a year ago. Meanwhile, 68% expect expenses to rise. Translation: optimism remains, but wallets are tightening.

And yet, the sentiment index Deloitte tracks—a quick read on overall optimism—sits at 65, down a touch from last year’s 68, but miles above the 2023 trough of 44. This isn’t despair. It’s disciplined optimism.

Executives still expect improvement across core CRE fundamentals—leasing, rents, and capital costs—over the next 12 to 18 months. The biggest concerns now? Capital availability, interest rates, and the cost of capital. No surprise there. But an encouraging twist: cyber risk dropped off the worry list, while employee retention rose. That’s a signal that firms are finally pivoting from “crisis mode” toward rebuilding teams and strategy.

Debt Markets: From Distress to Opportunity

If 2024 was the year of the loan maturity cliff, 2025–2026 could be the year lenders and borrowers finally climb it.

There’s no denying the hangover from legacy loans. Over $1.7 trillion in U.S. commercial mortgages are facing maturity, many underwritten when rates were in the 3–4% range. With today’s rates closer to 6.5%, refinancing is painful—and only one in five firms expect to pay off upcoming maturities in full.

But here’s the silver lining: new debt is healthier. With valuations stabilizing and underwriting standards tightening, new loan origination volume rose 13% in early 2025—and a staggering 90% year-over-year. Spreads have tightened, capital access is improving, and even traditional banks are easing standards.

Private credit is leading the charge. Alternative lenders—private funds, insurance companies, high-net-worth investors—now make up 24% of U.S. CRE lending volume, well above the 10-year average of 14%. Globally, private credit markets hit $238 billion in 2024 and are on track for $400 billion in assets under management by decade’s end.

The message? The “shadow lenders” are now the sunlight. With $585 billion in CRE dry powder waiting to deploy, liquidity is coming back, just from new directions.

Partnerships and Alliances: Power in Numbers

CRE has always been cyclical—but this cycle is also collaborative. The report highlights a major shift toward strategic partnerships and joint ventures as the go-to growth strategy.

Why? Scale and specialization. As the cost of capital rises, teaming up allows firms to spread risk, share expertise, and unlock new markets faster than going it alone.

Take the April 2025 alliance between Blackstone, Wellington Management, and Vanguard. It’s designed to integrate public and private market exposure and bridge active and passive investment strategies. The takeaway: partnerships are becoming the new M&A—leaner, faster, and more adaptable.

Survey data backs this up. Seventeen percent fewer respondents plan to pursue traditional mergers or acquisitions in 2026, but alliances are trending up. Larger asset managers (with AUM over $15B) are partnering for operational expertise—especially in data centers, healthcare, and specialized housing—while smaller firms (AUM under $5B) are using partnerships to enter new markets.

Even REITs are getting in on it. Ventas partnered with GIC, Singapore’s sovereign wealth fund, to co-invest in life-science and healthcare assets. Expect more of that: REITs teaming up with private capital to diversify and scale.

And it’s not just finance. Across the data-center boom, partnerships with energy suppliers and tech firms are emerging to manage power costs and sustainability goals. Equinix’s collaboration with Bloom Energy for on-premise natural gas generation is a leading example of how CRE and infrastructure are converging.

Sector Highlights: Digital, Industrial, and Office Make a Comeback

The Deloitte outlook underscores a clear reordering of property-type opportunities—and some surprises.

Digital infrastructure—data centers and cell towers—has reclaimed the top spot as the most promising asset class. Demand far exceeds supply; in nine major global markets, 100% of new construction is already pre-leased. Power constraints are creating new growth hubs in Central Washington, Berlin, and Singapore.

Industrial and logistics properties, while cooling slightly after years of outperformance, remain strong. Short-term trade turbulence is slowing leasing, but long-term fundamentals are robust thanks to onshoring and the need for supply-chain flexibility.

And here’s a headline few expected two years ago: offices are finding their footing. Both suburban and downtown spaces are rising again in investor rankings. With record-low new construction and a gradual return to workplace normalcy, top-tier office assets are gaining favor.

Beyond the “core four,” alternative sectors—healthcare, grocery-anchored retail, and senior housing—are drawing competition even in a low-growth environment. Deloitte notes that the share of “nontraditional” property types in CRE portfolios has grown 10% annually since 2000 and is set to accelerate through the next decade.

AI in Real Estate: From Hype to Hands-On

Last year, everyone in CRE was talking about AI. This year, they’re asking: “Okay, how do we actually make it work?”

According to Deloitte, 19% of organizations are still early in their AI journey, and 27% report implementation challenges—mainly around data quality, technical expertise, and change management. The hype has matured into a realism that’s actually more productive.

AI’s real traction is happening in specific, high-impact areas: tenant relationship management, lease drafting, and portfolio optimization. Smaller, domain-specific models—rather than giant general-purpose systems—are becoming the tools of choice.

Think of this as the “fit-for-purpose” phase of AI in real estate. Instead of one giant model doing everything, firms are deploying small language models trained on industry-specific data—like lease clauses, property valuations, or zoning rules. These models deliver faster, more relevant results without the heavy computing costs of big AI.

Deloitte’s guidance is spot-on here:

-

Embed explainability and human oversight into all AI workflows.

-

Make AI literacy a company-wide initiative, not just an IT project.

-

Tie AI pilots to clear business outcomes—lease efficiency, underwriting speed, or tenant retention—rather than chasing headlines.

The message is clear: AI isn’t magic—it’s a multiplier. When paired with strong data governance and human expertise, it can supercharge operational efficiency.

What CRE Leaders Should Do Now

Deloitte closes the outlook with a reminder that the early-mover advantage is fading. In other words, this is the window to act before the crowd floods back in.

Here’s the 2026 playbook in plain language:

-

Stay selective and agile. Don’t chase every shiny deal. Focus on sectors insulated from short-term shocks and keep dry powder ready for opportunistic buys.

-

Rebalance with discipline. Use data-driven portfolio reviews to shift capital toward resilient, income-generating assets.

-

Expand through partnerships. Whether it’s a joint venture or a capital alliance, collaboration is now a competitive edge.

-

Stress-test everything. From refinancing exposure to asset valuations, know your weak spots before the market does.

-

Deploy AI strategically. Invest in targeted applications that drive measurable performance, not buzzword compliance.

The Bottom Line: The Opportunities Are Real

The commercial real estate story for 2026 isn’t one of doom—or euphoria. It’s one of preparation and pragmatism.

Yes, macro headwinds remain. But capital is coming back. Lending standards are easing. Digital and industrial assets are growing. And AI is shifting from promise to practice.

For leaders willing to move decisively, the opportunities are real. The recovery may be slower than expected, but it’s still on track—and the market rewards those who don’t wait for certainty to act.

As Deloitte puts it: Don’t wait for the comeback—help build it.

The CRE rebound won’t wait, and neither should you. 2026 is the year for decisive operators. Capital is coming back, data is reshaping strategy, and every square foot counts.

REoptimizer® gives you the clarity, analytics, and foresight to move before the market — and lead the recovery, not follow it.

Office markets are showing signs of stabilization. In Q2 2025, U.S. office markets recorded the fifth consecutive quarter of positive net absorption, even as vacancy held near 19%… Even with that, it shows a re-calibration of demand. Companies need to re-occupy strategically, consolidate footprints, and rethink what each square foot should do. Because, many major tenants still treat real estate as “that big cost you must minimize.” That’s short-sighted—and dangerous. The more forward-thinking occupiers now see CRE as a lever for growth, agility, and talent advantage.

But to make that shift, you need to ground your strategy in data, not hope. Because the difference between a passive portfolio and a strategic one often comes down to data, discipline, and design. Here’s how to tighten that gap.

The Utilization Delta: Your Hidden Liability

You don’t have “reserve capacity.” You’ve got wasted cost.

What the data shows today:

- According to the XY Sense Workplace Utilization Index, global workplace utilization over Q4 2024 to Q1 2025 averaged ~ 40%.

- While organizations are pushing for higher utilization, the gap between target and reality remains wide: in the 2025 JLL Global Occupancy Planning Benchmark, 74% of organizations collect utilization data, but only 7% rate their capabilities as “excellent.”

What these numbers mean for you:

- If you’re paying for 100 % capacity but only getting ~40 % usage, more than half of your footprint is functionally “dead weight.”

- Worse: utilization is uneven. Peak days may approach 60–70%, but off-peak days dip far lower, so much of your space sits underused most of the week.

- Because most firms lack rigorous data capabilities, they under-see or misjudge that waste.

That delta (space you pay for but don’t effectively use) is your strategic opening. Every point of utilization you reclaim can fund growth levers: experience improvements, tech, amenities, or even new markets.

Optimization ≠ Blind Downsizing

The impulse might be to slash square footage across the board. But that’s naive. Optimization needs nuance… think “redeploy, rezone, repurpose,” not just “retreat.”

Where value hides:

- Identify ghost zones (floor segments, meeting rooms, or underutilized wings) that see almost no traffic.

- Use sensor and badge data (desk booking systems, motion sensors) to map “hot spots” vs “cold spots.”

- Transition underused zones into flex, amenity, collaboration, or innovation space.

- Instead of blanket cuts, simulate trade-offs: “If we reduce X% in location A, can we invest in higher-impact space in location B?”

A disciplined, data-driven reconfiguration often yields 15–25% reductions in dead space (i.e. areas that generate no utility) — more meaningful than a blunt 10 % cut everywhere.

Location Intelligence: The Geography Behind Value

Where your offices are, and where you place new ones, increasingly determines your competitive edge.

What winning tenants do:

- Overlay labor supply maps, commute corridors, demographic trends, and climate/regulatory risk when choosing new nodes.

- Use geospatial models to anticipate where talent will live… not just where it works.

- Incorporate future optionality: can you expand in that submarket? Can you scale back if needed?

This is not theoretical. Industry reports show that 55% of global occupiers already use flexible office models, with 17% planning to increase usage. And as occupier demand shifts, capturing right-located nodes becomes a defensible moat.

Flexibility as Strategic Armor

Flex space isn’t fringe; it could be your buffer against volatility.

- In North America, demand for flexible workspace is now 19% higher than pre-pandemic, even as supply has only grown ~8%.

- Forecasts that demand for flex will continue rising in 2025, especially from occupiers seeking agility.

- Globally, flexible offices are dislodging traditional assumptions: 17 % of occupiers plan to increase flex usage.

Flexible office market forecasts are aggressive. One estimate sees growth from ~$41.6 billion in 2024 to ~$48.3 billion in 2025 (CAGR ~16 %).

Think of flex space as convenience stores. Ready-to-go, but with a price. While they come with more of a cost, they’re a great strategic lever.

Companies like Amazon are increasingly tying flexibility into portfolio structure. Negotiate expansion/contraction rights, or keep flex providers adjacent. Use flex space as your “shock absorber” to market swings or even test out new markets without the long-term commitment.

Build a Real Estate Intelligence Engine

To act strategically, you need a real-time spine of data. The more you unify layers, the more insight you gain.

Core data layers you need:

- Occupancy & utilization — sensors, badges, desk booking

- Lease & cost metadata — rates, term, escalations, options

- User behavior & experience metrics — surveys, app feedback, heatmaps

- Business signals — hiring plans, headcount forecasts, project timelines

- Risk overlays — climate stress, ESG, obsolescence

Speak the Language of Capital

Your real estate arguments need to land in the C-suite, anchored in business metrics… not floor plans. Translate your moves into value:

- Cost avoided / freed: show $/SF saved or reallocated

- Capital redeployment: what projects or strategic bets the savings fund

- Agility metrics: speed of expansion/contraction, time to relocate

- Talent impact: commute delta, space quality catchment, retention lift

- Risk mitigation: ESG exposure, building obsolescence, regulatory liability

Don’t sell “better workspace.” Sell “$10 million redeployable capital,” “3-month pivot capacity,” or “20 bps lower operational risk.”

Pivot, Learn, Scale

You can’t rewire your entire portfolio at once. Roll methodically.

Execution roadmap:

- Pick 1–2 markets with poor utilization and high cost burden.

- Deploy sensors, badge integrations, booking systems, and stand-up dashboards fast.

- Run test interventions — reassign teams, rezone collaboration hubs, carve flex zones.

- Track metrics — space savings, utilization lift, user sentiment, friction costs.

- Adjust and standardize the playbook.

- Roll out regionally over 12–24 months.

Within a cycle, your operational model moves from reactive to iterative.

Common Pitfalls (and How to Avoid Them)

- Overcooking the cut: Eliminating too much space too fast can erode collaboration, brand, culture.

- Data paralysis: Waiting for perfect data means no action. Start with what you have, layer in more.

- Siloed silos: CRE decisions made in isolation from HR, finance, ESG tend to misalign.

- Neglecting adoption: No matter how smart your plan, if users reject it, utilization will lag.

- Ignoring leases: You can hang clever design on rigid leases — but you’ll lose the optionality unless you re-negotiate clauses.

Avoid these, and you keep momentum.

Real Estate as Engine, Not Overhead

The numbers don’t lie. Most large-portfolio tenants carry 40+% of their space underutilized. That’s not slack—it’s opportunity.

Every underused square foot represents trapped value — in rent, energy, and opportunity cost. And yet, the fix isn’t cutting space blindly. It’s about turning your portfolio into a dynamic, data-driven asset that continuously aligns with your business, workforce, and financial goals.

That’s where portfolio optimization platforms like REoptimizer® come in. They’re not just reporting tools — they’re decision engines.

- They help you see your portfolio clearly: lease obligations, occupancy costs, utilization patterns, and scenario impacts, all in one view.

- They help you model outcomes: what happens if you consolidate markets, rebalance cost centers, or push utilization targets by 10 %?

- And they help you act decisively: surfacing which sites to renegotiate, right-size, or reinvest in based on data, not instinct.

The companies winning in this cycle are the ones who treat real estate data like financial data — tracked daily, optimized continuously, and benchmarked globally.

When you combine accurate utilization analytics with a platform that optimizes your entire lease portfolio, you shift from reactive cost management to strategic capital deployment. Real estate stops being a burden to explain and becomes a lever to pull.

In short:

- Optimize utilization.

- Deploy flexibility intelligently.

- Use location and cost data to make precision moves.

- Run the entire play through a real estate intelligence platform.

The payoff isn’t just efficiency — it’s agility, resilience, and better capital performance.

Your real estate should earn its seat at the strategy table. If it isn’t doing that today, the fix isn’t another spreadsheet — it’s smarter portfolio intelligence.

REoptimizer® gives you that edge. The rest is execution.

For decades, corporate America ran on a simple formula: hire big, train big, and house big.

Fresh graduates poured into the workforce every summer, filling sprawling back-office floors where they learned the ropes through long hours and repetition.

That system is vanishing, faster than many are prepared. The AI evolution is here.

By 2024, graduate recruitment at major tech firms had fallen 25%, as companies began prioritizing experienced hires over onboarding waves of rookies.

Combine that with the breakneck pace of AI, and suddenly, the old model, the one that once demanded entire floors of cubicles, is evaporating.

The result is fewer employees, fewer desks, smaller leases.

Companies that once relied on massive headcount to drive productivity are now building leaner, AI-assisted teams. And unlike humans, AI doesn’t obviously need an office.

The ripple effects on commercial real estate are profound. Headcount, long the cornerstone of leasing demand, is collapsing. Smart tenants are already pivoting. Those who hesitate risk being stuck with space they don’t need, in buildings that can’t adapt, on lease terms that lock them into the past.

The AI Shockwave: Six White-Collar Sectors in Danger

AI isn’t touching every industry equally. But certain white-collar sectors are already experiencing large-scale disruption. Let’s break them down:

1. Software Development: Fewer Coders, Faster Code

AI coding assistants like GitHub Copilot, Amazon CodeWhisperer, and Tabnine are rewriting the way software gets built. Developers using Copilot have cut coding time in half. Microsoft’s research shows productivity gains of up to 40% on complex projects.

What once required teams of 50 developers can now be accomplished by 10 with AI support. The impact on office footprints? Smaller project teams, leaner real estate needs, and less demand for sprawling engineering hubs.

2. Legal & Compliance: The Billable Hour Gets Automated

Contract review, NDA parsing, legal research—these once kept armies of junior associates employed (and firms leasing prime floors in Midtown Manhattan). Now AI tools like Harvey, Spellbook, and LawGeex can do them in minutes with higher accuracy.

A pilot with Allen & Overy showed Harvey cut legal research time by 80%. That means fewer associates, smaller offices, and lower real estate demand. BigLaw is already consolidating space across expensive metros like D.C. and Chicago.

3. Accounting & Finance: Structured Data = AI’s Playground

When rules are clear and data is structured, AI excels. Accounting and finance are ground zero. McKinsey estimates 38% of accounting tasks are highly automatable, while the World Economic Forum predicts up to 20% of roles could disappear by 2030.

AI bots now reconcile accounts, flag anomalies, and even support audits—leaving human staff to focus on strategy instead of data entry. Finance hubs in Charlotte, Tampa, and Salt Lake City are already seeing reduced demand for traditional cubicle farms.

4. Administration, Scheduling & Claims: Back-Office Bleed

Admin roles (once the backbone of suburban office parks) are evaporating. AI cuts health insurance claims processing time by 80% (Deloitte), while scheduling, billing, and documentation are being automated at scale.

Entire suburban admin hubs are shrinking. In Nashville, Phoenix, and Louisville, healthcare back-office demand is already softening. Translation? Fewer leases, smaller footprints, and rising vacancy in Class B/C suburban stock.

5. Customer Support: The Call Center Is Now Code

AI chatbots no longer just answer FAQs. They handle refund requests, ID verification, even escalations. Tools like Intercom, Dialpad, and Google Dialogflow already resolve 95% of Tier 1 support issues—and Accenture predicts AI will cover 95% of all support queries by 2025.

The fallout? Call centers—once massive job engines—are hollowing out. Those 500-seat suburban support floors? They’re going dark.

6. Routine Content & Data: Words Without Writers

HR letters, job ads, onboarding docs, even newsletters—AI drafts them all. In marketing, it builds campaigns that actually outperform human-created content: AI-generated emails see 25–40% higher engagement.

As companies adopt AI for templated writing and data summaries, creative-heavy offices are downsizing too. Teams are reconfiguring into hybrid pods, mixing strategists with AI tools instead of sprawling copywriter armies.

The Pattern Behind the Collapse

AI’s targets are clear:

- Repetitive tasks with predictable inputs.

- Data-heavy functions bound by rules.

- Standardized workflows with templated outputs.

In other words, AI is gutting entry-level white-collar work—the very layer of the workforce that used to justify massive training hubs and endless cubicle rows.

Which means: the apprenticeship system is crumbling, and with it, the office floors that sustained it.

Implications for Corporate Real Estate

The shift isn’t theoretical. It’s happening now:

- Fewer employees = fewer desks.

- Fewer desks = smaller leases.

- Smaller leases = shrinking office demand.

Companies that once leased 50,000 square feet for onboarding rotations are now running lean, AI-augmented teams in half—or even a quarter—of the space.

Headcount is no longer the metric driving real estate. AI is. And AI doesn’t need office space.

The Tenant Playbook: How Smart Occupiers Are Responding

The smartest tenants aren’t waiting for the dust to settle. They’re moving aggressively to realign portfolios with the AI reality.

Renegotiating Bloated Leases

Office utilization remains down 50%+ in major markets. Every unused desk is a liability. Proactive tenants are consolidating space now—before more jobs disappear.

Exiting Class B/C Assets

Vacancy in Class B assets has crossed 25% in cities like Chicago and San Francisco. These buildings are spiraling, with declining NOI and rising risk. Tenants are shedding them while they still hold leverage.

Demanding Major Concessions

With landlords under stress, tenants are negotiating hard. They’re securing tenant improvements in escrow, early termination rights, and over a year of free rent. The balance of power has shifted—and occupiers know it.

Embedding Flexibility in Portfolios

Instead of 10–15 year commitments, tenants are diversifying:

- 3–5 year leases with auto-renewals.

- Flex space integrations for project surges.

- Swing space mobility for seasonal needs.

Agility is the new currency of corporate real estate.

Where REoptimizer® Fits In

Spotting the trend is one thing. Acting on it effectively is another. That’s where REoptimizer® comes in.

Our platform equips occupiers to:

- Identify underutilized space and eliminate waste.

- Run “what if” scenarios to restructure leases proactively.

- Compare deals across markets so you negotiate from strength.

- Model future needs by layering headcount projections with AI-driven disruption.

- Embed flexibility with smarter lease structures and portfolio diversification.

REoptimizer® doesn’t just help you cut costs—it helps you future-proof your portfolio in a world where headcount is no longer the driver of demand.

The Bottom Line for Tenants

AI is collapsing white-collar headcount. The apprenticeship system is gone. The cubicle farms are going dark.

The apprenticeship model that once filled tens of thousands of square feet is disappearing. And every occupier is left with a choice:

- Keep carrying bloated leases that no longer match reality.

- Or act strategically—renegotiating, exiting, upgrading, and embedding flexibility—before the market shifts again.

The smartest companies are already making these moves. They’re not just cutting space. They’re re-optimizing portfolios to align with the future of work.

And with REoptimizer®, you don’t have to guess your way through it. You can use real data, real modeling, and real market intelligence to make confident, cost-saving, future-proof decisions.

Ready to see how REoptimizer® can collapse your real estate costs as fast as AI is collapsing headcount? Learn more today.

Most companies think about real estate too late—when they need to downsize, relocate, or when the lease renewal notice hits their inbox. But by then, it’s often too late to make strategic decisions. The real estate is making decisions for you.

Today, real estate optimization isn’t just about cutting costs, it’s about aligning every square foot with how your business actually operates.

Widespread portfolios need to base decisions around hard data, not assumptions.

And with this, decision-makers need the ability to see the entire portfolio clearly, across office, industrial, and logistics facilities, before those spaces become liabilities.

That means improving transparency, benchmarking against the market, and making smarter strategic decisions. Let’s dive in.

Square Footage Ain’t Free

Underutilized office square footage is one of the most substantial sources of financial waste in corporate portfolios. This is waste, plain and simple.

Even at $40/sf, a 10,000-square-foot surplus means $400,000 per year in unnecessary spend. That’s before factoring in taxes, maintenance, and energy costs. Now compound this across a 10 year- lease. Realistically though, companies are paying for much more wasted space on average. Recent industry studies estimate as much as half of office space today sits unutilized.

According to a 2025 Industry Occupancy Planning Benchmark Report, global office utilization reached just 54%, while utilization targets climbed to ~79%. That means nearly half of leased office space remains unused.

Warehouse inefficiencies hurt just as bad, but can come in different forms. Drags on efficiency often come as supply check bottlenecks due to poor warehouse locations.

If your warehouse location is 30 miles from your key customers or your intermodal hub, you’re not just paying extra in rent, you’re compounding transportation costs, slowing delivery times, and damaging customer satisfaction.

Every square foot in your portfolio needs to earn its keep. That means knowing:

- What’s actually being used—and what isn’t

- What square footage costs across markets

- Which spaces are high performing versus high-risk

- When leases roll over—and where hidden escalation clauses live

The goal? Replace guesswork with clarity.

Your Portfolio Is Only as Strong as Its Weakest Site

Let’s say you have five warehouses, but only three drive 80% of throughput…or you have six regional offices, but two haven’t been fully staffed since 2021.

Every location that underperforms isn’t just dead weight, it’s tying up capital, wasting labor, and diverting executive focus.

This is why real estate portfolio optimization starts with filtering by performance metrics including:

- Utilization rate (especially for office)

- Transportation costs and proximity to major highways, intermodal hubs, and customers

- Workforce availability and labor costs by metro

- Total cost of occupancy (rent, CAM, taxes, insurance)

- Building age, code compliance, and maintenance status

And here’s the kicker: You need to see these metrics side by side. Not in six spreadsheets or five regional folders—but on one integrated map or dashboard.

Visibility Is the First Step to Control

Let’s talk about a basic reality: most companies don’t have a centralized, living document of their lease portfolio. Without this, you’re really flying blind.

You need a portfolio tool that tells you:

- Where you’re overpaying

- Where lease renewals or expirations are looming

- Where your business units are underutilizing (or outgrowing) space

- Where opportunities for consolidation exist

Imagine knowing the exact square footage, lease terms, critical dates, rental escalations, and market comps across every property you occupy.

That’s how you get proactive instead of reactive.

This is how smart companies see what no one else sees: when to negotiate early, when to exit, and when to double down on a location before demand spikes.

Office and Warehouse Optimization Have Different KPIs—But the Same Goal

Too often, portfolio reviews lump office and industrial space into the same discussion. But they’re fundamentally different assets with different drivers:

Warehouse Optimization Requires:

- Proximity to robust transportation infrastructure

- Lower handling costs

- Efficient inventory management layouts

- Easy access to highways, ports, and rail

- Local environmental factors and compliance with building codes

- Labor costs and workforce availability

- Ideal storage area vs. raw materials sourcing

Office Optimization Requires:

- Rightsized square footage based on headcount and hybrid policies

- Lease clauses that allow early termination or downsizing

- Sublease potential or coworking alternatives

- Visibility into occupancy vs. utilization

- Energy efficiency and total cost of operations

- Proximity to talent pools and commuter hubs

But both demand the same thing: data visibility.

Benchmark to Market — Once You See Your Costs, You Can Optimize Them

You can’t fix what you don’t measure.

Once your portfolio costs are visible, the next step is benchmarking them to market. Too many companies are still paying above-market rents for warehouse space or office square footage—simply because no one flagged it in time.

- Compare your current leases to active comps with similar warehouse location, transportation access, square footage, and labor availability.

- Assess how each site performs against your Key Site Drivers—whether that’s commute time, distribution network alignment, or regulatory complexity.

- For office assets, dig into underutilized areas, renewal options, and early termination rights that could unlock flexibility or savings.

Companies that take this step routinely uncover 10–30% savings compared to current market conditions.

Tools like Reoptimizer® let you run these comparisons portfolio-wide, surfacing which locations are still aligned…and which are overdue for renegotiation, consolidation, or exit.

Key Dates Are Strategic Leverage

Every missed lease milestone is a missed opportunity, often a costly one.

The best-run corporate real estate teams don’t just track key dates; they act on them early. Hitting renewals, expansion options, or terminations early gives you leverage leverage to renegotiate, consolidate, relocate, or walk away altogether.

The average corporate real estate team is sitting on millions in potential savings just by acting 12–18 months earlier on key dates.

In a market defined by uncertainty and excess space, timing is one of the few things you can still control. When you act early, you create leverage. When you wait, you lose it.

If you know when a lease expires or when the termination notice must be given, you maintain your negotiation power. If you don’t? You’re at the landlord’s mercy.

Smart tenants are asking:

- Can I use my lease expiration to renegotiate?

- Do I have a right of first refusal on adjacent space?

- Is there an upcoming market downturn I can capitalize on?

- How many leases roll in the next 6 months? 12 months?

REoptimizer® tracks these dates, flags them in advance, and ties them to financial modeling. So, you’re never caught off guard—and always ready to play offense.

The Best Portfolio Strategy Is a Living One

Too many companies treat portfolio decisions like one-time events. A new lease is signed. A site is decommissioned. A relocation is completed. And then… everything goes quiet until the next disruption.

But the best real estate strategies are continuous. Because your business evolves—so should your portfolio.

This means regularly revisiting:

- Which properties align with your strategic goals

- How hybrid work is affecting office needs

- Where fulfillment times are slipping

- How much space is being wasted—and why

- Where labor trends and supply chain bottlenecks are shifting

And that requires a system—not a spreadsheet. Something that connects the dots across square footage, cost, usage, operations, lease terms, and future needs.

Your Portfolio Can Be an Asset or a Liability

Real estate is often the second-largest expense for a business. But it’s also one of the most under-optimized. The difference between a bloated, scattered, inflexible portfolio ,and a streamlined, insight-driven one, is millions in annual impact.

Most importantly: you can’t optimize what you can’t see.

Whether you’re trying to reduce lead times in your supply chain, trim excess office space, or plan your next 3 warehouse locations, data clarity is everything.

REoptimizer® exists to make this possible. It’s built for corporate tenants who want to own their data, control their costs, and make real estate a strategic weapon—not a sunk cost.